The Weekly Insight Podcast – Where’s the Drama?

Well, this is new. A week without much drama! The Fed news is behind us (for now). The war in Ukraine is ongoing, but there have not been any significant changes as it would relate to the markets. Some are starting to be concerned about the newest COVID variant, but it has not affected caseloads in the United States (yet?). Overall, the market was up, and it was kind of a boring week.

But, as usual, that won’t last! So, we’re going to take some time this week to go through a “grab bag” of issues that may impact the market over the coming weeks. We will stay away from predictions here. Instead, we want you to have an opportunity to see what it is we’re watching as we enter Q2 and how these items may impact our thinking for the rest of the year.

COVID BA.2 Omicron

You have probably heard of the BA.2 variant of Omicron by now. It’s often referred to as “stealth COVID.” It’s becoming the latest driver in the 2-year COVID story. Per a World Health Organization report last week, BA.2 is now the dominant version of COVID around the world making up 86% of the cases reported to the agency.

Per the CDC, BA.2 has not yet become the dominant strain in the U.S with just about one third of cases being tied to the new variant.

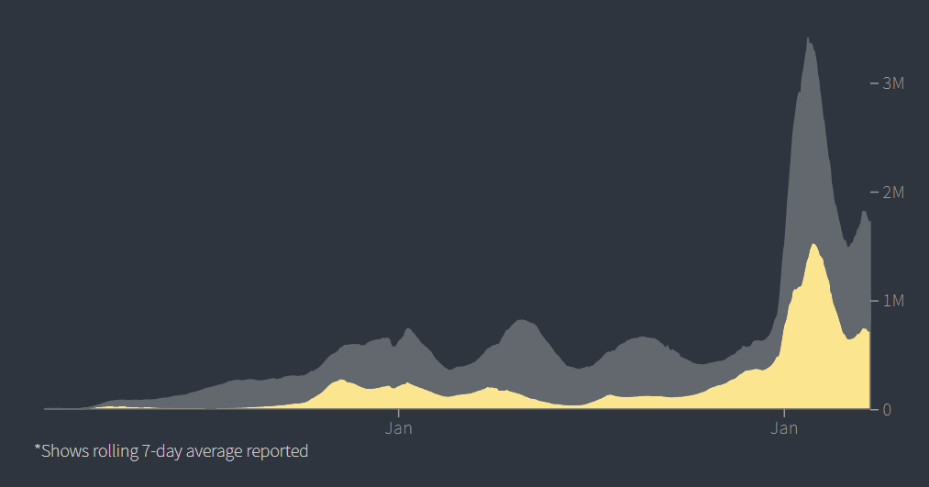

The question for us is will this new strain impact the economy in the way original COVID, or Delta COVID, or the original Omicron COVID did? In previous surges we have experienced, economic activity has slowed and restrictions that had previously been relaxed have been reinstated. In each of those cases, the surge started in Europe. And they have experienced a bit of a surge over the last few weeks.

Source: Reuters

Past performance is not indicative of future results

COVID has been a politicized mess. But as you know about us, we like math. You cannot politicize math! So, let’s look at a few facts:

- COVID vaccination is effective at preventing severe disease from BA.2 (per the CDC).

- Previous Omicron infection is effective at preventing severe disease from BA.2 (per the CDC).

- 217,000,000 Americans are fully vaccinated.

- Using our previously discussed formula of four times reported cases, roughly 110,000,000 Americans contracted Omicron (a low estimate in our understanding of the data)

Simply put, there is a LOT of immunity out there right now against BA.2. That is why Dr. Anthony Fauci said last week that there will “likely be an uptick in U.S. cases this spring, but hopefully we won’t see a surge. I don’t think we will.”

We will see. But history tells us he may be right. Past surges that have started in Europe have then popped up in the U.S a brief time later. That has not yet happened here. While the 7-day positive test rate has not improved in the last week, it is at its lowest level since prior to the Delta variant. Knowing that BA.2 is here (1/3 of positive tests) without a significant spike as was seen in Europe may be a good sign. Now we watch and wait.

Economic Data

Anytime we come to the end of a month or end of a quarter, we are gearing up for significant news on how the economy performed in the preceding period. There are always a lot of assumptions and hope (or fear) but getting real data can set the mentality for the market over the coming weeks and months.

This week we will start seeing some of that data, especially on Friday, April 1st. That is when we will get the March payroll and unemployment data as well as the Manufacturing PMI data. The expectation right now is that we will add 475,000 jobs (down from 678,000 jobs in an excellent February) and that Manufacturing PMI will be flat at 58.6 (a fantastic number). Any miss on these data points and we may see a rocky end to the week.

Then it is a long wait until the middle and end of the month where we start getting information on inflation, GDP, etc. And that will all hit right about the time we start to get to…

Earnings

That’s right, our favorite season is about upon us: earning season. There’s been so much talk about war, inflation, and interest rates in these pages over the last few months. And with good reason. But we cannot forget about the other big thing that moves markets: how companies are performing. We are going to be getting the report card soon.

In the meantime, we can look at what we know today and what analysts are predicting for the coming weeks to get an idea about how good or bad the Q1 print might be.

First, we look at the forward earnings estimate. We have beaten this into readers for a few years now, so we will try not to belabor the point. But right now, the S&P 500 is trading at a forward 12-month estimate of 19.50 earnings. High? Historically, yes. But significantly lower than the twenty-five times number we saw last year. And much closer to the 10-year average of 16.8x.

That number goes up or down based on two things: are earnings expected to grow or shrink? And is what the market is willing to pay for those earnings going up or down? As we head into earnings season, we are most concerned about the former. Let’s look at what analysts are saying right now.

First, we should report that the estimate for Q1 earnings growth now sits at 4.80% (per FactSet). That is down from the beginning of the quarter when the estimate was 5.7% and is the lowest estimate since Q4 2020 when it was 3.8%.

Negative revisions seem bad, right? Yes and no. You will recall a few memos we wrote last year about how strange it was analysts were revising their estimate upward during the quarter. Before the post-COVID boom, this was nearly unheard of. Analysts tend to be more optimistic at the front end of a quarter and then use the information they gain during the quarter to bring their estimates more in line with reality. We should also note that the economic impact of Omicron all happened during Q1 which has undoubtedly impacted earnings.

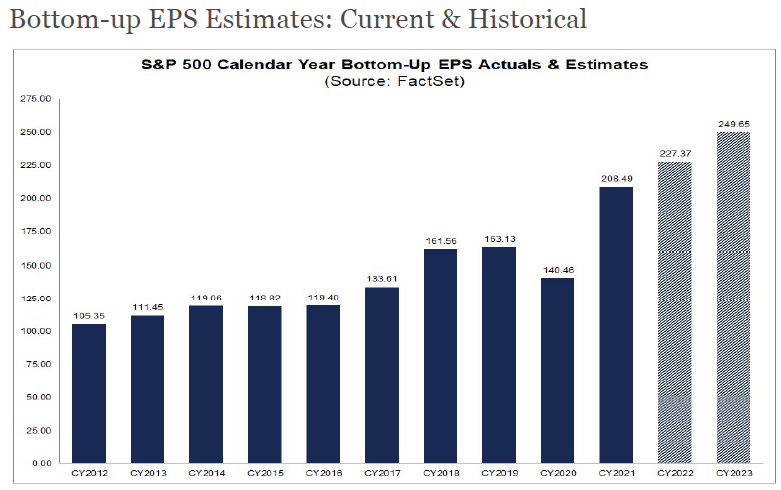

More importantly, that 4.8% earnings growth rate still leaves us on pace for 9.4% earnings growth over calendar year 2022. That still puts us well above the historical trend for the last decade. And that is with everything the world knows about COVID, wars, and inflation.

Source: FactSet

Past performance is not indicative of future results

The bottom-up estimate from analysts puts the S&P 500 at a total index value of 5,278 one year from now. That would be approximately 17% growth in the index over the next 12-months. That seems a little optimistic given what we know is happening in the world today. But even if the number is half of that, we would certainly be pleased with the results.

So now we wait to get the real data! It is coming soon, and we’ll look forward to reporting it to you. In the meantime, do not hesitate to reach out if you have any questions about the market or your personal portfolio.

Sincerely,