Time is a weird beast. If you are like us, this COVID season has both raced by and crawled. In some ways, it seems like we have been dealing with this pandemic FOREVER. Yet it also seems like we just sent you a note about earnings season a few weeks ago. It seems odd that a whole quarter has passed, and it is time to do this yet again.

We have talked for several weeks about the conflict between fundamentals, the pandemic, and the election. Last week we spent a good bit of time on the process for the vaccine. We have to admit we felt a bit silly talking about the prospects of the three most likely candidates when – just hours after we sent the memo – Johnson & Johnson (JNJ) announced they were pausing their trial due to unexpected illness in a patient (more on that later!).

The week before we dove into the election. That is a topic we are going to dive into in depth over the next couple of weeks – including an exciting 2020 Election webinar with two former White House Political Directors and our friend Phil Kosmala. We hope you will join us to learn more about how the outcome of the election will impact the market. Invites were sent via mail and email last week. You can RSVP by going to www.InsightWealthGroup.com/Election2020.

But this week we are going to focus on the stuff we enjoy – fundamentals. It is nice to be able to focus on the things we can tangibly see and understand. There are so many unknowns about the election and the virus. But audited financial data? That is what we love. Let’s dig in.

Economic Growth Will Recover

It is important to remember what the financial press means when they are discussing “expectations”. Whether a company beat its earnings is a function of expectations: how did they perform vs. how analysts expected them to perform. Beating expectations is certainly good – but we must understand expectations are still a function of human emotion.

The COVID-period is a perfect example of how this works. You may recall our writing in the beginning of this epidemic discussing the expectations for GDP growth for the year considering the various shutdowns. At the time, we saw some brutal expectations. One large bank in New York was predicting a 25% hit to GDP for the year. The consensus was close to -10%. At the time, we were discussing our opinion that it would be closer to -5%.

Why? It is simple. In the heat of the moment, emotions run high and the situation – one we have never seen before – seemed catastrophic. Human emotion drove those apocalyptic expectations. Now – however – with the smoke clearing, we see estimates for 2020 GDP is coming in at less than 5% both here at home and for the world economy.

Past performance is not indicative of future results

This is an important backdrop to remember as we walk through earnings expectations for Q3. We mentioned in our last earnings memo an interesting fact: earnings expectations typically get worse throughout the quarter no matter the economic condition. It is a function of analysts hedging their bets. Much like the old GDP forecasts it creates a very low bar to clear. We are seeing that so far with the Q3 numbers.

Clearing the Bar

As we mentioned – the bar this quarter is very low. Typically, quarterly earnings are compared using a year-over-year analysis. I.e. are the Q3 numbers in 2020 better or worse than the Q3 numbers in 2019. Obviously, they will be worse, and analysts have projected, on average, they would be 21% worse.

Admittedly, we are not very deep into earnings season right now – but we are starting to get a good sample size. The results are positive. Of the companies that have reported, we are seeing the following:

- 86% have beat the analysts’ estimates.

- Of those that have beat they are reporting earnings which are 21.7% above estimates. That is a very large number. The average over the last five years is 5.6%.

- The updated estimate for the quarter is now a year-over-year decline of 18.4% (still a large number!). We will be watching to see if this comes down over the next few weeks as more figures come in. If we continue to see “beats” of this magnitude, it should come down more.

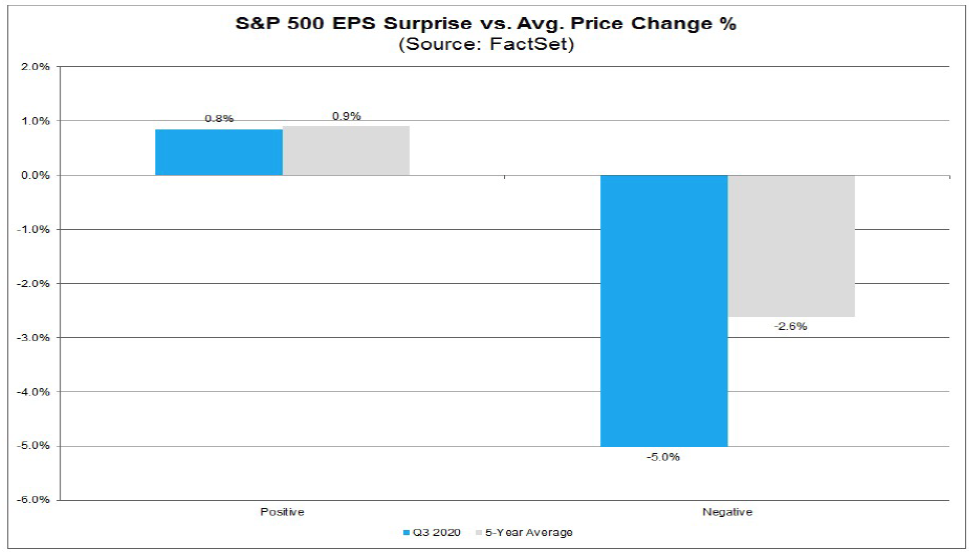

Interestingly, failure is being punished this quarter much more than success is being rewarded. As you will note from the chart below, positive “beats” are trading up – on average – 0.80%, slightly less than the historical average. But those few companies who have missed their earnings expectations are being pounded – down 5.0% on average.

Past performance is not indicative of future results

America Still Matters – But 2021 May be a Year for International

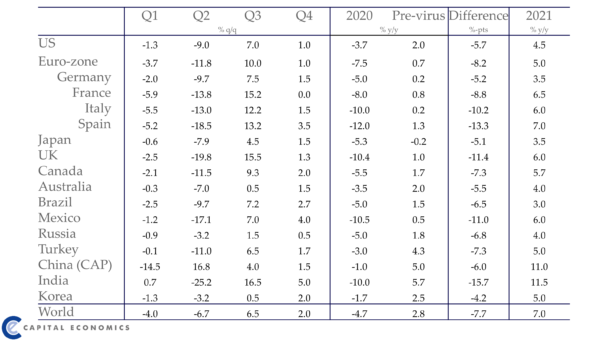

We have shown many charts in the last few months showing how we believe the international markets – particularly developed Europe – are priced well relative to U.S. stocks and will present an opportunity in the months and years to come. If you look back to the GDP chart we posted earlier, the 2021 growth expectations make that case well. While U.S. GDP growth is anticipated to be a decade-best 4.5%, it is substantially below the worldwide expectation of 7.0%.

We must, however, give credit where credit is due. One of the reasons our GDP is expected to be lower next year is our contraction this year is much smaller than the rest of the world. Our 3.7% contraction estimate compares favorably with nearly every developed country in the world.

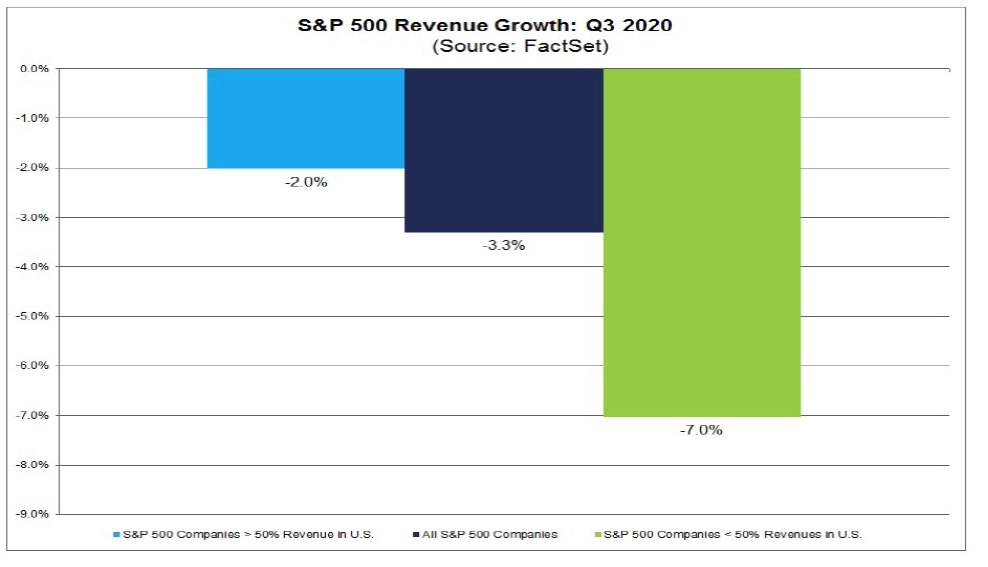

That is coming through in earnings. As you can see below, S&P companies that have greater than 50% of their revenue generated domestically are performing substantially better than those with the majority of their business overseas. This is a justification for maintaining a strong weighting domestically – for now – but being prepared to participate in what is likely outsized growth overseas next year.

Past performance is not indicative of future results

Big Tech Warning

We know, we know. We have been complaining about the valuations of Big Tech for a long time now. Logic, it seems, does not matter all that much when it comes to these stocks. Momentum is driving them now – not math.

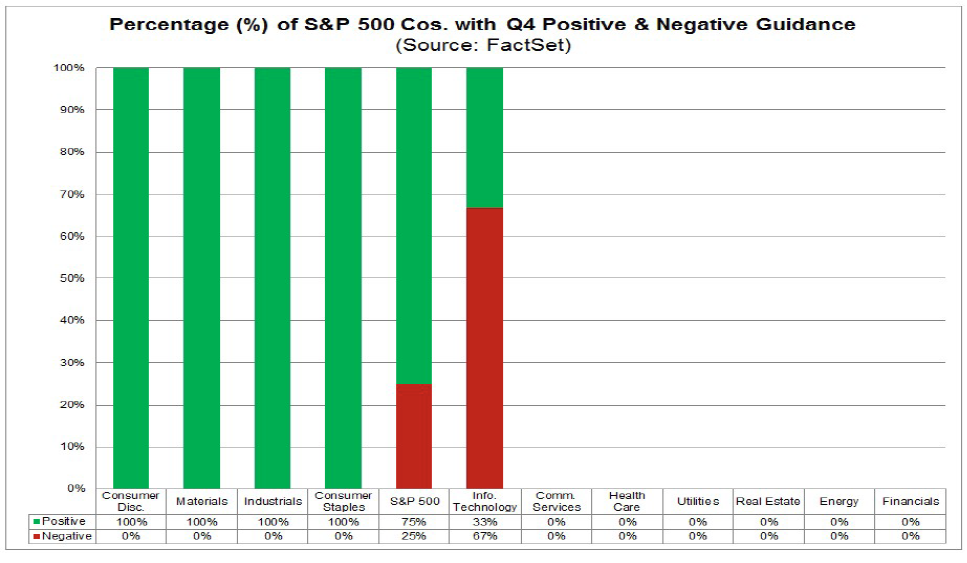

While, as mentioned before, we have a fairly small sample of companies reporting earnings, one data set is interesting: there is only one sector where companies have provided negative guidance for Q4: Information Technology. Valuations have not mattered in this sector for a while – so we do not know why earnings would matter at this point. But this is an important thing to watch.

Past performance is not indicative of future results

Energy Update

We have fallen on this sword more times than we can count this year. Our biggest miss of COVID season has been our exposure to energy. Yet the worse it looks the more confident we are in the recovery. As we have noted in previous memos (see: The Case for Energy, July 27, 2020), the disruption in this space has so impacted exploration and supply, prices will undoubtedly have to improve.

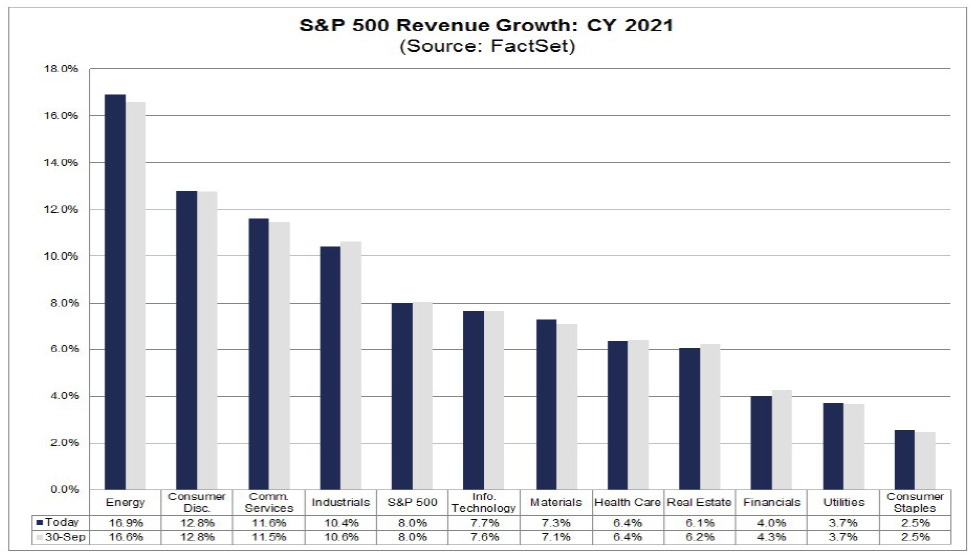

It seems analysts are starting to take notice. The 2021 expectations for the energy sector are better than any other area of the market. Our exposure here should be a positive catalyst for portfolios in 2021.

Past performance is not indicative of future results

Earnings Do not Always Trump the News: The JNJ Example

We noted at the beginning of this memo our embarrassment over the Johnson and Johnson vaccine trial being “paused” just hours after we sent a memo discussing it as a potential solution to the COVID-19 problem.

But our missing the mark is not the real point of the JNJ discussion. Instead it is this: JNJ reported very good earnings results this week. Their year-over-year earnings were positive 3.5% (a far cry from the overall market expectation of -18.4%). Adjusted earnings per share were up 3.8% from Q3 2019.

That should make for a good week for the stock, right? Wrong. COVID still carries a lot of weight in this environment and JNJ’s announcement of the pause rocked the stock. In a week with overall poor market performance (S&P down 1.43%), JNJ was down more than 3%.

We must all remember that – no matter our optimism in the numbers – this is not just a numbers game. In the end, the numbers matter. But getting there can be a long and winding road. And getting there from 2020 will mean getting past this election and solving the COVID puzzle. We are on our way – but we are not there yet.

Sincerely,