The Weekly Insight Podcast – $235 Billion Has to Come from Somewhere

Last week, the world’s largest IPO landed. Everything else was noise. Economic news, drama in the Strait of Hormuz, and none of it mattered. There was only one story worth watching: the SpaceX (SPCX) IPO.

And for good reason – it was the largest IPO (by market cap) in history. And the scale of the shares released to the public (556 million at $135 per share) was unprecedented. SpaceX raised $75 billion in a single day. Given the entire U.S. IPO market last year was $45 billion, that’s a big deal.

But hopeful investors were likely disappointed. What was initially 30% of the shares going to the investing public (vs. institutions) was reduced to 20% days before the listing. And investors who signed up got a fraction of the shares requested. Not much to write home about.

The day of the event tracked almost perfectly with history. You may recall us discussing a study called The Long-Run Performance of Initial Public Offerings by Dr. Jay Ritter. His data shows, since the early 1980s, the average IPO pops 18.1% on its first day of trading. SPCX shares were up 19.22% on the day.

But the main story of this IPO – and the future AI public offerings of OpenAI and Anthropic – wasn’t written on Friday. It’s going to be written and re-written over the next 180 days. And the impact on the broader market has the potential to be significant.

It comes down to two distinct – but inextricably linked – timelines: the lock-up periods for pre-IPO investors in SpaceX and the forced buying timelines for institutions.

The Sell Side

We’ve all heard the stories by now: the janitor at SpaceX who is now a multi-millionaire. The welder making $28 an hour who amassed $880,000 in stock. It’s an amazing windfall for the people who put the work in every day at SpaceX. Over 4,400 current and former employees became millionaires (on paper) Friday.

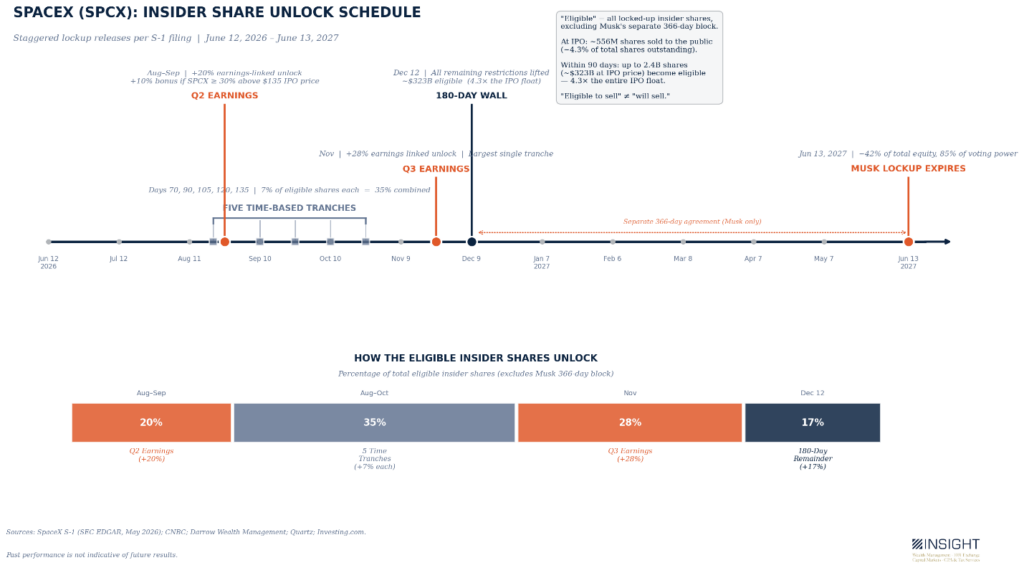

But those shares are a relatively small piece of the puzzle. The bigger piece is the pre-IPO investors who are now going to be looking for liquidity. And the lock-up schedule through which it will happen is incredibly important to understanding the future value of SpaceX shares.

Before we dive into the timeline, let’s briefly understand who actually owns shares of SpaceX. Per the S-1 which preceded the IPO, there are 13.076 billion shares of the company. They are broken out as follows (these numbers are rough estimations from the S-1, not precise figures; values are as of the Friday’s close at $160.95):

- Elon Musk (42%): ~5.49 billion shares worth ~$884 billion

- Alphabet (Google) (7%): ~915 million shares worth ~$147 billion

- IPO shares (4.25%): 556 million shares worth ~$89.5 billion

- Insiders/Pre-IPO Investors (~46.75%): ~6.11 billion shares worth ~$984 billion

Combined, that is a $2.1 trillion market valuation as of COB Friday. But only 4.25% of it is actually trading on the open market. The timing of the rest is staggered and will greatly impact both the future share price and the availability of shares.

Past performance is not indicative of future results.

No doubt the chart above is a bit confusing. But here’s the point: from now until August, the “float” (shares available for public trading) is incredibly small. Just 4.25% of the company shares trade on the open market. But by the time we get to August, the floodgates begin to open, and more and more shares will hit the open market. By December 9th – 180 days from the IPO – the number could grow to as many as 7.58 billion shares. Which is more than 13.6x the number of shares available today.

Now – the fact investors (both individuals and institutions) can sell their pre-IPO shares doesn’t mean they will. Many insiders will hold. But not all. And the potential supply overhang is what markets will be pricing. So, if you’re trading shares of SPCX, be very aware of the dates noted above. The market will be and it will impact pricing.

Passive Isn’t Passive Right Now

Insiders dumping shares will weigh on the price of SpaceX stock in the coming months. But that’s natural with any IPO. What’s not natural is the forced buying which will happen – both as a function of the sheer size of this company and the market mechanics at play.

The Hollywood version of Wall Street is quant nerds in a room finding the one piece of data no one else discovered. But that’s not how it works. Instead, in response to the demand of investors, over 50% of total equity holdings in the U.S. are in passive holdings. Meaning investors are buying and holding indices.

There are benefits. Lower turnover (typically), lower fees. Passive investing is the ultimate buy and hold. And let’s be clear – we use a sizable number of passive strategies in our models. For the exact same reasons retail investors love them. There are certain parts of the market where the best way to get exposure is through a passive interest.

But there are mechanics of “passive” investing which can make it seem significantly more active than normal. And we’re barnstorming straight into one of those moments. It is not a choice investment managers will make. It is simply a function of the mechanics of the market. And it’s going to shake things up.

How Index Participation Works

The S&P 500 is the granddaddy of all the indices. It’s run by Dow Jones, Inc. and has a very defined process for participation:

- Be one of the largest companies by market cap in the United States

- Be profitable

- Be listed for one year

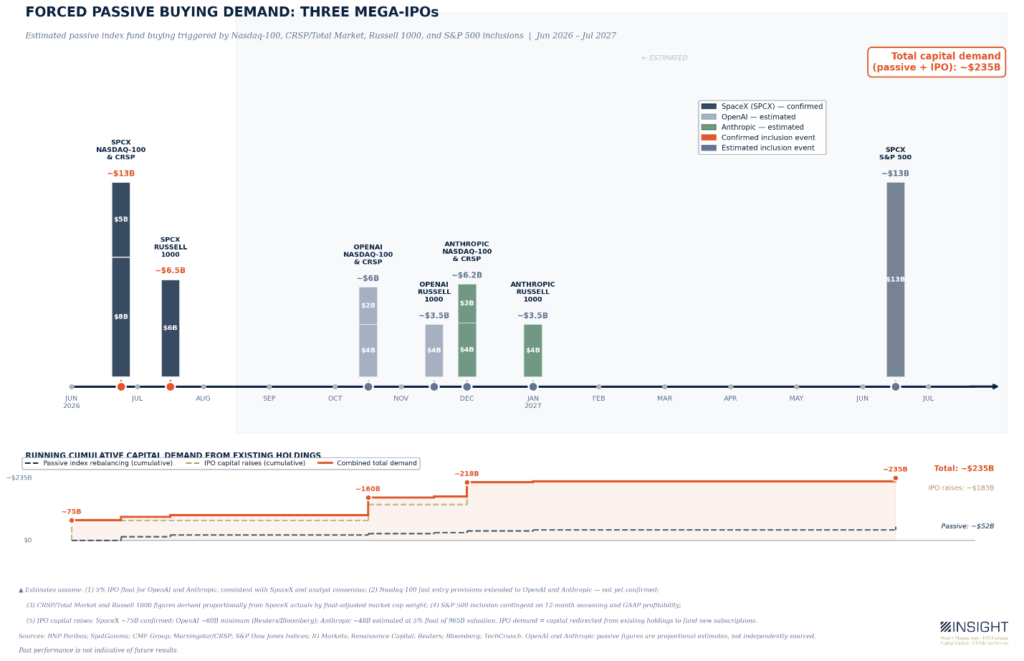

By that standard, SpaceX is at least 12 months away from S&P 500 listing. And the “Be profitable” standard may stretch that period out even further. But the S&P isn’t the only kid on the block.

There are three other indices which are extremely excited to include SpaceX. The Nasdaq-100, in fact, made a special exception to their rules to allow participation within 15 days of listing. The Russell 1000 plans inclusion within 30 days. And one you’ve likely never heard of – CRSP, the index behind Vanguard’s total market funds – which is far bigger than the rest, may include SpaceX within the first week.

Massive Buys Mean Massive Liquidity Demands

That means a massive demand for SpaceX shares in the next month. Rough estimates put it at $20 billion worth of shares. Using Friday’s closing price, 22.3% of all shares which are available today will need to be bought up in the next month.

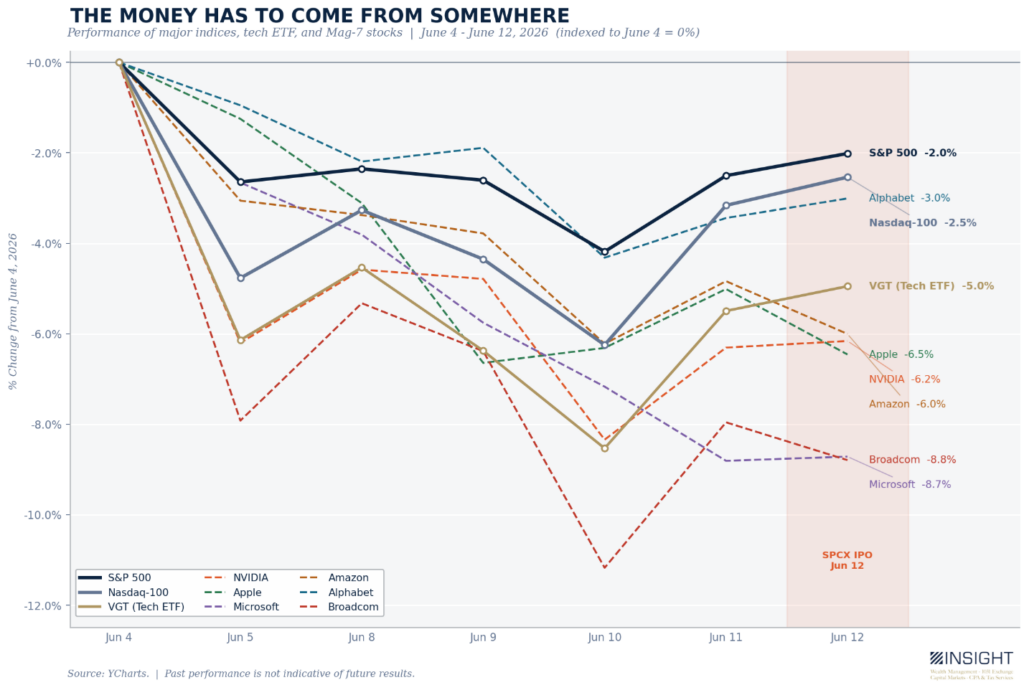

So, the market already produced $75 billion on Friday to buy SpaceX shares. Now another $20 billion will be traded. $95 billion in one stock. The money has to come from somewhere. It doesn’t materialize out of thin air. It comes from other positions. We’d suggest that’s exactly why we saw such volatility in tech stocks leading into Friday’s IPO.

But none of that considers the passive buying. Those managers – by the very investment policies which govern them – can’t make the changes until the index makes the change. When the change happens, a significant amount of forced buying – and forced selling – will occur.

SpaceX Is Just the Start

We mentioned this in our previous SpaceX memo, but it bears repeating. This IPO was huge. But it’s not the only one coming. OpenAI has already done the initial filings for their IPO and intends to hit the market this fall. Anthropic – the maker of Claude – filed its own confidential S-1 on June 1st and is expected to IPO this fall.

The same liquidity needs we saw with SpaceX will repeat. Massive amounts of cash will be necessary for both the IPOs and the passive listings.

Past performance is not indicative of future results.

Between the IPOs and the passive trading, these three companies would – given current estimates – chew up more than $220 billion in capital between now and January. If SpaceX does make it on the S&P 500, the number will climb to $235 billion by next June.

Estimates show U.S. equity markets have volume on an annual basis of ~$25 trillion. So, in the grand scheme of things, $235 billion is big – but not extreme. It comes to roughly 0.3%.

But it’s not that simple. There are roughly 250 trading days in a normal year. Which means daily equity volume is ~$100 billion. The liquidity demands for the shares of these three companies happen on thirteen specific trading days over the next year:

- IPO Day (x3)

- Nasdaq-100 inclusion (x3)

- CRSP inclusion (x3)

- Russell 1000 inclusion (x3)

- S&P inclusion (SpaceX)

Thirteen normal trading days would have volume of $1.3 trillion. Which means – on those specific days – the impacts of these IPOs will make up a total of 18% of normal volume (much, much higher on the IPO days!).

The Impact on Markets

The last few weeks were a preview of what is to come in public markets. The dates are largely known. The liquidity needs are largely known. And – by virtue of how the mechanics of markets work – the biggest impacts will be felt by the biggest companies. Which happens to be exactly how the market has gotten its AI exposure up to this point.

Past performance is not indicative of future results.

Will things bounce back into shape the minute the market digests these big buys? History says yes. The market has absorbed every supply shock before this one. But history didn’t have three trillion-dollar companies lining up in the same calendar year.

The FOMO of these moments – we need a piece of the next big thing! – is a real draw. And it’s not wrong. Yes, investors should have some exposure to the first true AI names to hit public markets. And we will – if only through exposure in broader indices.

But we must remember where the money comes from. The dates are on the calendar. The supply events are visible from here. Investors who understand the plumbing don’t need to be surprised by the pressure of the specific moments to come.

Sincerely,