The Weekly Insight Podcast – The Warsh Standard

There was a time – during the post-COVID inflation surge – that this memo could have been aptly retitled “The Weekly Fed.” We spent considerable time in these pages discussing Fed policy and trying to understand what it may mean for the markets.

And for good reason. The Fed was one of – if not the – biggest drivers of market volatility during that time. And it’s not a new phenomenon. The New York Fed did a study in 2011 that showed that from 1980 – 2011 nearly half of all realized excess stock market returns happened in the 24 hours before an FOMC announcement.

But, during the Powell era, that dynamic changed. Instead of “Fed days are good days,” it became “Fed days are messy days.” To understand this, you need to understand that two things happen on FOMC meeting days. First, the FOMC releases their Statement at roughly 2:00PM EST. Then, thirty minutes later, the Chairman holds a press conference.

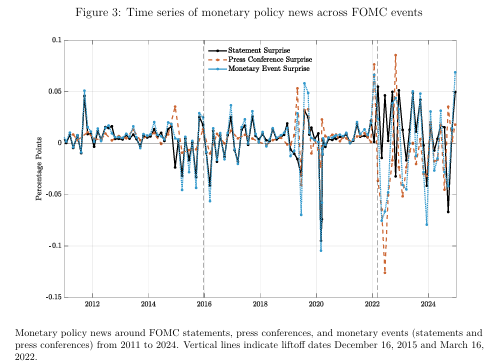

What happened during the Powell era was interesting. In a study by the San Francisco Fed, titled Financial Market Effects of FOMC Communication, authors David Lucca and Emanuel Moench determined that whatever direction the Statement moved the market, Chairman Powell moved it in the opposite direction during his press conference.

Source: Financial Market Effects of FOMC Communication

Past performance is not indicative of future results.

Even a layman’s eye can see the change. The “messiest” part of the chart above is after Powell became Chair in 2018 and especially after inflation hit in 2022. Powell – and his FOMC – consistently moved markets (in one way or another). Parsing Powell became more important than analyzing the economy.

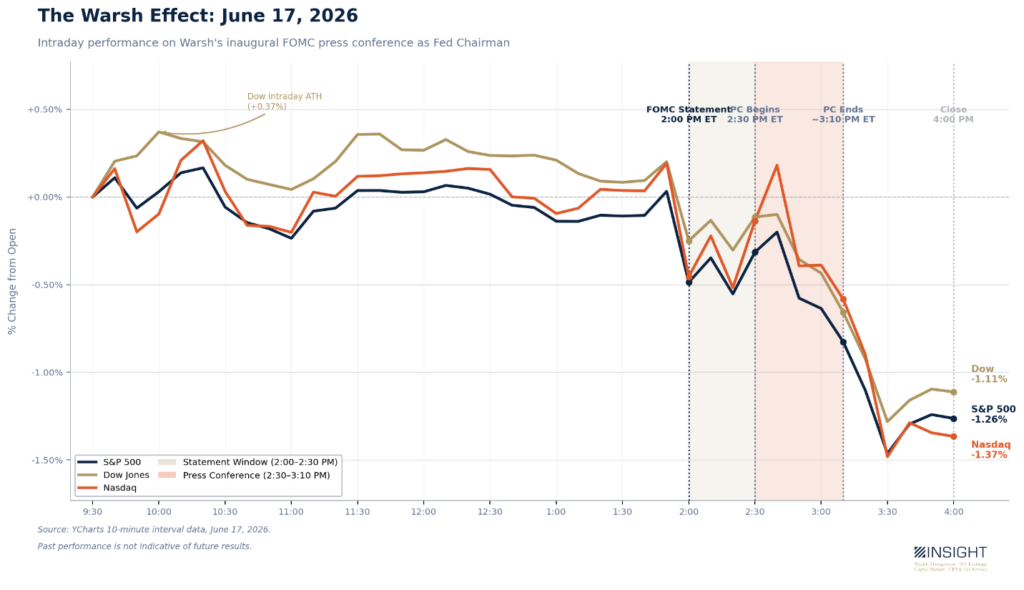

Enter new Fed Chairman Kevin Warsh. His press conference on Wednesday announced a fundamental restructuring of how the Fed communicates. As different as he may be, however, the market’s reaction was remarkably similar. A bump up between the statement and the press conference followed by a strongly negative move during and after the press conference.

Past performance is not indicative of future results.

So more of the same? If his first press conference is to be believed, the answer to that is a resounding “No.”

The Circular Sentiment Firing Squad

Four years ago this week, we wrote a memo called The Circular Sentiment Firing Squad. It was the memo that came out following the Fed’s 0.75% jump in interest rates (one of the largest ever) after a bad all-items CPI print. It was the first of what became four consecutive 0.75% rates hikes.

We won’t rehash the whole memo, but the gist of it was this: despite the Fed’s “preferred inflation indicator” (core PCE) falling, the Fed took a drastic step in reaction to market sentiment and the public’s “feelings” about inflation. The market loved it on day one. But by the end of the day Thursday, markets were off hard. The S&P was down 3.25%. The Nasdaq was down by over 4.05%. The markets all of a sudden shifted from “the Fed needs to act on inflation” to “the Fed is going to cause a recession with these huge rate hikes.”

At the time we noted that the Fed was making decisions based on “sentiment.” But those moves were changing sentiment which in turn either justified or invalidated the Fed’s decisions.

The results have not been how anyone imagined the modern Fed would be utilized. Powell noted repeatedly that the Fed’s decisions were “data dependent” and that it’s “predictive models were broken” – meaning they would simply interpret inflation data as it came through and use it to make decisions.

But at the same time, the market looked to the Fed as though it were an analytical guru that would provide guidance on the future. This was repeated time and again when the Fed would release its “dot plots” each quarter. They would be digested as a sort of roadmap for the future which would then almost always be invalidated by future data or decisions of the Fed.

It all became one very noisy feedback loop. The market justifying what it was doing based on the Fed, the Fed looking at the same data the market was seeing and making calls that were largely from the gut and devoid of any analytical framework. All while justifying what they’re doing because of how public markets reacted. No one was leading.

The bottom line of our critique of the Fed since 2022 has been this:

- It communicates too much – offering ideas that are not rooted in fundamental beliefs, but instead on the news of the day.

- The “dot-plot” is noise at best, bad data at worst (which, to his credit, Powell repeatedly stated).

- Its models – long since broken – have been completely abandoned and there are no clear principles of the FOMC for the public, and the market, to understand.

A New Day?

If Warsh is to be believed, that all changed on Wednesday.

To be fair, he had to do the things a Fed Chair has to do. He released a dot plot. He talked about the Fed’s views on rising inflation. But he also delved into the philosophy the Fed will take under his leadership.

The message? Forward guidance is gone. They’re not doing it anymore. As he said, it’s “not well-suited to the current policy” moment. He added that several members thought “as a general proposition forward guidance isn’t the business we should be in.” The Fed isn’t going to be the market’s economic analyst anymore.

The Fed will continue to release the dot plot. But Warsh is going to exclude his position. No one is going to know how he voted. Why? He doesn’t want the market to make decisions based on his opinion at a particular moment.

But there was one quote that we thought was particularly worth noting. It may end up being more focus group tested garbage. Or it may end up being the true distillation of the Warsh Fed. In many ways, we hope it’s the latter. No matter what, it’s notable for just how different it is from the Fed we’ve had for the last 20+ years:

“I think financial markets perform best when they react to incoming data. I think financial markets work less efficiently when they ask a question: How will the Federal Reserve react to that incoming information…Financial market prices are probably the most important source of information to guide central bankers. But when all the financial markets are doing is reflecting back what we’ve said, then we’re taking the most important source of information and being blind to it.”

That’s it. That’s what we’ve been saying for years. It’s the “circular sentiment firing squad.” According to Warsh, he’s pulling the Fed out of the circle. They’re going to do their job. They’re going to report on it. But they’re not going to feed into the information bonanza that is the market.

Can they do it? We’ll see. Some habits are hard to break. But the message on Wednesday was refreshing, even if the market didn’t want to hear it. Let’s hope it continues. The Fed’s job is to lead – not to follow the market it’s supposed to guide.

Sincerely,