The Weekly Insight Podcast – The Chokepoint (Revisited)

Editor’s Note: Due to travel schedules, this memo was drafted late Thursday. Needless to say, Friday was a whole other story. Equity markets were off hard on a couple of key issues:

- A very strong jobs report shifted the expectations for Federal Reserve rate decisions. The broad expectation is now tracking to rates increasing by the end of the year – not what the market was hoping for.

- Combine that with trouble in cryptocurrency (hitting a low below $60,000) and profit taking in tech stocks ahead of the SpaceX IPO (see last week’s memo). The impact was significant. The S&P was off over 2.5% and the NASDAQ was off over 4%.

We’ll spend more time on that as we see how things shake out next week. But we wanted to lay out the context of the memo below. One day pullback or not – the issues laid out in the following pages remain important to understand and monitor as we head into summer.

Over three months ago, the morning after the United States started bombing Iran, we wrote a memo called “The Chokepoint” discussing the economic ramifications of a hot war in the Persian Gulf. And – more specifically – the impact which would be felt if Iran effectively closed the Strait of Hormuz.

We were writing it hours into one of the most significant global conflicts in the last decade and trying to understand the economic effects. Information was scarce. What we didn’t know then was how much of it we’d get right or how little the market would care.

Over the next month, the market reacted as you might imagine. Lots of volatility. Downward pressure on equities – especially overseas. Interest rates crept up. And the defining driver of market sentiment was whatever was said from the podium – or the Truth Social account – of the White House.

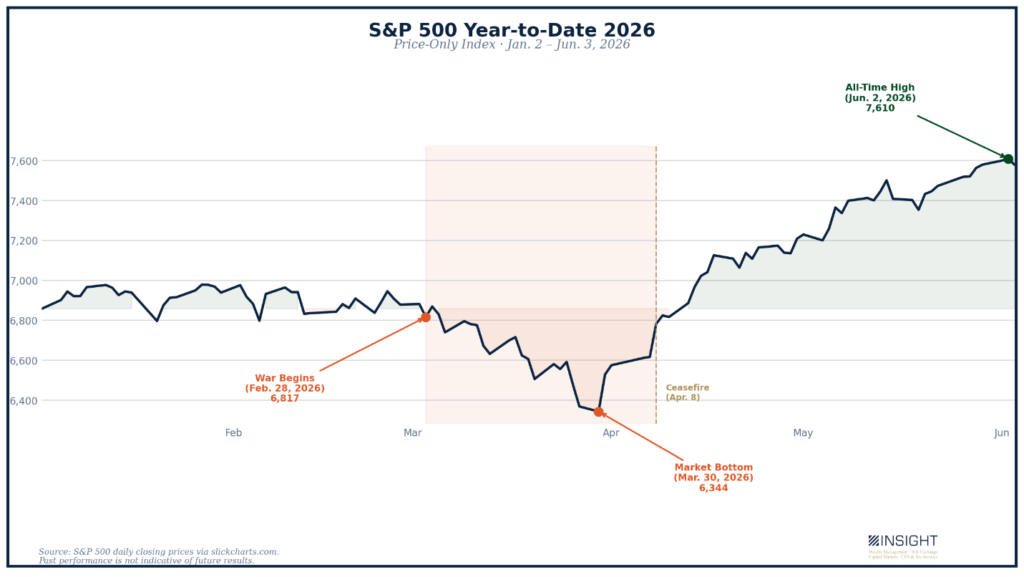

Which brings us to March 30th. The conflict has now been ongoing for 30 days. The Strait is closed. The S&P 500 is down 7.8% from the start of the year and 9.1% from its high earlier in the year. The market hadn’t yet reached correction territory, a fact that, in hindsight, says a lot about how much the ceasefire announcement would matter. But the Strait is still closed and shows no sign of reopening.

If you would have sat us down at that moment and told us “Over the next two months, the Strait of Hormuz will remain effectively closed, shutting off 20% of the world’s oil supply for a minimum of three months with no signs of an immediate solution” and then asked us to predict the market’s performance, the chart below would have never – ever – crossed our minds.

Past performance is not indicative of future results.

So much ado about nothing, right? The market thinks so. The ceasefire – in its continually changing forms – has clearly been more than enough for the market at this point. We’re yet to be convinced.

But, if we’re honest, from an economic perspective we couldn’t care less if we’re in a war with a third-rate authoritarian government halfway across the world. A hot war or a ceasefire standoff doesn’t really change the game.

But the Strait of Hormuz is still – effectively – closed. That matters. A lot. And it’s worth revisiting to understand the impacts going forward.

Resilient Oil Markets

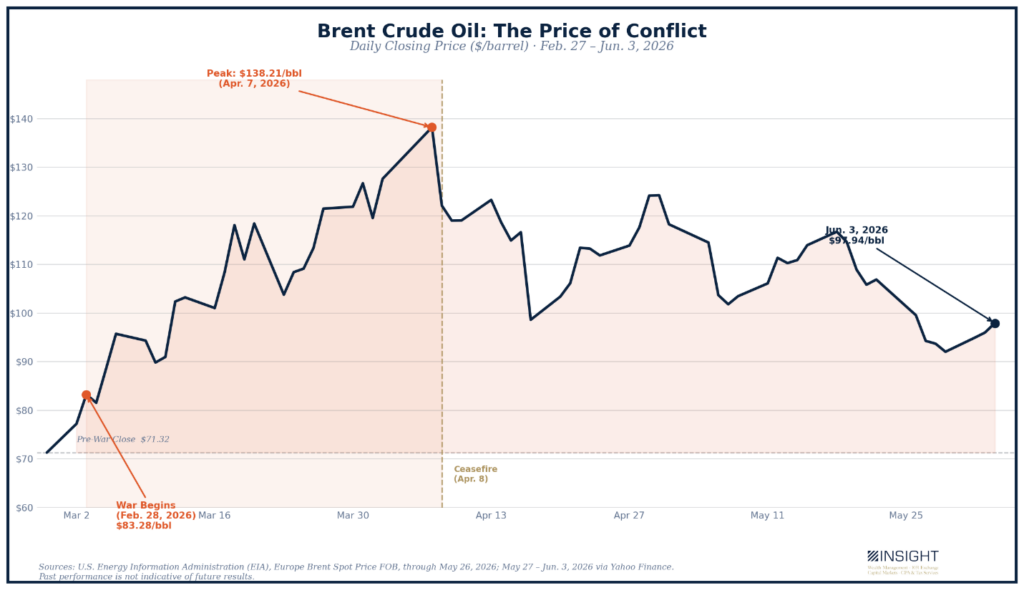

The literature we dove into in early March about global oil pricing was all fairly straightforward: a prolonged closure of the Strait of Hormuz would unquestionably result in global oil prices spiking to $110 – $130 per barrel. A more specific figure – from JP Morgan – noted that regime change events in the region historically caused oil prices to go up 76%. That would have been $118 per barrel for Brent Crude.

And that’s exactly what happened. Until it didn’t.

Past performance is not indicative of future results.

The rise in oil prices – while rocky – reflected exactly what a prolonged closure of the Strait should produce.

But then we entered the “ceasefire” era. And the power of that phrase has had a significant impact on global energy prices. Even after a slight bump up, Brent crude remained below $100 per barrel last week.

Why? The oil industry – especially in the United States – has changed. And the impacts of that are both good and bad.

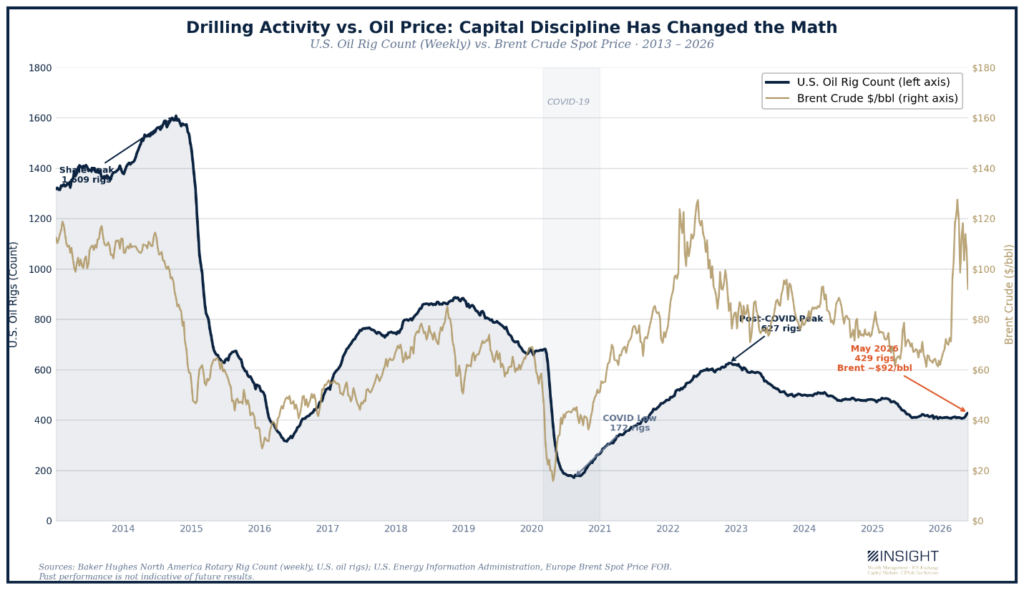

You may recall the last big surge in energy prices that peaked in 2014. The energy industry went crazy. Capex went through the roof. Drilling rigs were running night and day. You could see half of North Dakota from space at night because of all the activity going on.

Until prices dropped and the piper came calling. That expansion was funded with massive amounts of debt and energy producers were on the wrong side of it as prices fell with the inevitable glut of supply.

To their credit, they learned their lesson. And since, they’ve been significantly more focused on putting free cashflow to dividends, share buybacks, and debt reduction – not drilling more holes.

Which is why you may find it fascinating that there are actually fewer rigs drilling in the United States today than there were one year ago when oil prices were a fraction of today’s price.

Past performance is not indicative of future results.

For clients already holding U.S. energy producers, this is exceptionally good news. Their profits are skyrocketing and their input costs aren’t significantly shifting.

For the retail energy consumer – or the world – the news isn’t so good. It’s a world energy market and no significant new production is stepping into the void. Instead that gap is being filled – at least partially – by U.S. energy producers shipping existing production to markets that will pay more. Crude exports from U.S. ports have skyrocketed from 3.9 million barrels per day (b/d) before the war to an estimated 5.44 million b/d in April.

That’s a nearly 40% increase. And it’s being filled by product that is no longer going to domestic uses. It is the reason we’re seeing $4+ at the pump today. U.S. energy producers have been the shock absorber for this major bump in the road. And they’ve been paid nicely for it. But can the impact to the consumer be contained?

The Broader Economic Impact

When we wrote that first memo the day the war started one phrase kept rattling around in our head a version of which has been uttered by countless “experts” over the years:

“A sustained closure of the Strait of Hormuz undoubtedly ends in a recession.”

The dreaded “R” word. As we’ve said repeatedly in these pages, understanding the next recession is one of – if not the – most valuable insight one can have into the markets.

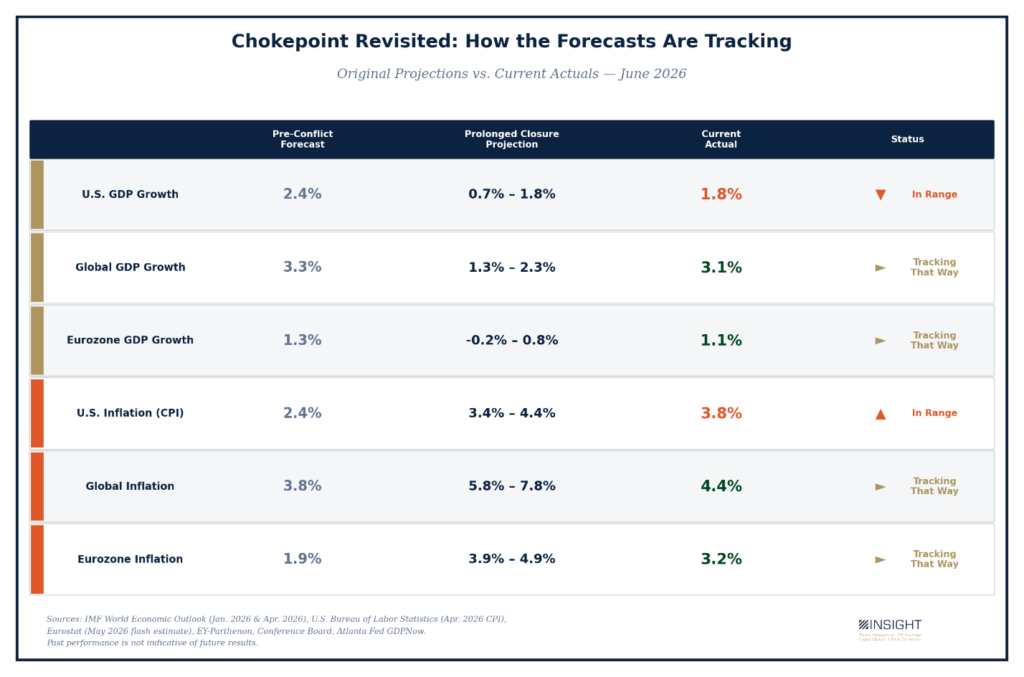

The math we used at the time was fairly simple and long ago defined by economists. Every $10 increase in oil prices meant a 0.1% – 0.3% decrease in GDP and a 0.2% increase in inflation.

We went and reworked that old data to show the impact-to-date compared to the day one projections. It hasn’t been “worst case” because oil prices haven’t spiked enough for that. But the impacts are real. And they’re all trending in the wrong direction.

Past performance is not indicative of future results.

The world economy continues to be in a manageable position. It’s not great – but no one was panicking about 1.8% GDP growth during nearly a decade of sub-2% growth we had in the 2010s. And 3.8% CPI – while higher than desired – is historically normal.

And so, the oil crisis hasn’t materialized like some foretold. But that doesn’t mean it won’t.

So, what happens next? The ceasefire is fragile, energy stockpiles are depleting, and the market has already priced in an agreement between Iran and the United States that isn’t signed.

So far, the market is right. The last three months haven’t killed the economy. But every week the Strait remains closed is a week the margin for error shrinks. The real question is what the next three months look like if the talks with Iran continue to stall. And whether the tools that have worked to this point have the bandwidth to maintain the status quo.

Sincerely,