The Weekly Insight Podcast – SpaceX IPO: Go/No-Go?

In our 14 years as a firm (and many more in this business), there aren’t many things we see for the first time anymore. COVID was one. The collapse of the financial sector in 2008 was one. But most of the day-to-day machinations of the market all rhyme with previous experience.

Over the last month or so, you have all surprised us! Never before have we had this many calls regarding an IPO. There is tremendous interest – both in our client base and throughout the country – in access to the SpaceX IPO.

You asked. So, we went digging. And we have now been able to source IPO shares (more on that later). But before we get there, we’re going to do what we always do in the Weekly Insight and dive into the story – and the data around it – to answer some especially important questions: What are you really buying? What is the historical track record of IPO shares? What does this mean for the broader market?

One important note: We don’t make one-off stock recommendations. It is not the service for which our clients employ us. The information below is meant to educate you on the company, the IPO process, and its logistics. It is not a recommendation to buy (or not to buy) SpaceX shares.

What is SpaceX Actually Selling?

The “how do I get SpaceX IPO shares” question we’ve heard so many times shouldn’t be a surprise. It’s the hottest ticket on Wall Street right now. But what is it investors are actually buying? What is the company today and what does its future look like?

When you think of SpaceX, you need to think of it as three companies: satellite internet (Starlink), space launch services, and SpaceXAI. Let’s look at all three:

Starlink is a wildly successful enterprise. When Elon Musk started talking about providing satellite internet service – at high speed – for the masses and in remote areas, no one thought it could be done. But he’s done it. And done it at scale.

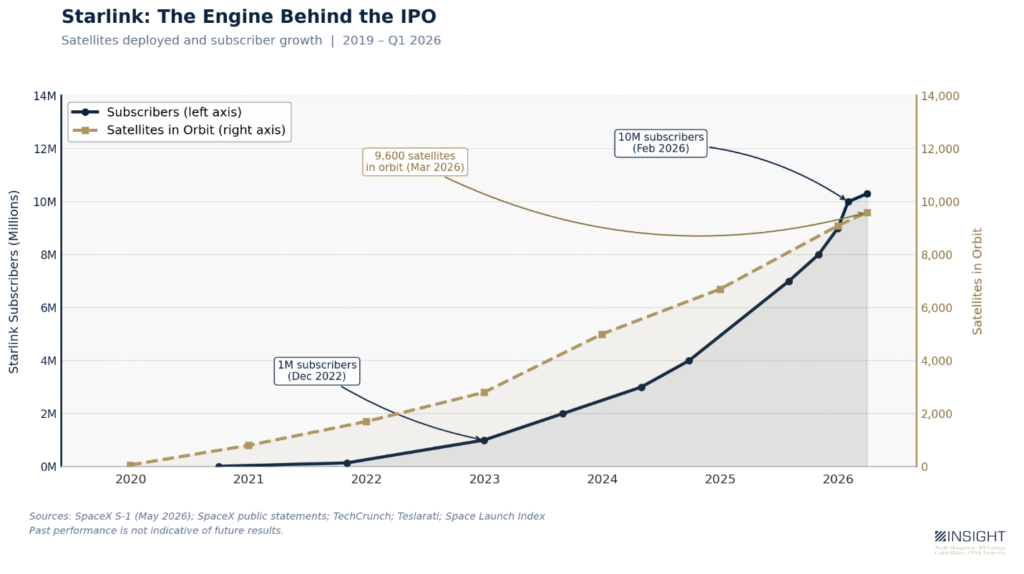

In the last seven years, he’s put 9,600 satellites in orbit and now has over 10.3 million Starlink customers worldwide.

Past performance is not indicative of future results.

You’ll note that over the last few years the trend is clear. Yes, they have to put more satellites in orbit, but the customer base is scaling faster than the equipment needs. Three years ago, they had 1MM subscribers and roughly 3,000 satellites. Today the subscriber number has grown 10x while the satellite needs have only expanded 3.2X.

And it’s already profitable. According to the S-1 filing for the IPO, it generated $4.42 billion in operating income with adjusted EBITDA of $7.17 billion on revenues of $11.39 billion. Those are software company margins. And each new customer just adds high-margin recurring revenue at near-zero marginal cost.

That is, however, where the profitability ends for SpaceX. The launch business – which is by far the piece of the business which gets the most attention, is losing money. In fact, it has lost $662 million in Q1 alone. That’s certainly necessary to make Starlink work – but it’s notable.

And then there is SpaceXAI. This was rolled into SpaceX earlier this year in preparation for the IPO. And it really includes four things:

- Grok: This is Musk’s competitor for ChatGPT, Claude, etc.

- X: Formally known as Twitter, this is the social media component of the company

- Colossus: A supercomputer facility in Memphis, TN

- Cursor: This is a deal Musk made earlier this year to buy Cursor, an AI coding tool. The purchase will be finalized after the IPO.

It’s no insult to say SpaceXAI is significantly unprofitable. AI is still in its infancy, and all of the major players are in the “spend money to make money” mode. OpenAI lost $9 billion in 2025 and that number is expected to balloon to $74 billion in 2028 alone before they pivot to profitability in 2030.

But we have to note, the same goes for SpaceXAI. It lost $6.4 billion last year.

So, in the end, we get a company that has adjusted EBITDA of $6.584 billion. But that’s adjusting for all of the expenses like stock-based compensation, satellite depreciation, infrastructure CAPEX, etc. The cash number? SpaceX lost $4.94 billion last year.

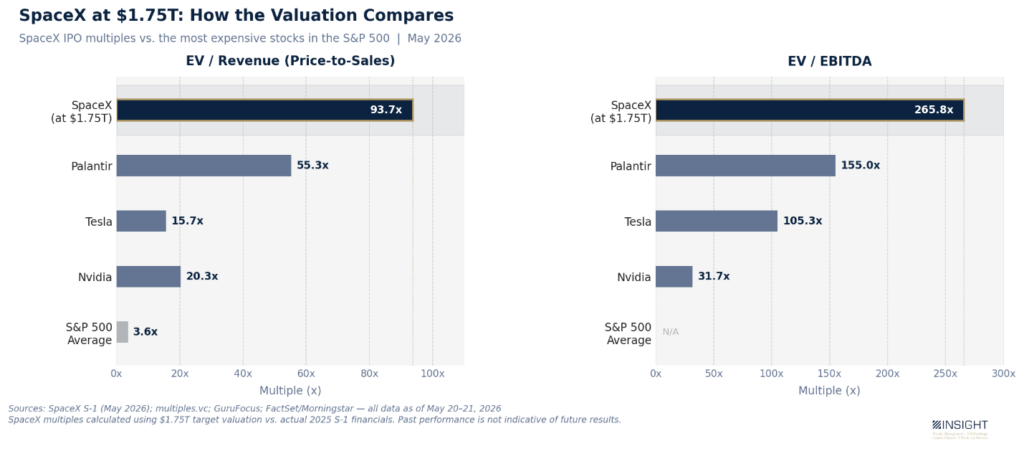

And so, this is a growth play. And an extremely expensive one when you look at the $1.75 trillion expected listing valuation. Since there are no earnings, we can’t calculate the multiple. But we can look at other multiples:

Past performance is not indicative of future results.

Key Man Risk (or Benefit?)

What do you say about Elon Musk? He is a genius. He’s a rebel. He’s wildly popular with some. And wildly unpopular with others.

This can cut both ways in this scenario. From a risk perspective, you need to ask yourself, “what is SpaceX without Elon Musk?” Can it thrive? Is it worth the previously mentioned valuations?

On the other side, Musk fan or not, we all must admit that his fans do buoy his companies’ valuations. Just look at the chart above. Even after all of the drama about Musk and his electric cars, and the fact that Tesla still isn’t terrifically profitable (+$7.3B net income in 2025), it’s still one of the most expensive companies in the world. That magic may yet work for SpaceX.

The good news is that SpaceX isn’t just Elon Musk. You’ve probably never heard the name, but Gwynne Shotwell has been the President and COO of the company since 2008. She runs the day-to-day operations and has been there since the beginning. She’s employee #7. From a key man perspective, there is bench depth behind Elon.

But from a power perspective, there isn’t. Musk will control 85% of the voting shares even though he will only own 42% of the equity. To force a vote on his power at the company you need to hold $52.5 billion share value. That’s a huge hurdle if problems arise in the future. Investors aren’t buying a seat at the table. They’re buying one in the stands.

The IPO Trap: FOMO

FOMO (Fear of Missing Out) is a real thing. And it’s a very real thing when it comes to investor behavior. And IPOs are a place where we can see with extreme detail the impacts of it.

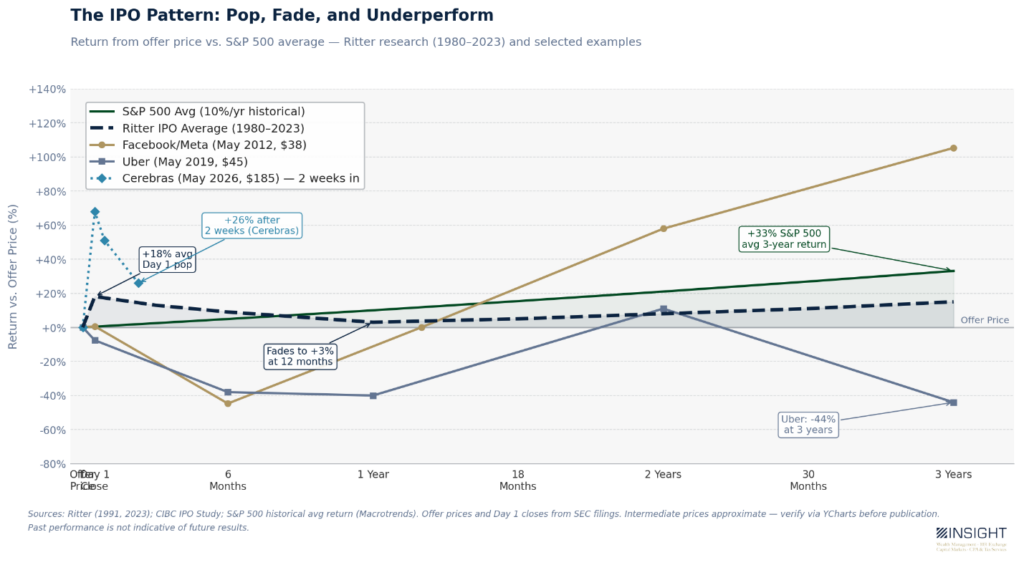

Dr. Jay Ritter, a professor at the University of Florida, has been studying IPOs for a long time. His research in this area started with a 1991 study called “The Long-Run Performance of Initial Public Offerings” and he’s continued to track and update this data ever since.

What Ritter found was a very repeatable process: a big pop on Day 1 and significant underperformance over the next three years. Compared to the market, IPOs outperform by 18.1% on day one, but underperform by 4.8%, 8.1% and 19.6% over the next 1, 2 and 3 years.

We have a really good example of this right now. Cerebras, an AI company, went public earlier this month. On May 14th it went live at an IPO price of $185 per share. The stock opened on public markets at $350 per share! By the end of the day, it was down to $311.07. By last Friday, it was down to $233. It’s still above the IPO price, but it’s coming back to earth quickly.

This is a common story. Facebook and Uber are two prominent examples. We shouldn’t be surprised if the largest and most hyped IPO in history has similar characteristics.

Past performance is not indicative of future results.

Mega IPOs and Market Cycles

We’ve heard a lot of comments and read a lot of stories that start something like this: these are the IPOs that happen before the market crashes. The most cited is the Visa IPO in March of 2008. But that’s quite a stretch, considering the Visa IPO happened after the market peaked in late 2007.

Maybe mega-IPOs are a signal. Or maybe the timing is coincidental.

What can’t be denied, however, is that the pipeline for mega-IPOs is hot right now. SpaceX is just the first of three massive IPOs happening in the coming months. Open AI filed an S-1 with the SEC targeting an IPO in September with an expected valuation over $1 trillion. Anthropic, the maker of Claude, is targeting an October IPO with a valuation of at least $965 billion.

That’s $3.75 trillion in just three IPOs. Those IPOs intend to raise ~$200 billion. For perspective, the entire U.S. IPO market in 2025 raised $45 billion.

The problem is this: the money has to come from somewhere. And for the last few years, investors have been getting their AI exposure via proxy. Maybe they’d buy some shares in Nvidia to get access to the chips that are powering it. Or they’d buy Google because it owned part of Anthropic. Or Microsoft because it had a stake in OpenAI.

So where do those dollars come from? One can imagine institutions – and individual investors – taking from those proxy positions to allocate directly to SpaceX, OpenAI, and Anthropic.

The result? It might be a bit of a wild ride for the market as it figures out how to swallow this huge new allocation directly into artificial intelligence.

The Bottom Line: How Do We Buy It?

This is what you all read this far for, correct? Let’s get into it.

We have been accepted into Schwab’s allocation for SpaceX shares (trading under the symbol SPCX). As such, we will be allowed to indicate interest in the shares for you in the coming days. Here is the important information:

1. The window to indicate interest to Schwab is June 4th (this Thursday) through June 10th (next Wednesday). Right now, we anticipate an offering price in the range of $180 – $210 per share. The problem? That’s an educated guess without any hard info. We won’t have a real number until after the window to indicate interest closes.

To indicate you want to purchase shares, please do the following:

-

- Email Alex Perez at aperez@insightwealthgroup.com (and cc your advisor) with the number of shares you’d like to purchase and the account you’d like to do it in.

2. Schwab will have a limited allocation of shares. They cannot guarantee everyone will be allowed to purchase their requested allocation. But it is their intent to make sure every interested investor will have access to at least one share.

3. The IPO shares can be purchased in most types of accounts. But they cannot be purchased in 401(k) accounts, corporate accounts, pension trusts, etc. If you’re trying to purchase it in a disallowed account type, we’ll let you know.

4. If we have the paperwork on file to execute this on your behalf, that is all you’ll need to do. If not, we may need to send you a form called a WPFA to give us that authorization.

5. On June 12th, the shares will be purchased in the appropriate account. If trading is necessary to make funds available for the purchase, we will handle that for you.

Two BIG caveats. First, we will be handling this as a client directed trade. We’re happy to handle the execution, but this will be your call, not a piece of our broader managed strategies.

Second, they are your shares, and you can do with them what you like. As you may have seen in the chart above, selling on Day 1 may be tempting. But we’re not the only ones noticing the trend.

As such, Schwab can’t make you hold onto the shares. But they provide clear notice in this process that if you don’t hold the shares for 31 days, they can disallow you from participating in any future IPOs on their platform. Additionally, if a lot of Insight clients execute such a move, they can disallow Insight from participating as a firm in the future as well.

We hope this has given you some valuable info to chew on as you consider this interesting opportunity. As usual, we’re always here and happy to chat if you have any questions.

Sincerely,