The Weekly Insight Podcast – The Space in the Middle

The thing about writing market commentary is that you can find statistics to justify pretty much any position you want to take. Want to argue the consumer is healthier today than they were a year ago? That’s easy – did you know credit card balances are down from their highs?

Or do you want to convince your readers the consumer is in peril? You can use the same stat: credit card balances are now $1.252 trillion, up nearly 63% from pandemic lows.

Just one data point can write two vastly different headlines in the hands of a skilled writer.

But it’s the space in the middle that interests us the most. And the space in the middle today is wide. On one side, there are those predicting disaster in the economy. On the other is the market – which until Thursday, was on a tear setting new all-time highs.

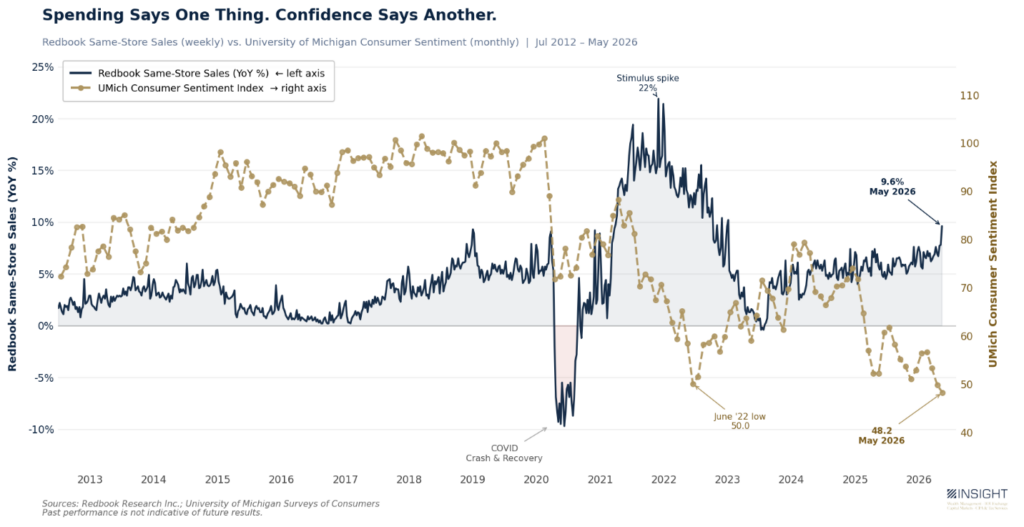

No set of statistics better tell the story of this conflict than consumer sentiment (how consumers say they feel about the economy) and Redbook same-store sales data (how they’re acting with their money).

Past performance is not indicative of future results.

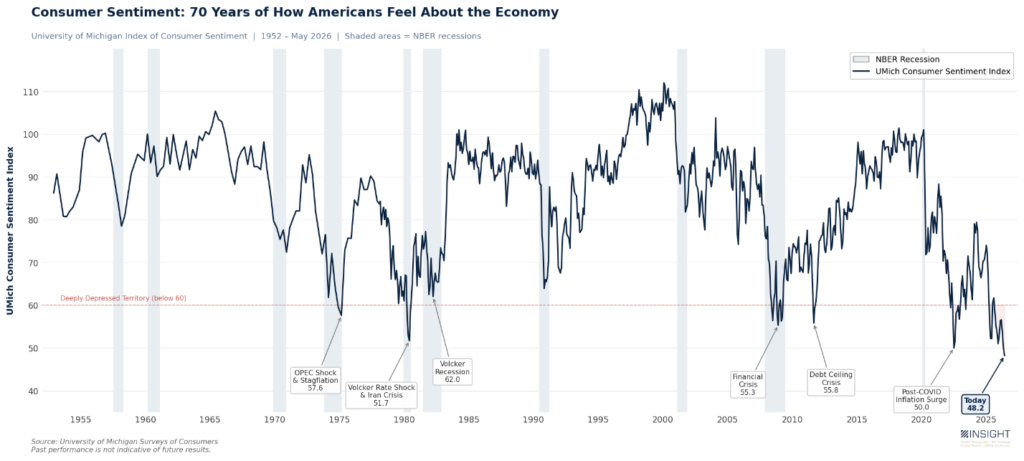

Let’s understand the story these two lines are telling us right now. First, let’s look at Consumer Sentiment. This is survey data taken by the University of Michigan. They ask a series of five questions to gauge how consumers feel about the economy today and its future prospects. They’ve been running this same dataset since 1952. The May 2026 reading is the lowest in history. Never before have consumers “felt” so bad about the current economic condition.

Past performance is not indicative of future results.

You’ll notice above the shaded areas which represent recessions. It shouldn’t be a surprise that those recessions all tie directly to significant drops in consumer sentiment. That’s not to say that every drop in consumer sentiment is tied to a recession – but the majority of big drops happen during one.

Until the last four years. We saw a massive drop post COVID to the previous all-time low. No recession. And – so far – no recession this time.

Spending and sentiment – however – aren’t the same thing. But historically, they rhyme. And you can understand why: if consumers feel bad about the economy, they’re going to be less likely to spend money.

The Redbook same store sales data measures the year-over-year growth of spending at specific retail locations. The data isn’t nearly as old as the Consumer Sentiment survey. But you can see a clear trend – pre-2025 – of the two following each other. Until they didn’t. Since early 2025 they have been moving in distinctly opposite directions. Last week that spread exploded when Redbook jumped from 7.8% year-over-year growth to 9.6%.

Weve’ only seen these two lines diverge in such a manner once before – immediately after COVID. And there was a very compelling excuse at the time: pent up demand from COVID inventory problems and excess cash from COVID stimulus. Today, those factors don’t exist.

What Explains the Divergence?

You know the line: 70% of the U.S. economy is consumer spending. The obvious takeaway is that more consumer spending (i.e., Redbook UP) is good for the economy. In general, that’s true.

But if we’re interested in the “space in the middle” we need to ask ourselves why consumer spending is spiking at a time when confidence is falling. There are four main arguments:

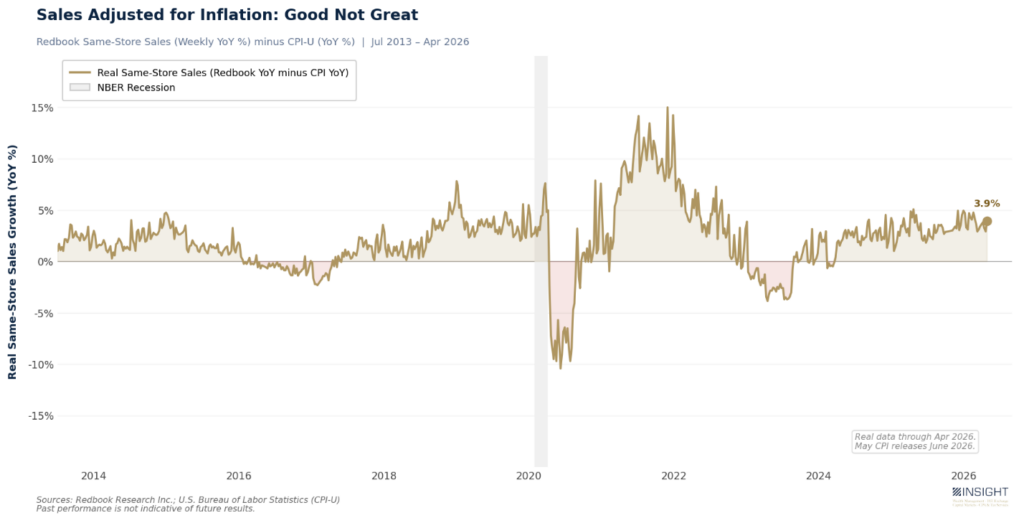

1. Inflation

We can hear the argument now: “Of course spending is up…everything is more expensive!”

There’s validity here – but it doesn’t solve for the whole problem. Yes, things are more expensive. But Redbook is measuring spending year-over-year and is showing it has grown 9.6%. Inflation is higher than many would like – but to this point, it’s not high enough to wipe out that sales growth.

Past performance is not indicative of future results.

If you look at the data through April (our last CPI read) what you see is that sales growth – when adjusted for inflation – still remains relatively strong. It’s not as good as we saw back in the post-COVID days, or even the end of the 2010’s, but it’s much stronger than we saw in times of relative economic strength, like the mid-2010s. And no one was talking about recessions then.

VERDICT: Not True

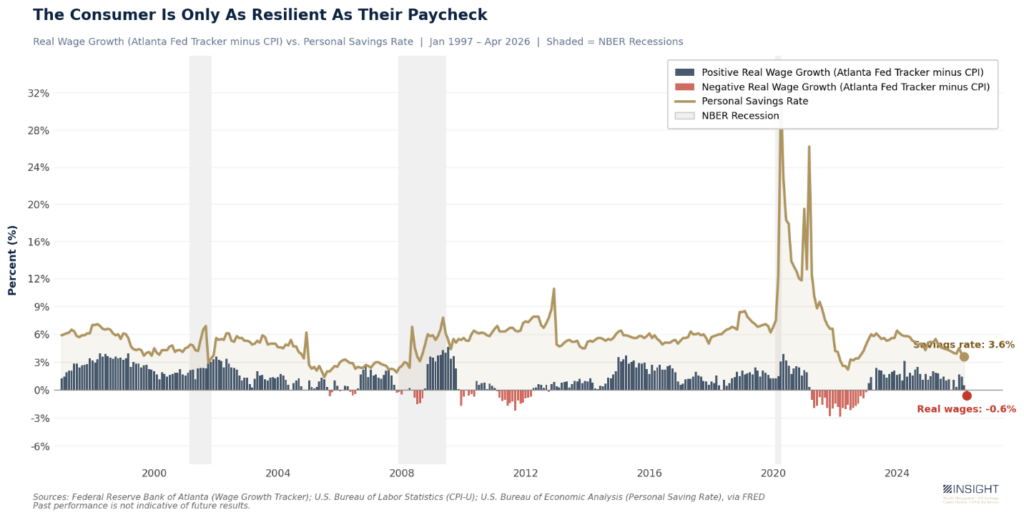

2. The Resilient Consumer

This is the stock trader’s answer right now. It goes something like this: “Yes, things are rougher than they were. But consumers are going to consume. It will all work out.”

That’s been true in the past. But the consumer needs money to spend. And a few things are happening right now that must be understood.

First, real wages (wage growth minus inflation) are compressing fast. In January it was 1.7%. By April, it had dropped to -0.6%.

And with wages, so goes the money people have to set aside. The savings rate failed to meaningfully recover from the 2021 – 2023 drawdown and is now approaching those lows again. Against a backdrop of newly negative real wages, that’s worth monitoring.

Past performance is not indicative of future results.

VERDICT: Resilient for the moment…But worth watching

3. Stocking Up

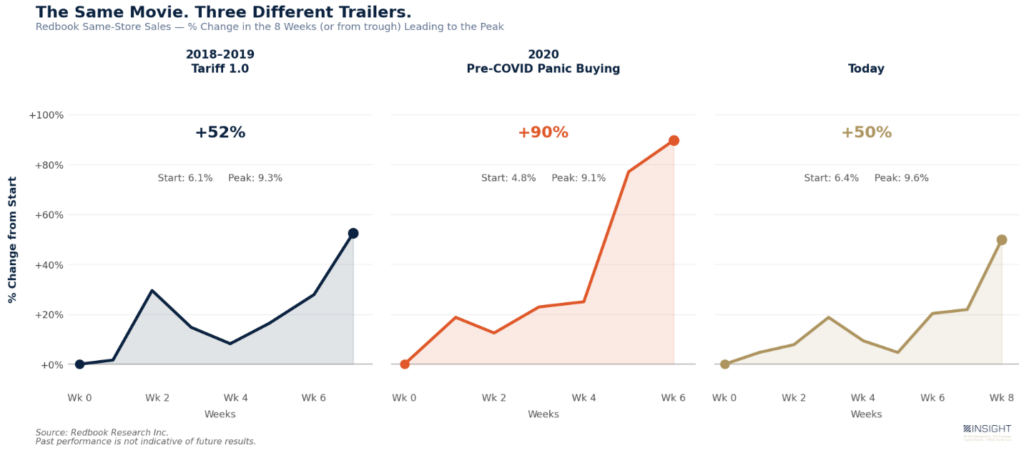

There’s another curious thing to look at in the spending data. The spike we saw last week continued an aggressive move in same-store sales. On March 10th, they hit an inter-period low of 6.4%. By Tuesday, they were at 9.6%. That move – 3.2% – is a 50% move in two months.

When we were looking at the Redbook chart, we saw another similar spike: right before the collapse in spending caused by COVID. In one month, same-store sales nearly doubled from 4.8% on February 11th to 9.1% on March 24th.

We all know that was a crazy time. But it was also a moment where consumers acted in great self-interest. Why? They were genuinely concerned that goods would not be available, so they went out and stocked up (remember toilet paper?).

Could that be happening again? Is the consumer concerned about the onset of inflation and/or economic troubles and using this moment – and the last of their savings – to buy up what they need?

It’s not that explicit. No one has the “world is ending” fear we did then. But, in 14 years of Redbook data there has only been one other time when we’ve seen such a jump: 2018 during the first “Tariff War” when consumers were panicked about rising prices.

Past performance is not indicative of future results.

An economic disaster didn’t happen in 2018 as the tariff concerns eased. 2020 was a disaster all its own. But the consumer was preparing for something in each situation. What are they preparing for today?

VERDICT: Plausible

4. K-Shaped Spending Collapse?

This is the most obscure of these options.

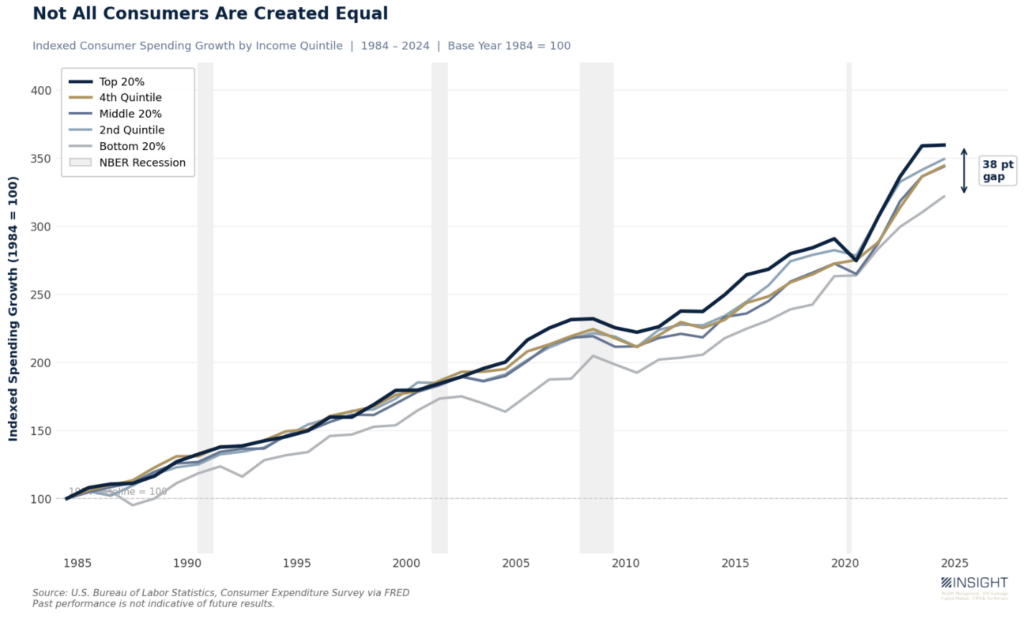

You’ve heard us discuss before the difference between the spending of the wealthiest Americans and the less well off. It’s a significant spread. And there is real truth to the fact that the highest wage earners are the drivers for our economy.

Past performance is not indicative of future results.

As of 2023, we set the record for the largest gap between the top 20% and bottom 20% for spending. The 2025 numbers aren’t out yet – but you’ll notice the flattening that happened in 2024 for the top 20%.

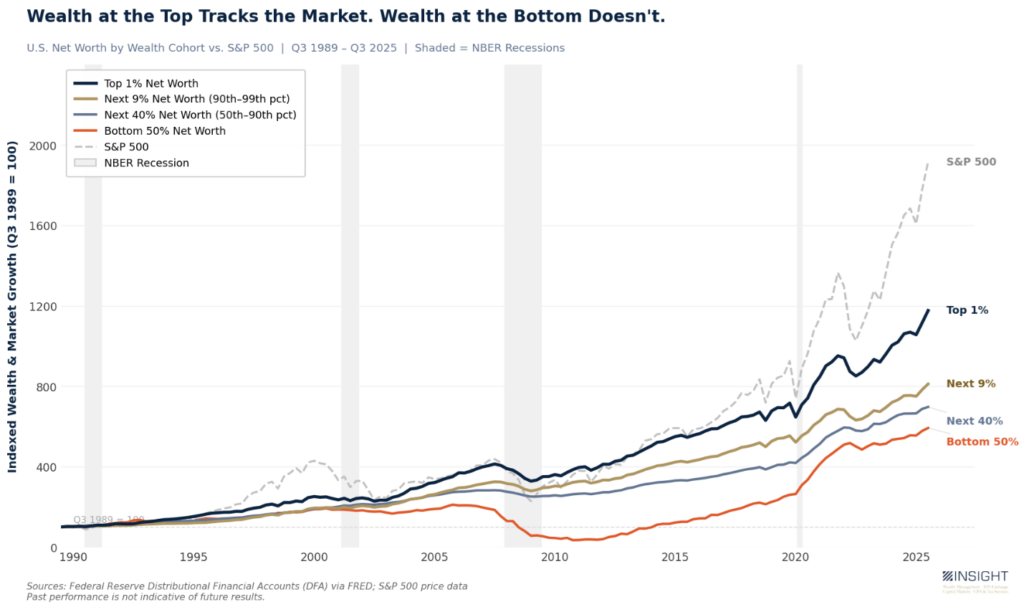

One of the things we know about the spending of the wealthiest Americans is it is significantly tied to wealth – not just income. And wealth is created by things like stock market performance. The correlation is easy to see when you plot the net worth of the top earners vs. everyone else in correlation to the S&P 500’s performance.

Past performance is not indicative of future results.

Yes – all groups generally track. But the higher the income ladder you go, the more direct correlation you see to equities. The peaks and valleys are steeper, but the benefits are substantively larger.

So, here’s the “space in the middle” moment: wage growth has kept the consumer in this game for a while, even with pressures on prices. But as wage growth has tailed off, spending has been buoyed by wealth. It’s the classic “K-Shaped” problem. But if wealth were to correct (i.e., the stock market!), there’s nothing left to drive consumer spending.

Which brings us to Friday. The market had a difficult day. The worst since March. But it was the bond market that made us sit up straight – specifically the 10-year treasury yield which breached and held above 4.50%. That is a risk to equity prices.

Why? The “equity risk premium” (ERP). It is the difference between the earnings yield for the stock market and the risk-free rate of return (i.e., 10-year treasury). If you calculate it using the S&P 500 forward earnings multiple at 21.5x, the yield comes to roughly 4.65%. Other calculations – like the Shiller CAPE – put that number much lower.

The 10-year closed Friday at 4.59%. That is shrinking the equity risk premium very quickly. And it will force investors to consider their options. Why would you take the risk of the stock market if you can get similar economic benefit from risk-free fixed income? That could create a correction. And a correction will certainly impact the spending from those that drive it most.

VERDICT: Not true…yet. But the most concerning.

Living in the Space in the Middle

There’s a temptation – even an expectation – to wrap up an article like this with an answer. OK, Insight…what do we do? We could stake out a bold position and then, when the winds shift, pick another one more in favor.

But it’s not that simple.

Are things disastrous? No. Equities are literally one day off an all-time high. But there is enough bad potential in this moment – Iran, inflation, shrinking wages – to require us to remain vigilant.

Are they wonderful? No. The consumer is genuinely concerned about the future. But the Redbook number is real. Spending is happening. We’re not here to tell you the economy is collapsing – because it isn’t.

What we are telling you is the mechanisms that drive spending (and our economy) are shifting. A year ago, wages were driving spending, but they’re now negative in real terms. Today it’s savings, but they’re dwindling. If the wealth that underpins it all – i.e., the stock market – starts to correct, the picture looks very different very fast.

That’s the space in the middle. Not a disaster. Not a green light. A moment that requires us to understand how things are working, not just that they are.

Sincerely,