The Weekly Insight Podcast – Avoiding the Hidden Inheritance Tax

We’ve spent considerable time in these pages over the last several years talking about all that could go right or wrong with public markets. But, if you’ve been paying attention, you’ve heard us say that no one – not us, not the big wire houses, not the Federal Reserve – actually knows. The only difference is we’ll actually say it!

There are – however – a few things we do know: we’re all going to die and we’re all going to pay taxes.

Yes, there is still some uncertainty there. When will you die? Will you get hit by a bus tomorrow or pass away in your sleep in 50 years? How high will taxes go?

But, as the saying goes, death and taxes truly are the only two things promised to us in this world.

Which brings to mind a question: why do people spend so much time worrying about the things we think might happen and so little time thinking about the things that will happen?

And so, we’re turning a new page with The Weekly Insight. Our discussions about what moves markets and how we’re responding won’t go away. But we are going to spend more focused time – at least once a month – addressing real world financial planning scenarios. Our goal is to make you think just a little bit deeper about the long-term planning that matters most.

This series, over the next several months, will be focused on GOALS. And from those goals, we hope to give you a few actionable ideas that may fit your scenario. Let’s dive in.

What REALLY Is Your Goal?

In the financial planning process, this is always the hardest question. Nearly every family we have the pleasure of working with knows how to make money. And they know how to save it. But very few actually know what they want to do with it. Or maybe it’s better framed as why they worked so hard to save it in the first place.

We frequently hear the two easy answers: “We’re doing this for retirement.” Or “We’re doing this for our kids.” Those are – of course – completely legitimate reasons. But they’re not always the actual answer.

What does “doing it for our kids” look like? Is it leaving them with a big pile of money when you die? Is it helping deal with current needs like health concerns or job losses or education? Or is it giving them money now – while you’re alive – so you can all enjoy it together?

What does retirement look like? Other than not having to work anymore, not many have a true plan. And in some cases, not having a plan is the plan. Simply not having to worry about anything is a goal for many. But how do you want to fill your time?

Or is the goal to leave a legacy? Is charity your priority? Is there a particular cause that matters most to you?

The real work of financial planning isn’t happening until you know the main goal(s). And until your advisor understands them as well.

Taxes Change the Plan – Not the Goals

When we first meet most of our clients, the “goal” is simple: take this sum of money that we’ve spent our time, effort, and passion to save and make it grow. Some want it to grow as fast as possible. Others want a defensive approach. But growing it is the goal.

But once you start to understand the real desires for the funds, how we get there may dramatically shift the strategy. And that, in many ways, is where the second certainty comes in: taxes.

You all know the saying well: taxes are the single largest expense of your lifetime. So, if you’re not planning with taxes at the forefront of the strategy, you’re leaving a lot on the table. How we work with clients to manage those tax impacts is – almost entirely – one of the most impactful pieces of the puzzle.

You’ll see a lot of focus in this series on how the tax component can significantly shift the outcomes of any given plan. And, more importantly, how to make sure that shift is to your benefit.

GOALS: The Inheritance Planners

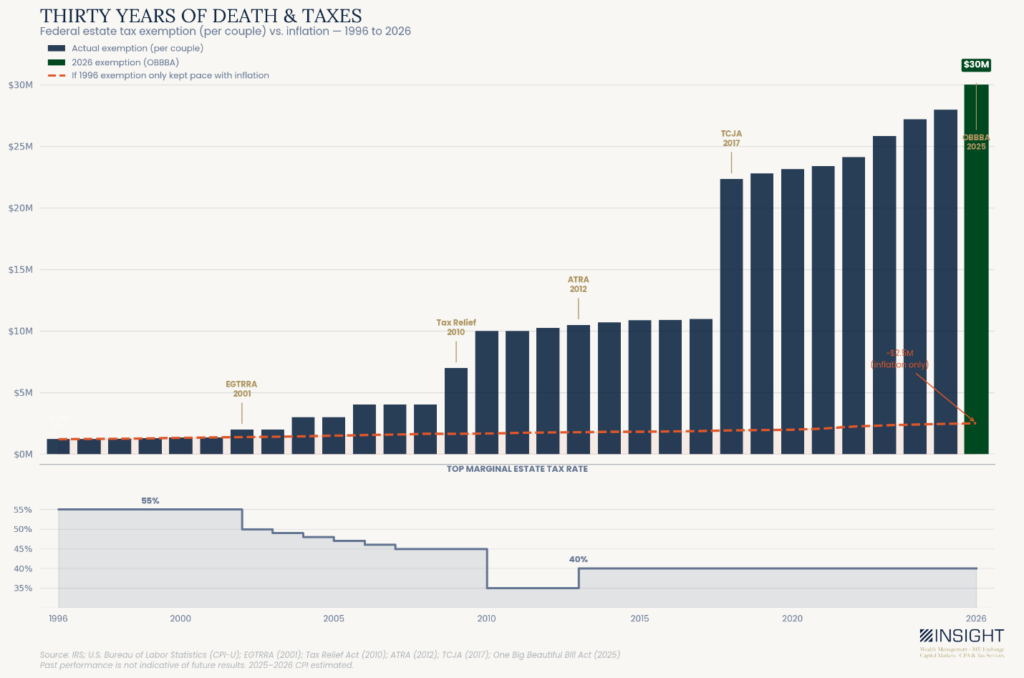

If we had to pick the most common goal we hear, it would be passing money along to children via inheritance. It is a noble and time-honored goal. And it is actually easier today than it was 30 years ago. The Federal inheritance tax limit sat at $600,000 per spouse in 1996, meaning any assets greater than $1.2 million per couple would be subject to estate taxes. And the Federal estate tax rate was an astronomical 55%.

But that estate tax exemption has skyrocketed in the last 30 years, even as the rate came down to 40%. The One Big Beautiful Bill made those changes permanent – or at least as permanent as any law can be in Washington.

Today the estate tax exemption is $15,000,000 per spouse/$30,000,000 per couple. And that’s not just a function of inflation. $1,200,000 per couple in 1996 is worth roughly $2,500,000 today. The estate tax exemption is twelve times higher today than it was in 1996, even after adjusting for inflation.

Past performance is not indicative of future results.

These policy changes have made estate planning significantly easier for families. Current estimates show that only 1,500 – 2,000 deaths each year in America (out of over three million) will trigger an estate tax payment. Less than 0.07% of families are affected.

The estate tax may be the one the media loves to dwell on, but it is not the real issue. The tax threat most families will actually face isn’t written in the estate code. It’s sitting inside your retirement accounts. And it will greatly affect those who place passing assets to heirs as a top planning goal.

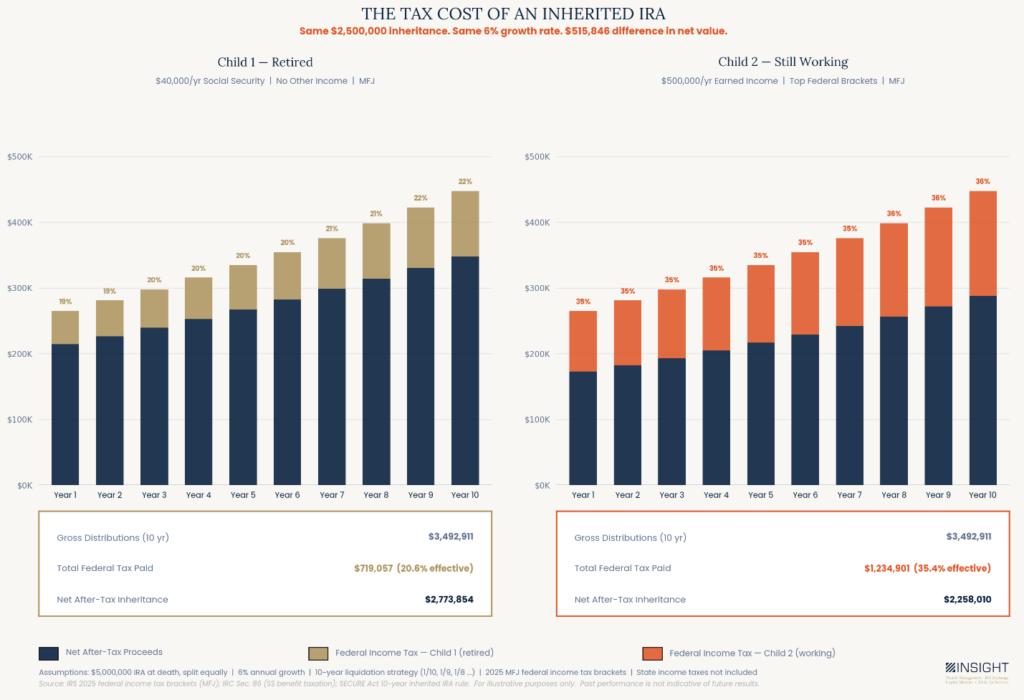

Let’s use the example of a patriarch – aged 80 – who has $5 million in IRA assets and two children as beneficiaries when he passes away. Both will – in theory – receive $2.5 million.

Current law gives them 10 years to withdraw the funds from the IRA, and those withdrawals are taxable as ordinary income. The common logic is to take those funds out in a regular manner over the 10-year period to reduce the impact on income taxes.

Let’s take it a step further and make some assumptions about the kids. Let’s say that both are married. One is retired and has only $40,000 per year in Social Security income. The other is still working and is highly successful with an income of $500,000 per year. Their outcomes are VASTLY different. And it’s all because of taxes.

Past performance is not indicative of future results.

The patriarch certainly didn’t intend to give one child $515,844 more. But what else could be done?

There is another way.

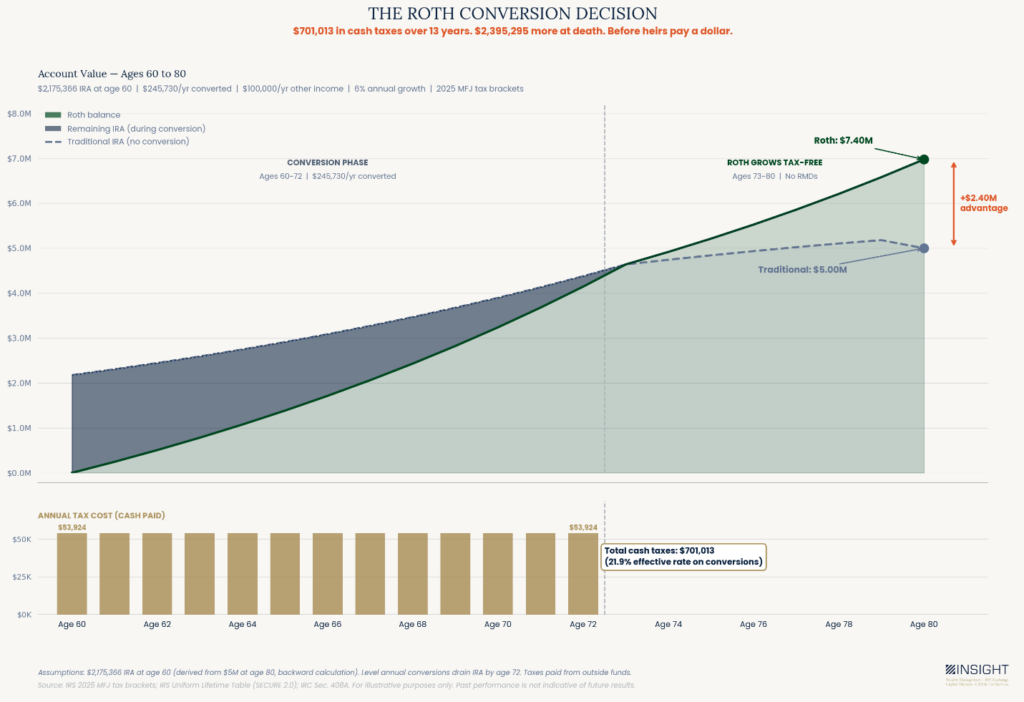

Let’s rework the assumptions. The 80-year-old patriarch retired at 60. He never needed his IRA money but took out Required Minimum Distributions (RMDs) as prescribed by law. The growth rate stayed stable at 6%. If you work that backward from a $5,000,000 balance at age 80, you get a balance at retirement of $2,175,366.

Now let’s change his strategy. Instead of just growing the account, let’s assume he started using the time between retirement (age 60) and RMD age (73) to do Roth Conversions. No one wants to pay taxes voluntarily. It sounds backwards, until you run the numbers: for just under $54,000 a year in taxes, he is passing along an asset that is worth 48% more than having done nothing!

Past performance is not indicative of future results.

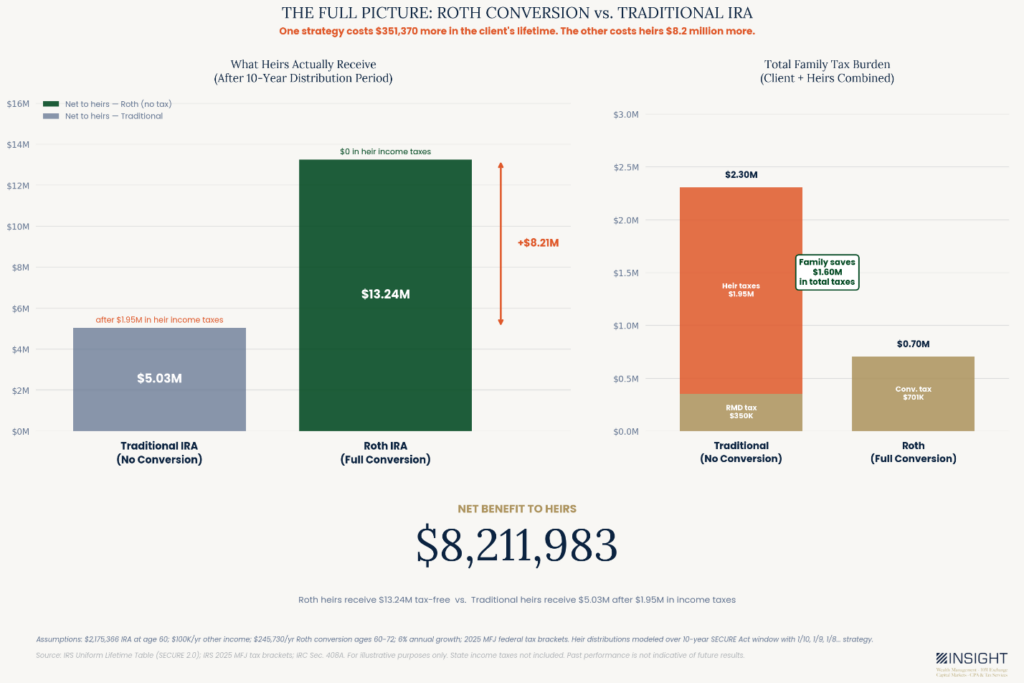

And here’s the fun part: we all know the inheritance is tax-free for the kids when it comes from a Roth. But the kids still get 10 years to distribute the funds. If they use that time to let it compound for inside the Roth before withdrawing it the results are staggering. The total benefit from the account is more than $8 million more than the original plan. $1.6 million of that comes from total tax payments that never need to be made.

Past performance is not indicative of future results.

$8.21 million extra. On a $5 million potential inheritance.

But there is a finite window to take advantage of these rules. Retirement to age 73. That’s the window for people to consider this strategy. It’s the only time in a high-income earner’s life when their income is substantially lowered. And when the window closes, it’s too late.

So, if this sounds like you, now is the time to plan. It could be worth millions to your heirs.

Sincerely,