The Weekly Insight Podcast – The Great Rebalancing: Part II

Editor’s Note: The Weekly Insight will be taking next week off due to the Fourth of July Holiday (Happy 250th, America!). Additionally, our offices – and the market – will be closed on Friday, July 3rd. We look forward to being back in your inbox on Monday, July 10th.

There is always drama happening in the markets. 2026 is no different. Wars, mega-IPOs, energy volatility, the advent of AI, new Fed chairs. It seems like…a lot. And it’s easy – and understandable – for investors to throw their hands up and just cry uncle.

But generally speaking – and especially this year – the drama is just noise. Does it mean something in the short-term? Of course. Should it be watched in the moment and understood for what risk and opportunities present themselves? Absolutely. But they will not determine the future of your portfolio 5+ years from now.

Underneath the hood, however, there tend to be some bigger trends happening that really do matter. They’re not nearly as flashy – but they can have significant impacts on portfolios.

Just over four months ago, we wrote about one of these in a memo called The Great Rebalancing. It’s worth another look. Because what we were calling out four months ago is now an eight-month trend. It’s real. And it’s not getting a lot of press. But it is impacting portfolios today in ways most investors don’t understand.

The Shine Is Off the Mag 7

“The Magnificent 7 is now a drag on the market.” – The Great Rebalancing, February 2, 2026

February 2nd seems like a lifetime ago. Just over three weeks after this memo was written, bombs started falling in Iran. No one was focused on valuations. The energy story took over and markets tumbled.

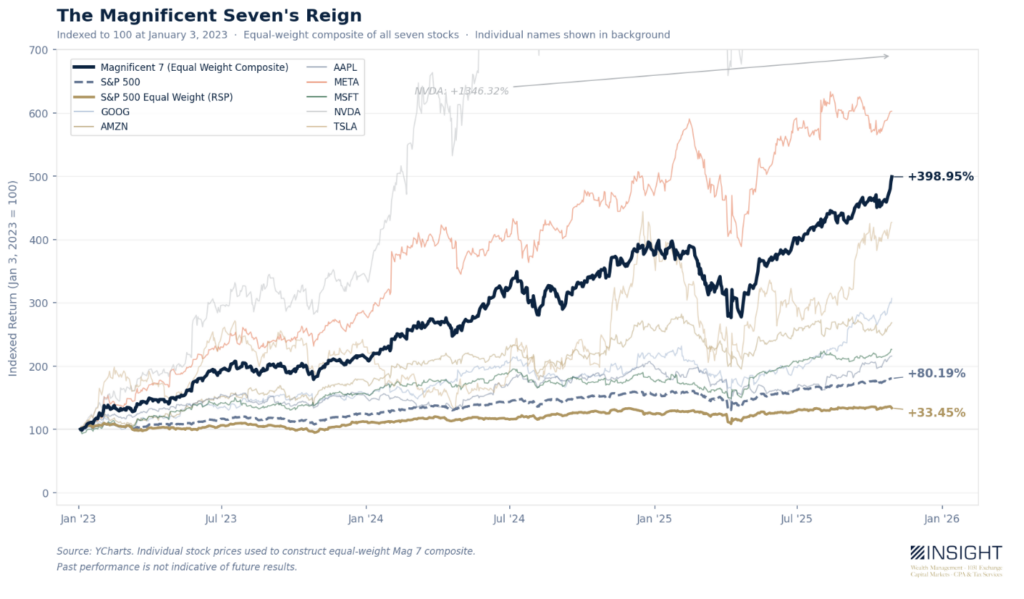

But with that (at least to some degree) behind us, we can now see the extent of the change in equity markets. But first, a quick reminder of just how significant the Magnificent 7 were in driving market returns. The rally started when the market turned in early 2023 and we were off to the races.

Past performance is not indicative of future results.

You can see just how impactful the weighted benefit of the Mag7 was during this time.

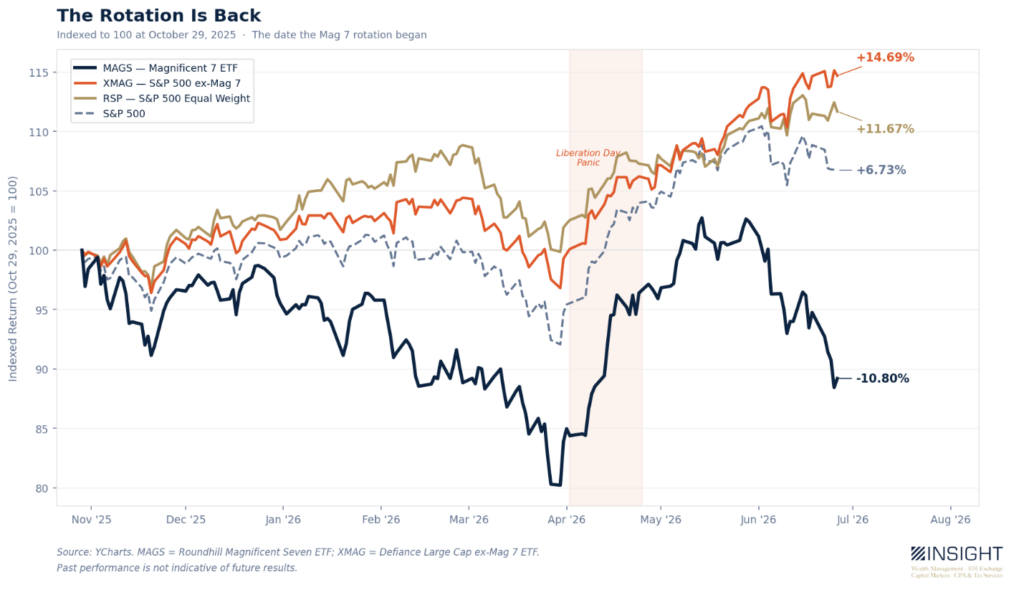

But as we noted in February, that all changed on October 29th when Meta reported earnings. It wasn’t really Meta’s fault. It was a pretty solid earnings report. But it was that moment when the market started to digest the risk it was holding as the Mag 7 began to take on mounds of debt to continue their AI infrastructure boom. The change has been stark.

Past performance is not indicative of future results.

Yes, there was a brief and significant rally after things settled down in Iran. One could have been forgiven for thinking the Mag 7 game was back in effect. But that changed quickly around the SpaceX IPO. The other 493 names in the S&P 500 are now beating the Magnificent 7 by over 25% since that Meta earnings call. That’s a meaningful shift that is significantly weighing down investors in market cap weighted ETFs.

Valuations Are Moving

The start of earnings season will be upon us when the world returns from the 4th of July. And what’s happening right now in earnings is telling for the future impact on the Mag 7 and the rest of the market.

To be fair to the Mag 7, their rise – while not fully justified – was based on earnings data. Their earnings growth during that time period was insane. And the success of that growth was directly correlated to the growth of their stock price.

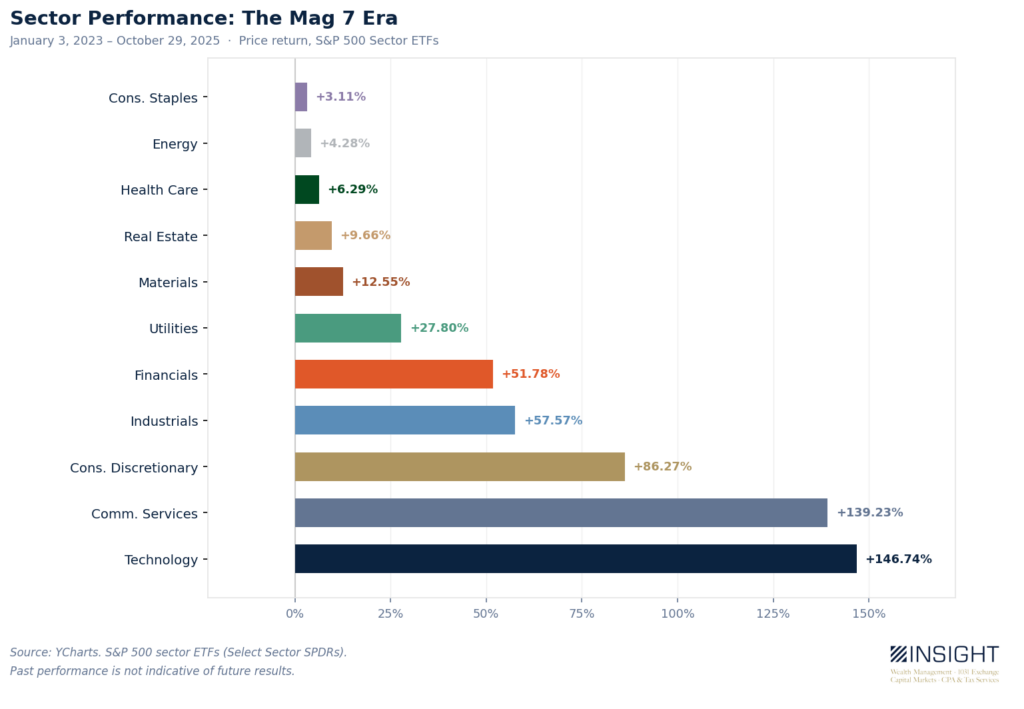

It showed up in the sector-by-sector performance of the market. Those sectors where earnings growth was expanding rapidly were being rewarded in the market. And unsurprisingly, Communication Services and Technology (where most of the Mag 7 reside) were the biggest winners.

Past performance is not indicative of future results.

That worm is turning. The exponential growth investors came to expect was never sustainable. The debt from their AI expenditures weighed too heavily. And the AI tools they hope to capitalize on have not yet borne fruit.

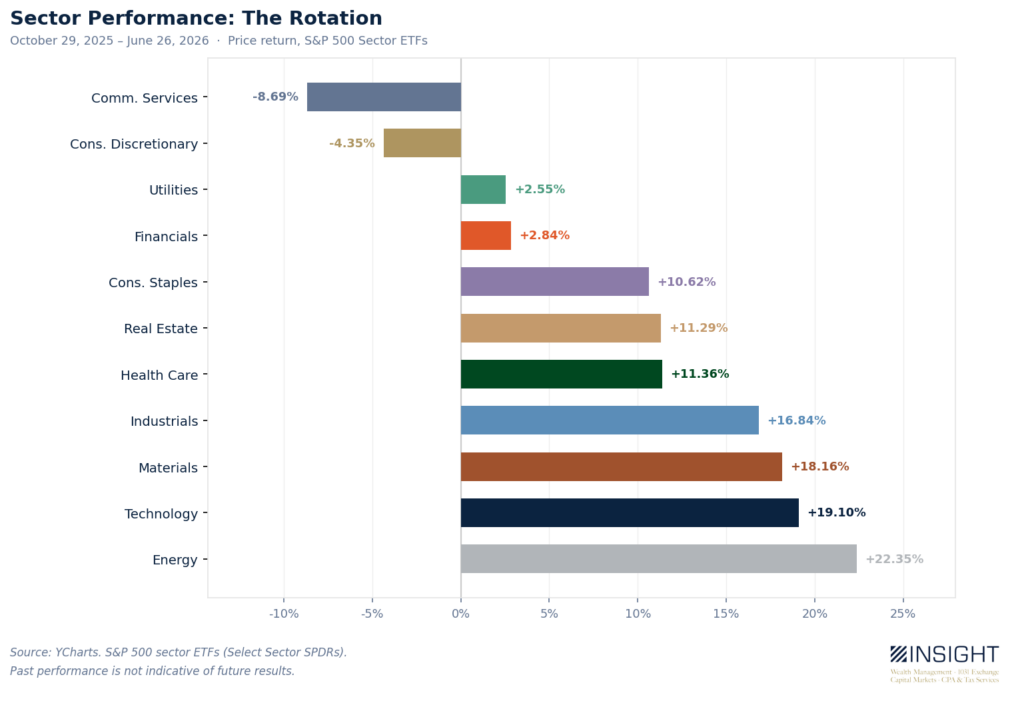

The results are showing up when you look at sector performance since October 29th. The shift is noticeable.

Past performance is not indicative of future results.

Communication services, which have dominated since 2023, are the biggest losers of the bunch. Energy – a former dog – is now leading the way. As are areas like materials, industrials, etc., etc. All the things we need to have to create an AI economy. Just not the sexy names that are building it.

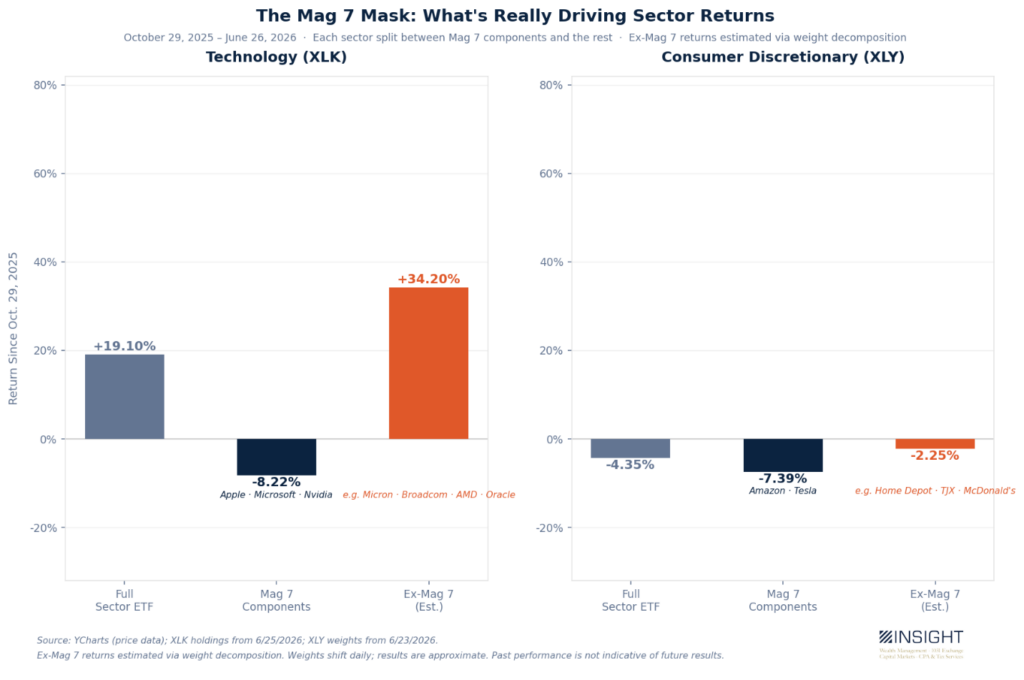

But wait – what about “Technology”? It was #1. And now it’s…#2. That’s not much of a fall-off, right? Aren’t the Magnificent 7 technology companies?

Yes…and no. Here are the sectors for the Mag 7 companies:

- Apple: Technology

- Microsoft:Technology

- Nvidia:Technology

- Google:Communication Services

- Meta:Communication Services

- Amazon:Consumer Discretionary

- Tesla:Consumer Discretionary

So, four of the seven are represented in the worst performing sectors over the last eight months. But even the sector story is masking the impact of the Mag 7. Because they are actually a drag on their sectors right now – not a boost.

Past performance is not indicative of future results.

It’s Always About Earnings

So if the sectors are masking the story, what’s the real signal? Earnings.

As we noted – extreme or not – the rise of the Mag 7 was all about earnings. Their earnings growth made everyone else look…flat.

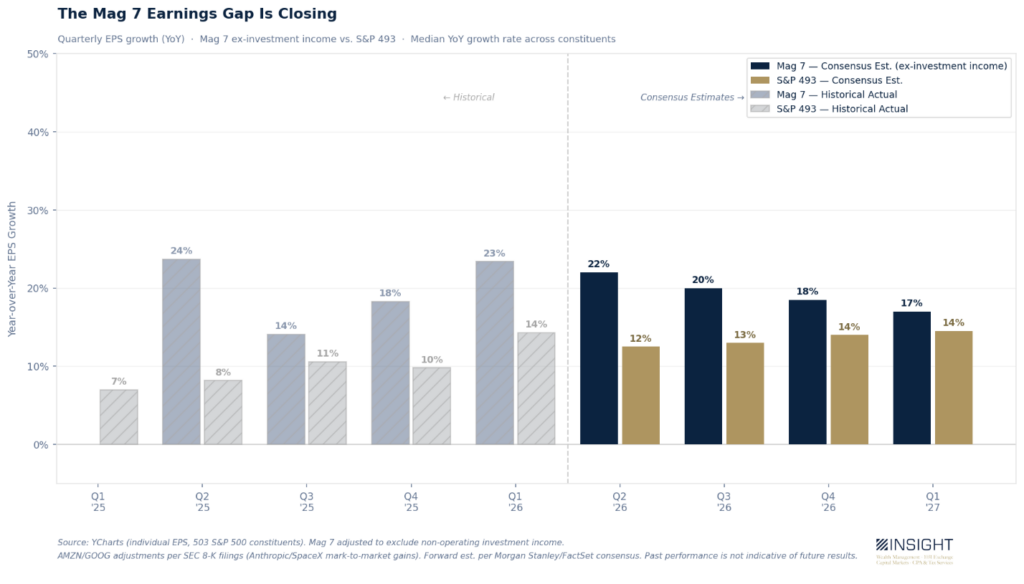

What goes up, must come down. Earnings can’t grow exponentially into infinity. Especially not when these companies are spending money aggressively to build the AI infrastructure of the future.

After the earnings growth started to slow, we got the Q1 figures. The headline number looked like a comeback: 52% earnings growth for the Mag 7. But it wasn’t growth driven by their businesses. It was accounting. Google and Amazon were required to mark up the value of their Anthropic stakes on their balance sheet. And that mark-up flows straight through to “earnings”.

The real math? Google reported earnings per share of $5.11 – but $2.35 of that was a mark-up in the valuation of Claude. Amazon reported $2.78 per share, but $1.22 of that was also from their valuation change in their Anthropic position.

When you strip those two things out, what you see is a gap that’s converging. A year from now, the earnings expectations for the Mag 7 are nearly in line with the expectations for the rest of the market.

Past performance is not indicative of future results.

That’s not the death knell for the Mag 7. 17% earnings growth is still fantastic. But 14% for the entire market? That’s amazing.

Investors use earnings data to chase returns, not the other way around. Their math comes to a simple question: what is the best value for a dollar invested today? Through that lens, what do you think is the better value: the Mag 7 at 33x earnings growing 17% or the rest of the market at 20x earnings growing 14%?

That’s why we see the Mag 7 slipping. The rotation is real. It’s healthy and it is justified. And we must adapt to it in portfolios.

And the fun part is this: you were ahead of it. The boring messages of diversification and valuation discipline aren’t a defensive strategy in 2026. It’s the offense. And it’s exactly the positioning we’ve maintained for months.

It’s working quite well. Enjoy the moment. That worm will turn, too. But the earnings chart above shows there is plenty of runway to enjoy.

Sincerely,

Insight Wealth Group