The Weekly Insight Podcast – When Optimism Becomes a Risk

This has been a remarkably good year in the market. War, energy disruptions, inflation risk. None of them have been able to pierce the veil of the growth happening in the U.S. economy writ large and the stock market specifically.

And for good reason. GDP continues to be one of the best predictors of stock market performance and the core pieces of GDP growth remain intact: Consumers are spending more, businesses are spending more, and the government is spending more. That spending drives growth. That growth drives markets.

As a firm we are very specifically NOT permanent contrarians. There is no value in it. The doomsayers may get the headlines – but unless you have the magic wand that can predict the future, trying to bet against the largest economic forces in the world is usually a losing game.

We are, however, observant. And when Wall Street does something, it rarely does, our hackles go up. Especially when the timing – historically – is not favorable. And that’s what we are about to see with Q2 earnings season which starts this week. Is it a moment to panic? No. But being measured in our decisions right now may pay big dividends in the coming weeks and months.

The History of The Low Bar

Regular readers have heard us talk about a particular phenomenon many times over the years: the tendency of Wall Street analysts to hedge their bets as a quarter rolls on. The reason is as basic as human biology: survival. If you are a paid analyst and you predict 3% growth in a company which instead comes in at 2%, you’ve failed. But if you predict 2% and it comes in at 3%? No risk to you.

And so, it goes with earnings expectations. Nearly every single quarter we see Wall Street do the same thing: start the quarter with rosy predictions for growth and constantly lower the bar as the quarter goes along. By the time earnings season comes around, the bar tends to be particularly easy to clear.

In fact, over the last 10 years, Wall Street has lowered their predictions – on average – by 2.7% each quarter. And so, when companies beat that prediction by 1%, it is a huge “win”. No one remembers what was being expected three months before.

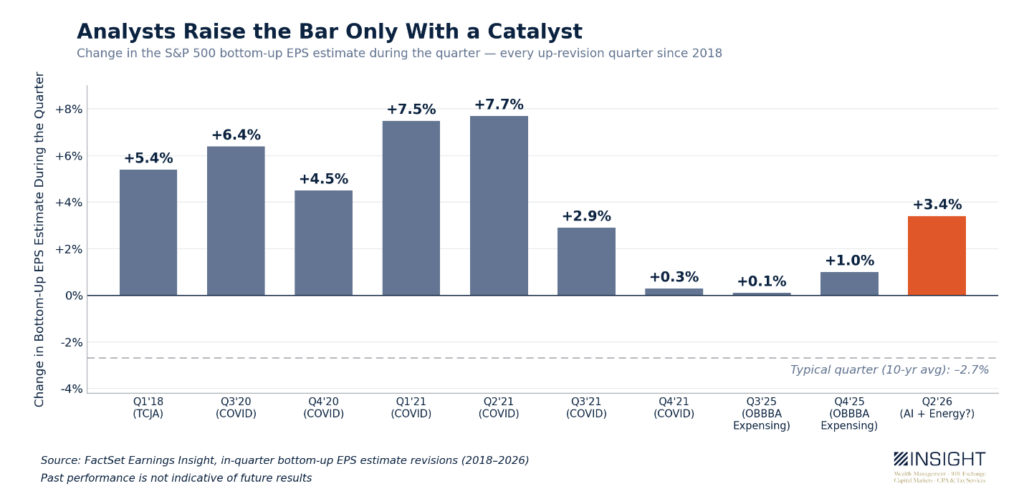

The Bar Is Raised

The “lowering into earnings season” phenomenon is so normal, most do not even think about it anymore. But that makes it even more notable when the opposite happens. And the drivers of such a change tend to be big and bold.

Analysts have raised their expectations of earnings just nine times in the last 8.5 years (or 34 quarters). Q2 2026 – the earnings season we enter this week – just became the tenth.

Past performance is not indicative of future results.

As you can see, the earlier examples had big, structural catalysts. The Tax Cut and Jobs Act from late 2017, the COVID recovery, and the One Big Beautiful Bill. And – if we are being frank – the numbers in 2020 and 2021 had more to do with analysts’ lack of ability to predict COVID impacts than they were about meaningful changes.

And then there’s this quarter. Earnings expectations have risen 3.4%. On its face, that seems like wonderful news. Earnings are up. Awesome!

But, as is often the case, the easy answer is not the best one.

Pricing in Greatness

All price movement in the market is not caused by earnings. Lots of things happen to move the needle. International affairs, public policy, economic conditions, and many other factors can play a role. But clearing the bar for earnings does matter.

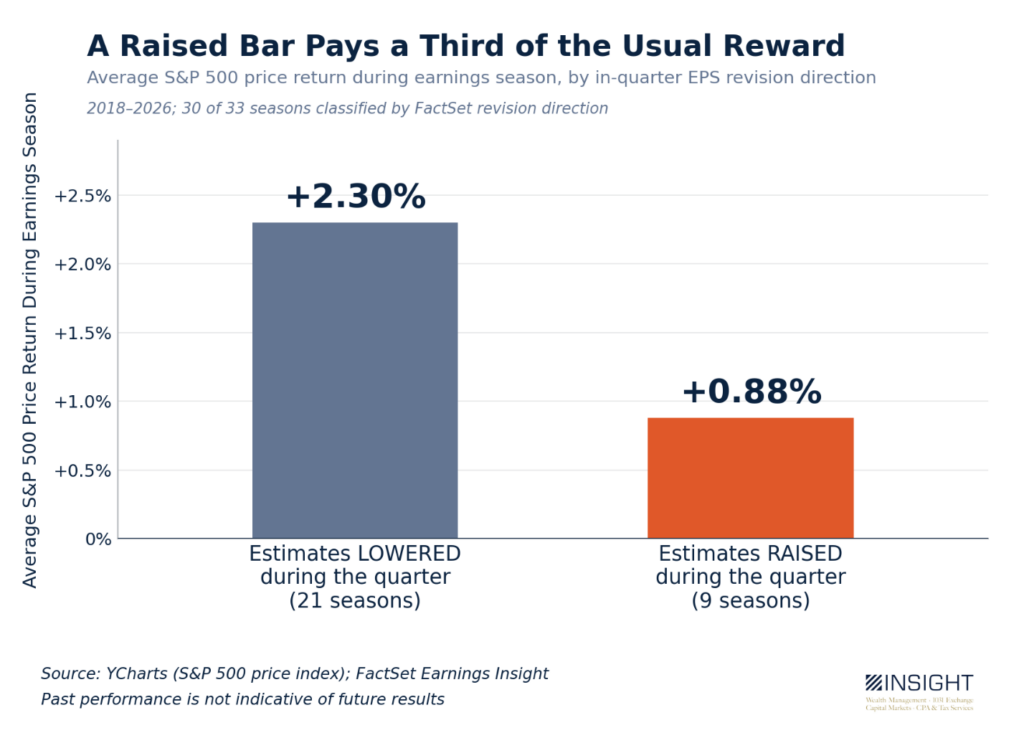

Remember we told you that – in the average quarter – industry analysts lower earnings expectations by 2.7%. We also know that – over that same time – stock market price performance has averaged +1.78% during the six weeks that make up earnings season each quarter. Earnings season has been a particularly good time for equities.

While the sample size is small, we do know that there is a significant gap, however, between quarters when analysts lowered earnings expectations and the nine recent times they have raised them.

Past performance is not indicative of future results.

Nearly 150 basis points of reduced performance is significant. And while there is not one easy answer that addresses the totality of the difference, one thing is clear: raising the earnings bar means the market is pricing in all the potential good news. There is no juice left in earnings season. In fact, the only real optionality is toward disappointment.

And disappointment – i.e., negative earnings surprises – have recently been punished badly. The five-year average for stock performance after a negative earnings surprise is -2.9%. In Q1 that number was -4.9%, 1.7x the average.

So, meeting (or exceeding) these raised expectations has less benefit. And missing them has a greater cost. Pricing in perfection leaves little room for outperformance.

What Is This Quarter’s Catalyst?

We mentioned before that previous quarters of raised expectations have had clear and obvious causes. In fact, it has only been two things: the COVID recovery and the impacts of tax policy.

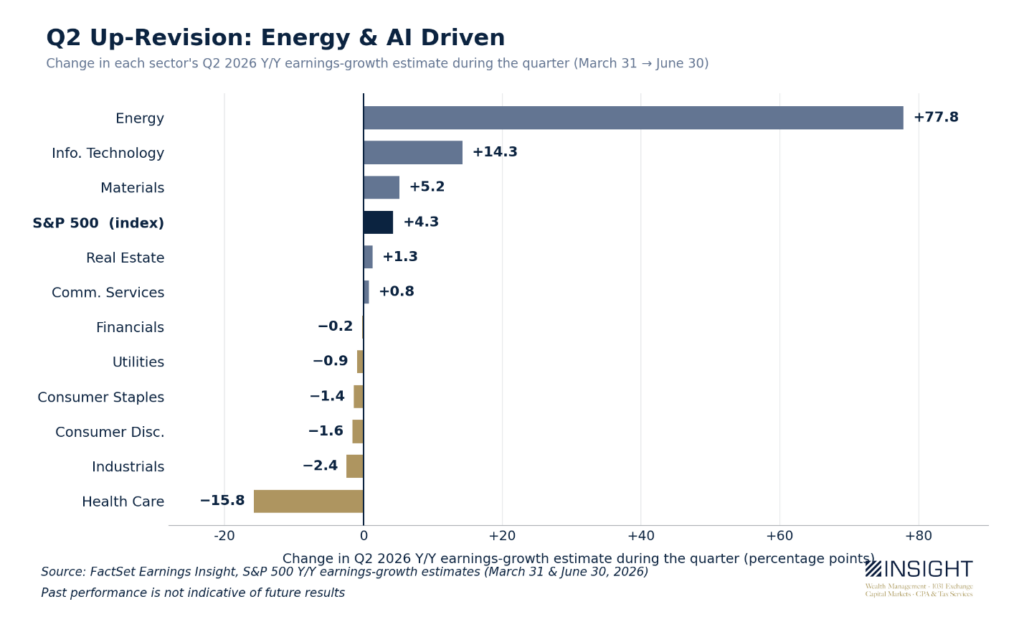

But what is it now? When we dig down to a sector-by-sector analysis of the changes we can see the story becomes obvious. Many sectors – as is normal – saw a reduction in their expectations. But two are blowing the doors off earlier estimates.

Past performance is not indicative of future results.

The energy revision makes a lot of sense. The conflict in Iran drove up energy prices. Energy companies sold their wares for higher prices and generated more revenue.

The revision for Information Technology is a bit more speculative and habitual for the market. It is the Magnificent Seven/AI story the market has been telling for the last three years, just with some new names.

Take, for example, Micron. It is the new darling of the tech space after it blew the doors off earnings last quarter. It rose nearly 900% in the last year. Why? It sells memory chips – something AI companies are gobbling up.

But the price movement in Micron – and the earnings expectations for the company – are built on future earnings expectations (i.e., the very same focus of this memo). They are built on the idea that no matter how many chips Micron makes, the market will want more. The demand will be endless.

Capitalism does not work that way. And neither does the semiconductor market. New inventions – which are happening constantly – will replace the current product. And new sellers will enter the market to compete with companies like Micron.

The question is not Micron as a company. It’s doing a fantastic job. It is instead the valuation the market is placing on its future growth (assumed to be exponential!). Take – for example – the new expectation about China’s largest competitor to Micron, CXMT. Analysts now project that by the end of this year, they will be able to produce 350,000 wafers per month. Micron currently produces 385,000.

CXMT is catching up fast, and for good reason: the market needs competitors. But that competition will – and has – weighed on Micron’s price. It peaked at over $1200 per share. Analysts were saying it was “cheap” (after rising 900%!) because as a function of its projected earnings, it was selling at 6 – 10x forward P/E.

That is cheap. If the earnings can grow like that. CXMT might have something else to say about it. Which would explain why – after this projection – Micron’s shares have dropped over $200 per share to $979.30. That’s a two week move that wiped out a lot of equity for the investors who “bought cheap” at $1200+.

Which brings us full circle: expectations. When expectations – particularly in these two sectors – rise to the levels we see today, they become particularly hard to meet. Does not meeting them mean the companies have failed? No. It means the analysts have. But with the market pricing perfection in these spaces today, it may have a negative impact on the market as we work back to more normalized assumptions.

Sincerely,