The Weekly Insight Podcast – The Old Playbook Doesn’t Apply

EDITOR’S NOTE: This memo was completed Saturday, March 7th. Since then, oil briefly spiked to $119/barrel before settling above $100 for the first time since 2022. That caused added volatility in Asian and European markets overnight as well as in the U.S. today. The thesis below continues to resonate.

The market experts were out in full force on Monday morning. The U.S. was at war with Iran. The Strait of Hormuz was effectively closed. And investors were looking for guidance. What do we do? Do we panic and sell? Do we buy the dip? Thankfully, we have places like CNBC to rely upon for measured and consistent advice.

Here’s what we heard Monday morning.

JP Morgan Trading Desk (via CNBC): “We are ‘Tactically Cautious’ as we prepare for what may be a multi-week period of elevated uncertainty. We would look for a 1 – 2 week decline in risk assets, creating a buy-the-dip opportunity as the market looks through the initial pullback.” (Note that news headlines said things like “JP Morgan says buy the dip!”)

Wells Fargo (via same CNBC Story): “The situation is fluid, but the playbook from the past two Gulf Wars was to sell the news, i.e. buy stocks…History also suggests geopolitical dips should be bought, usually recovering in two weeks.”

Jim Cramer (CNBC after Monday’s Close): “The market simply didn’t mind…We produce so much oil domestically that there’s really nothing (world oil producers) can do to cut us off.”

Peter Oppenheimer, Goldman Sachs: “View any pullback as a buying opportunity rather than the onset of a bear market.”

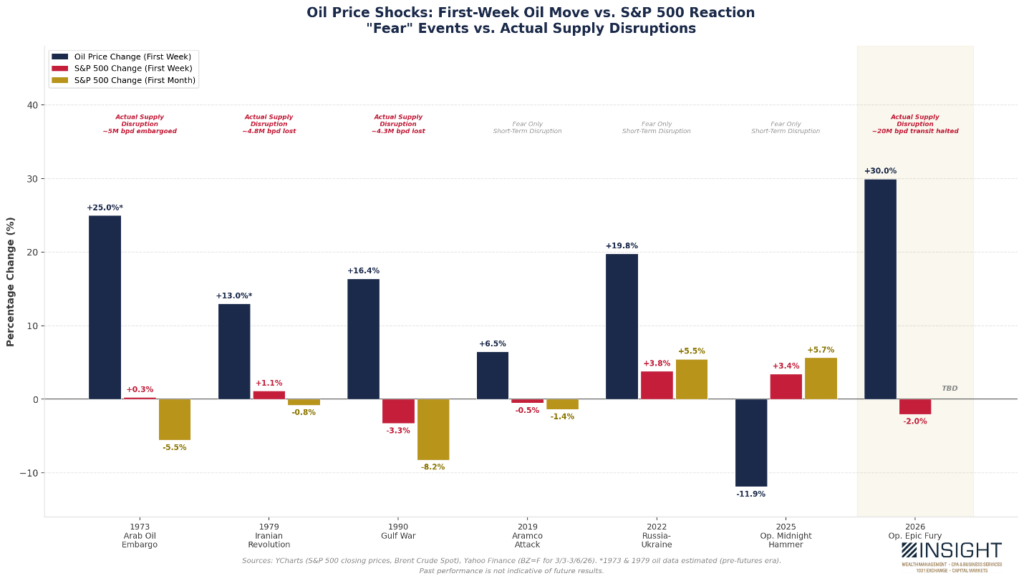

The market heard them. And the market understood. It knows the playbook: market dips caused by fears in the oil market have consistently been a wonderful buying opportunity for equities. And we’ve seen it play out very recently: markets were up more than 3% one week after both Russia’s invasion of Ukraine and 2025’s bombing of Iran (Operation Midnight Hammer). One month later, markets were up 5.5% and 5.7%, respectively.

And so, on Monday, both the S&P and Nasdaq closed higher than their close on Friday. Even after opening down more than one percent. The market bought the dip. Even after significantly more drama throughout the week, the S&P only ended up down 2.02%. To put that in perspective, since 2000, there have been 948 5-day trading periods when the market has been down 2% or more. That’s 14.4% of all 5-day periods. Last week in the market wasn’t bad. It was normal.

Scare vs. Disruption

So, the question we need to be asking ourselves is this: Is this normal? Should we treat it like previous oil price disruptions? Or previous U.S. military interventions? Should we be buying the dip – or is this a different moment that’s not being recognized as such by the market?

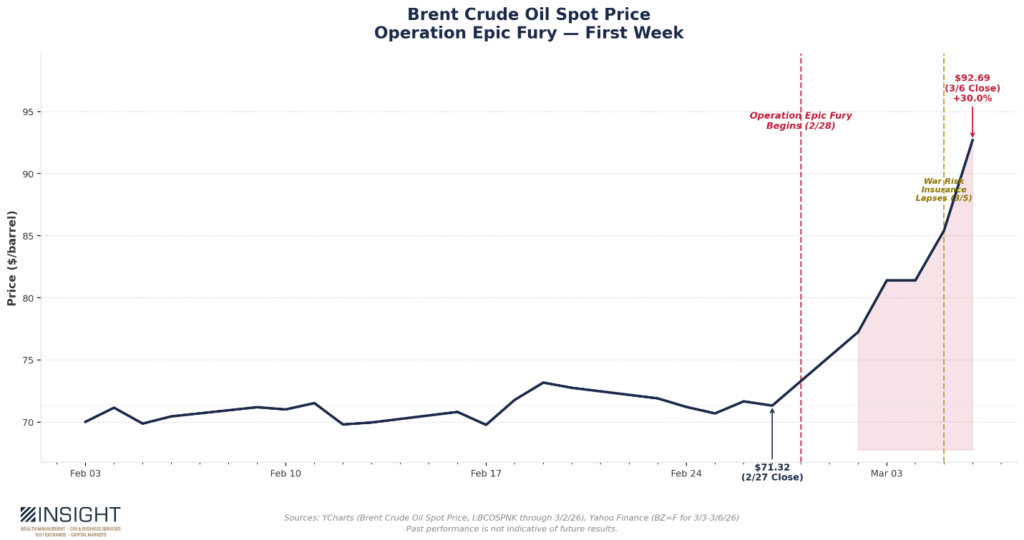

The oil market at this moment is different. Brent Crude rose 30% last week. That’s the biggest five-day price increase of any geopolitical oil shock in the modern era.

Past performance is not indicative of future results.

But, as the chart above shows clearly, there are two distinctly different types of oil price shocks: those caused by a fear of disruption and those caused by an actual disruption of supply. The experts on the news spent most of the week telling us this was a “fear moment.” The oil market – especially later in the week – came around to the idea that this might actually be a supply disruption moment.

Past performance is not indicative of future results.

What Really Happened

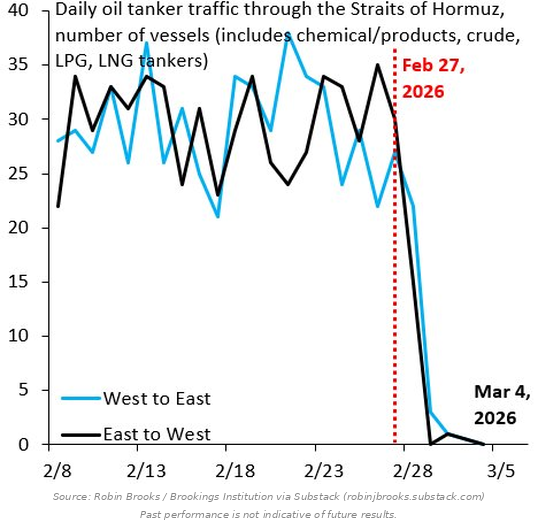

As you know, this all comes down to the Strait of Hormuz and whether oil supply can transit that very narrow piece of water next to Iran’s shores. Last week we told you the real risk to markets wasn’t Iran’s navy, it was whether shipping companies and their insurers would take the risk. We now know the answer: they won’t. As former IIF Chief Economist Robin Brooks pointed out this week, shipping traffic through the Strait has collapsed to near zero.

Past performance is not indicative of future results.

That’s all about insurance. The insurance companies issued their “Automatic Termination of War Risks Coverage” for all ships transiting the Strait. They lapsed at midnight on March 5th.

And so, some ships – those that were ready to go – raced for the exits. And while oil markets jumped, they held steady through Thursday. Maybe the conflict would be resolved? Maybe another plan would come through? Maybe this was just another scare?

During this time, the Iranians weren’t doing anything to instill confidence. They struck at least eight commercial vessels across the Persian Gulf and the Gulf of Oman. They targeted a Saudi refinery, another in Bahrain, a port storage facility in the UAE, and Qatar’s LNG facilities which produce one-fifth of the world’s LNG supply.

By Friday morning, oil markets were starting to grapple with reality. Insurance no longer existed, twenty million barrels per day were stranded in the Gulf, and there is yet no end in sight. This is a real supply disruption. It isn’t a scare. Even if equity markets haven’t accepted that fact yet.

The U.S. to the Rescue?

You may have heard that President Trump announced a two-part plan to get the Strait of Hormuz open again. In his announcement, he declared that the U.S. would provide insurance coverage to ships transiting the Strait and that the U.S. Navy would provide escort for those same ships.

That had a calming effect on the market when he said it on Tuesday. Oil prices dropped by over $4/barrel. Equities jumped. But executing the plan is much harder than announcing it.

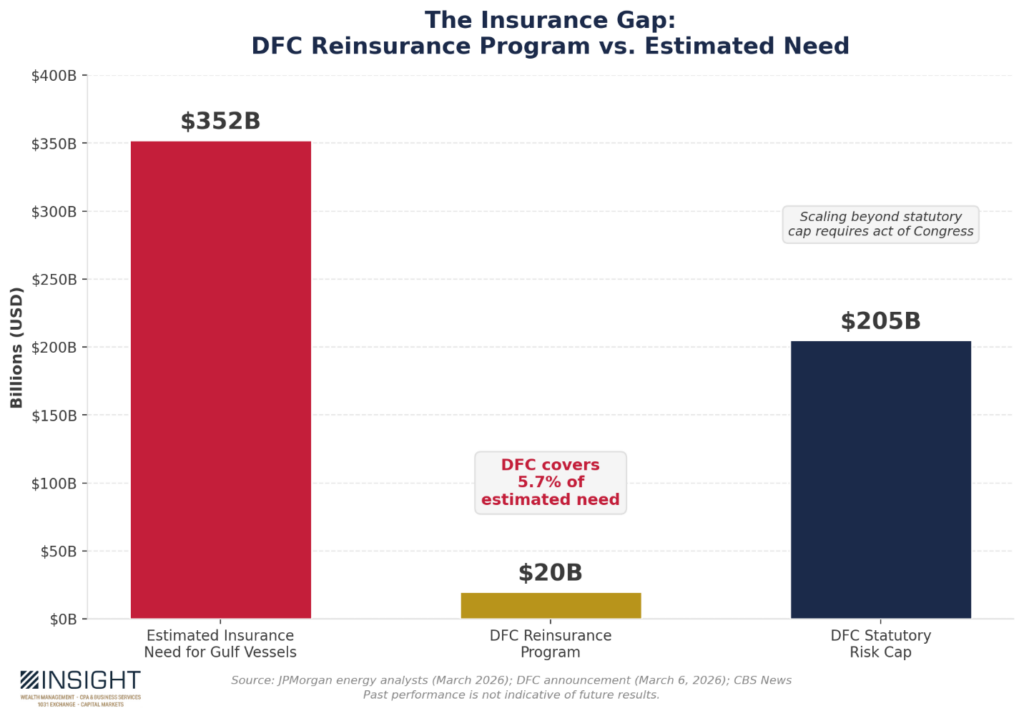

Over the weekend, the administration announced that the U.S. International Development Finance Corporation (DFC) would, in conjunction with the Treasury Department, provide a $20 billion reinsurance program for ship traffic through the Strait. The DFC CEO, Ben Black, stated that “we are confident that our reinsurance plan will get oil, gasoline, LNG, jet fuel, and fertilizer through the Strait of Hormuz and flowing again to the world.”

We should all hope so. But, as shocking as it might be, $20 billion is just a drop in the ocean as it relates to the real insurance needs right now. JP Morgan estimates the current need for the 329 vessels trapped in the Persian Gulf – for both the ship itself and the cargo it carries – is north of $352 billion. The DFC plan covers just 6% of the demand.

And even if the DFC went all the way to the maximum allowed number, they would only be able to insure $205 billion. Beyond that, they need an act of Congress to bump their statutory risk cap.

Past performance is not indicative of future results.

The bigger problem with the plan, though, is that it’s a RE-insurance plan. That means the U.S. is actually insuring the insurers that write the policies. That makes sense as the U.S. government is not the expert in underwriting maritime shipping insurance. But it also means none of this works if insurance companies are still unwilling to write policies.

And – at least for today – they are. And they will continue to be until they can be convinced the risk is reduced. Which brings us to the President’s promise of Navy escorts for these ships. That would – theoretically – significantly reduce the risk.

But the Navy isn’t ready to help. At least not yet. According to Lloyd’s List, they told shipping officials last week that American naval protection “is not an immediate option” as there is “no availability of naval escorts and no timeline for when such arrangements will be available, if at all.” They’re busy fighting a war.

What This Means for You

We don’t pretend to know how this resolves. Is it possible that the war is resolved quickly, the Strait reopens, and oil markets go back to normal? Of course. But there has never been a time in modern history where the infrastructure for moving oil has been this impacted. And while the market’s muscle memory from earlier oil scares (buy the dip!) sounds great, this may be a longer and more protracted issue than the experts seem to hope.

The risks remain real. Twenty percent of the world’s oil supply is, quite literally, dead in the water. The last time we had a sustained supply disruption (the 1973 Arab oil embargo), we saw GDP contraction, rising inflation and unemployment, and significant impacts on equities. The disruption during the 1990 Gulf War contributed to a recession that was already building but was quickly resolved when oil supply resumed.

Are we saying that’s what’s going to happen? Absolutely not. But we’re weighing those risks in every portfolio decision we make. It’s why we didn’t buy any dips this week – or sell any of our large energy positions into the rising oil prices. Our hedges allow us patience and a place to shelter if this isn’t the “buying opportunity” the pundits were pushing on Monday morning.

Sincerely,