The Weekly Insight Podcast – The Chokepoint

EDITOR’S NOTE: This memo is being drafted on Saturday, February 28th. Due to travel on March 1st & 2nd, we wanted to get this written given the timeliness of the situation. Significant facts may have changed by the time you read this. If an update becomes necessary, we will address it in next week’s Memo.

UPDATE: After the completion of this memo, Iran announced that Ayatollah Khamenei has been killed in Saturday’s attacks.

Well, it happened again. Remember two months ago when we wrote about rolling over in bed on a Saturday morning to find out we’d gone in overnight and captured the dictator ruling Venezuela? New Saturday morning, same result! The alerts started coming in hot and fast: The U.S. is now at war with Iran.

The political response is…predictable. Republicans love Trump’s decisiveness to eliminate a dictator, free an oppressed people, and defend Israel. Democrats are furious that Trump is engaging in a war without consulting Congress. It’s worth reminding them both that the GOP loved Trump’s campaign slogan of “no more foreign wars” and the Democrats never complained when President Obama bombed seven different countries during his term as President without ever getting Congressional approval.

But we’re not going to solve the politics of this situation. And we’re not going to solve the geopolitics either. Last we checked, we didn’t have any missed calls from (202) 456-1414 (the White House switchboard). No one making these decisions is asking our – or your – opinion.

So – love the new war or hate it – the question we need to answer is what this means for the market and the economy. And more specifically, what it means for your portfolio. Let’s dive in.

The Big Issue: The Strait of Hormuz

Regular readers of this memo are familiar with the geopolitical chokepoint that is the Strait of Hormuz. The 21-mile-wide strait that separates the Persian Gulf from the Gulf of Oman and the Indian Ocean is the most important stretch of water in the world. The math is simple: 20% of the world’s oil supply flows through that pass every single day.

As far back as April 2024 (when Israel and Iran were trading missile attacks), we noted – in our memo The Next Recession – the following:

“There is one clear global economic risk: Iran closing the Strait of Hormuz…that simple action would cut off 20% of the world’s oil supply and nearly guarantee a worldwide recession.”

Then, during the “12-Day War” between Israel and Iran in June 2025 (which was ended quickly when the U.S. struck Iranian nuclear facilities), we addressed it again. The Iranian parliament called for closure of the Strait at the time. They lack any “real power” – that all lies with Ayatollah Khamenei. And he blinked. As we said at the time:

“…think about it from the ‘big picture’ perspective of the leadership in Iran…Yes, closing the Strait would be a wonderful way to exact revenge against the United States. But it’s also a terrific way to make sure you end up without a country to govern.”

The political answer at the time was simple: if Khamenei wanted to remain in power, it was better to keep the Strait open and not solicit the wrath of the United States military.

That math for the Ayatollah and his friends may change rapidly in this conflict. President Trump has been clear in his messaging around this current invasion. As he said in his video address Saturday morning to the Iranian people: “When we are finished, take over your government. It will be yours to take. This will be, probably, your only chance for generations. The hour of your freedom is at hand.”

The goal of regime change was made clear. The U.S. & Israeli militaries are explicitly targeting Khamenei and his regime. He (or his successors) may then see closing the Strait as his final bargaining tool. As we noted back in 2024, “desperate economies take desperate actions”. This may be the only tool the regime has left in their bag.

Moving Fast: The Strait is Closed

We were about to wrap up this memo when word came down: Iran has announced a blockade of the Strait of Hormuz. Whether Iran can sustain the blockade is an open question, but the shipping industry isn’t waiting to find out. Maersk, Hapag-Lloyd, and others have already diverted or suspended transits. While some ships are still trying to sneak through, the Strait of Hormuz is effectively closed at this moment.

The obvious question here is “wait…can’t the U.S. Navy just move in and keep it open?” Yes and no. No one is questioning whether the world’s most powerful naval force can control a 21-mile stretch of water. Iran’s Navy won’t win.

But they don’t need to. They can launch drones or missiles from shore. They can send out speed boats to drop mines. They could use drone boats like Ukraine has effectively deployed. The closure of the Strait isn’t based on military might. It’s based on the willingness of shipping companies (and their insurers) to take the risk of transiting the Strait.

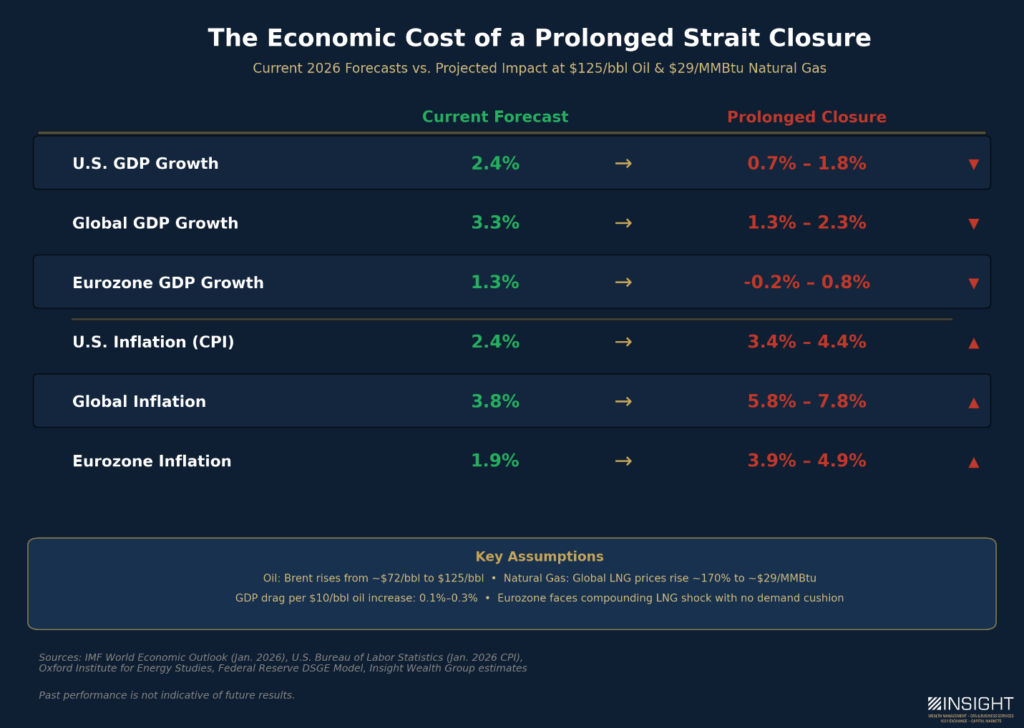

The Math: What Does This Mean for Global Energy?

The easy number is what we’ve said many times before: 20% of the world’s oil supply flows through the Strait of Hormuz. The impact on the global economy depends almost entirely on how long it stays closed. Analysts estimate a short-term closure would drive prices up to $80 – $100 per barrel. A longer-term closure (think more than two weeks) would drive prices higher with estimates falling in the $110 – $130 per barrel.

J.P. Morgan put out a piece late last week that was actually – long-term – bearish for oil. Their head of Global Commodities Strategy Natasha Kaneva noted the following:

“But given elevated inflation and this year’s midterm elections in the U.S., we do not anticipate protracted oil supply disruptions. If military action does occur, we expect it to be targeted, avoiding Iran’s oil production and export infrastructure.”

That came out the day before the first strikes. We’re guessing Ms. Kaneva wishes she were correct because she goes on to point out:

“Regime changes in oil-producing countries – whether through leadership transitions, coups, revolutions, or major political shifts – can have a profound impact on …global oil prices…averaging a 76% increase from onset to peak.

Prices rose sharply on Friday, with WTI crude closing at $67.02 and Brent hitting $72.48. A 76% increase in that price would be $118 (WTI) and $128 (Brent) per barrel. Right in the middle of the projected long-term closure estimates. Prices will undoubtedly be higher on Monday, but we won’t see the full sweep of the risk. That will depend on how long it is closed.

There’s No Easy Fix

The problem with the Strait is bigger than many pundits let on. And we understand why: this risk has been talked about for years and it has never, ever been closed (until now). Even during the “tanker wars” of the 1980s – when Iran and Iraq were attacking each other’s tankers – the Strait was never closed.

So, us writing about it for the last two years could have been seen as excessive. But the risk is real and the impact is huge.

Some market experts will tell you that the Strait is important, but – in a crisis – the oil will just be shifted to pipelines. That’s a great theory. But the problem is the pipeline capacity doesn’t exist. As you can see from the graphic below, it would only solve about 13% of the problem.

Past performance is not indicative of future results.

That still leaves roughly 17MM barrels per day pulled from the oil supply.

And there’s another significant issue noted in that graphic in very small print: Qatar. Qatar doesn’t produce much oil. But they do produce 20% of the world’s supply of liquified natural gas (LNG). And the ONLY outlet for that supply is through the Strait. There are no gas pipelines to service that supply.

Which brings us to the big picture impact.

1. Oil Prices: The broadly accepted math is that each $10 increase in oil prices equates to a 0.1% – 0.3% decrease in GDP and a 0.2% increase in inflation. Assuming a jump from $67 to $117, that is a 0.5% – 1.5% hit to GDP and at least a 1% increase in inflation. Both would be serious. The problem compounds the longer the Strait is closed and the higher the price of oil goes.

2. Natural Gas Prices: Natural gas is a global market driven by local issues. Prices will rise worldwide – but much less here in the United States as North America is the world’s largest producer of natural gas. The good news – it will make our natural gas exports worth a lot more. The bad news is it will drive up prices for Europe and Asia dramatically.

Europe already bailed on Russia as a natural gas supplier after the Ukraine invasion. Instead, they built their entire energy infrastructure around LNG imports. Oxford Institute for Energy Studies is estimating that a prolonged closure of the Strait would mean natural gas prices rise globally 170% to $29/MMBtu. That is a huge problem for European leaders – and likely the reason they’re encouraging the U.S. and Iran to come back to the negotiating table.

And Asia is likely the bigger story. 83% of Qatari LNG goes to Asian markets. How does China respond? And who fills that gap? Hint: Canadian LNG might have a moment here.

Past performance is not indicative of future results.

What Does It Mean for Portfolios?

As in any major disruption, there’s always a good news/bad news component to this. The bad news is obvious: a prolonged closure meaningfully increases recession risk. A whole new series of conversations will start happening. Can the Fed cut rates if inflation is going to pop off? And how do they defend against a recession if they can’t cut rates? Do our European holdings suffer if natural gas prices there increase very quickly? Keeping the closure of the Strait brief is imperative to ensure these don’t become larger issues.

The good news? We continue to be overweight energy in portfolios. Significantly overweight. And it’s not just U.S. oil companies. We have substantial exposure to oil companies, natural gas companies, and energy infrastructure (pipelines, rigs, etc.). Those companies will all benefit from elevated energy prices. And it could get particularly good for the Canadian LNG companies we own as they will likely be the direct beneficiaries of the Asian market looking to replace Qatari LNG.

The even better news? Our clients are sitting on a LOT of cash right now – fully 8% of our overall holdings. If a correction hits, we’ll have a lot of opportunities to take advantage of it.

This is a rapidly developing story – as evidenced by the change in the Strait while we were writing. As we finalize this memo, reports are emerging that Ayatollah Khamenei has been killed in the strikes. Iran denies it. But if it’s true, it may shorten the period the Strait is closed. A new government in Iran is going to want those oil dollars to rebuild.

Sincerely,