The Weekly Insight Podcast – Liberation Day?

Happy ADK Day, as we call it at Insight! Today is Andrew Kleis’ (one of Insight’s founders) birthday. He shares his birthday with none other than Johann Sebastian Bach, which explains his amazing tuba playing back in high school. You’ll have to ask him about it…

On a more serious note, let’s get down to business. When you write a weekly column on the market, there can be times when you feel like you’re stuck in a rut. The same issues – waiting to be resolved – drive the market. Five years ago, it was COVID. The sheer number of times we wrote about infection rates, resurgences, etc. was pretty mind numbing. But it mattered.

Today, there’s one big issue: tariffs. Yes – there are offshoots to that. Policy uncertainty – driven by the tariff discussion. Volatility. Tax policy. They all matter. But they all come back to one simple question: what will Trump’s tariff policies look like?

In speaking with an analyst ten days ago, he stated “The market believes we just have to get to April 2nd. Then we’re going to know what’s happening on tariffs”.

Trump himself has called this Wednesday “Liberation Day”. The whole market is on edge, just waiting to learn what the final plans are going to be. To which we say, really? Are you sure we’re going to have an answer?

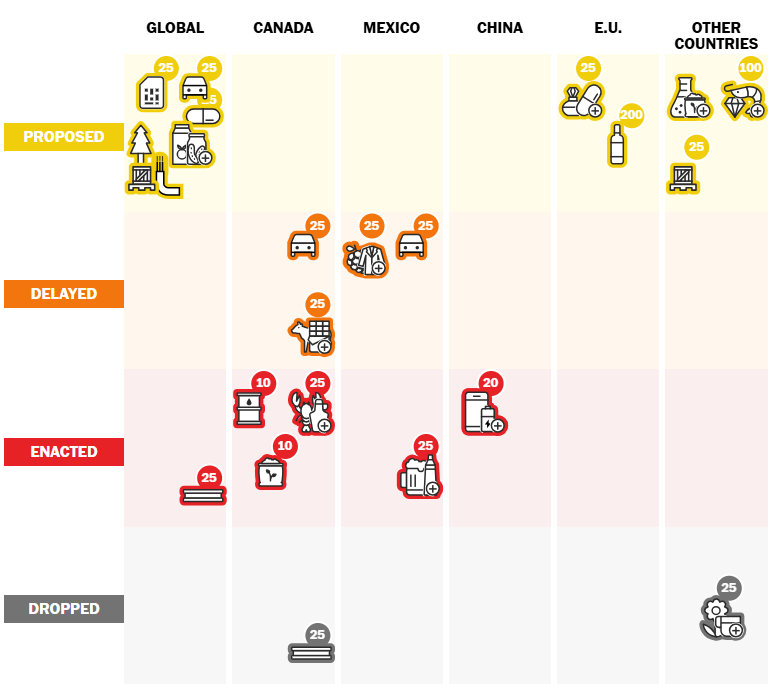

Let’s look at the tariff timeline so far:

January 20th (Inauguration Day): Trump announces plan to put 25% tariffs on Canada and Mexico on February 1st.

January 26th: Trump threatens tariffs on all Columbian imports (at 25%) after the country rejects U.S. flights carrying migrants back to Columbia. Columbia announces 25% retaliatory tariffs but eventually folds. Columbia accepts the flights, and the trade war is off.

February 1st: Trump signs an executive order to impose tariffs on Mexico (25%), Canada (25%), and China (10%).

February 3rd: After a terrible response in the stock market, Trump agrees to a 30-day pause on the Mexico and Canada tariffs.

February 4th: The China tariffs go into effect. China responds with an aggressive package of tariffs against U.S. energy, agriculture, and auto imports.

February 10th: Trump announces plans to hike steel and aluminum tariffs to 25% effective March 12th.

February 13th: Trump announces plans for “reciprocal tariffs” meaning the U.S. would impose the same tariffs on any country that had a tariff on U.S. imports. He indicates this would apply to all countries and suggests it could mean up to a 25% tariff on the E.U.

March 4th: Trump’s 25% tariffs on Canadian and Mexican imports go into effect, but he limits the tariff on Canadian energy to 10%. He also doubles the Chinese tariffs to 20%.

March 5th: Trump grants a one-month exemption on the Canadian and Mexican tariffs for U.S. automakers.

March 6th: Trump announces a wider postponement on many Mexican and Canadian imports.

March 12th: Trump’s 25% tariff on steel and aluminum goes into effect. The E.U. announces they will retaliate by taxing U.S. industrial and agricultural products, covering goods worth roughly $26 billion. However, they delay this action until Mid-April.

March 13th: Trump announces a potential 200% tariff on European wine and spirits in response to the potential E.U. tariff on U.S. whiskey.

March 24th: Trump says he will place a 25% tariff on any country that buys oil from Venezuela. This will primarily hit China, India, and Spain. He doesn’t address the roughly 84 million barrels of oil the U.S. is importing from Venezuela each year.

March 26th: Trump announces he is placing a 25% tariff on all auto imports into the United States.

So where does that leave us so far? A lot of proposed tariffs. And a limited number of things that have actually gone into effect:

- 25% global tariff on all steel and aluminum imports.

- 10% tariff on all Canadian energy and fertilizer imports.

- 25% tariff on all Mexican and Canadian imports except autos, energy, steel/aluminum and other USMCA covered goods). The result, after the USMCA exemptions, is that Mexico is essentially immune from tariffs and Canada is being tariffed on dairy products, sugar, and peanuts.

- 20% blanket tariffs on all Chinese imports.

Source: www.WashingtonPost.com

Other than China, steel, and aluminum, not much has been implemented.

Maybe Wednesday is the day we finally get clarity. But we’re not so confident on that front. Trump himself said last week that he “may give a lot of countries breaks” when it comes to tariffs. And he reiterated later in the week that he’s “open to deals” with other countries. National Economic Council Director Kevin Hasset said on Fox News’ Sunday Morning Futures that “President Trump is going to decide how many countries…I can’t give you any forward-looking guidance on what is going to happen this week. The President has a lot of analysis before him, and he’s going to make the right choice”.

We tend to believe this isn’t the finish line and we won’t have a binary and final outcome on Wednesday. If you’ve been paying attention to Trump’s nature over the years, this is much more like a real estate negotiation.

Think of it this way: 1990 Donald Trump walks into a building he wants to buy. He’s standing there with the seller. Do you think he says: “Wow…this is my favorite building ever. I just have to have it! Name your price”?

Or do you think he says: “Yeah…this building needs a lot of work. There’s no way I’ll meet your price. But I’ll take it off your hands for…”? And then the negotiation starts.

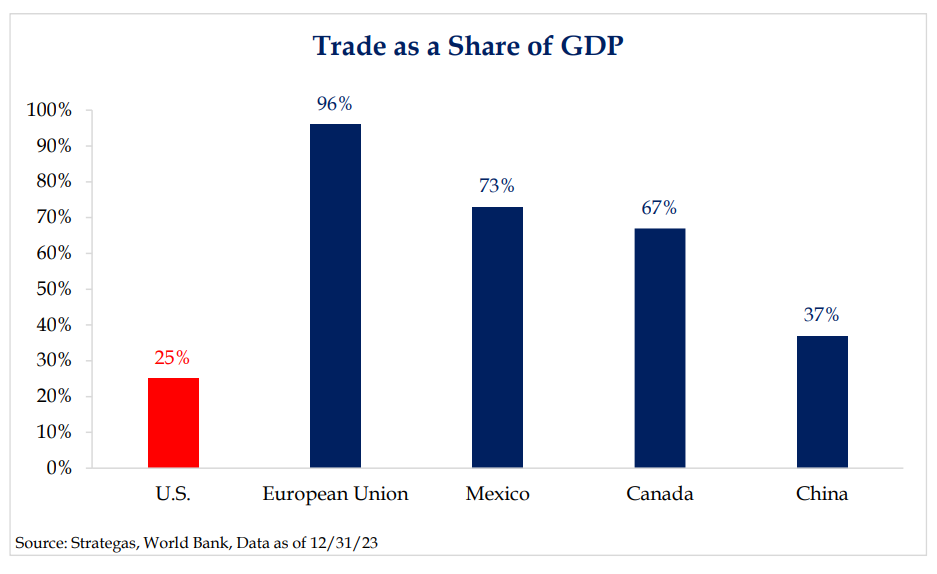

We’re betting on the latter. And the reason for it seems to be clear: the U.S. does have a strong negotiating position on this front. Our dependence on trade as a percentage of our GDP is miniscule compared to most countries.

Past performance is not indicative of future results.

Past performance is not indicative of future results.

But here’s where we get to the market and its reaction to all of this. If we’ve said it in these pages once, we’ve said it one thousand times: markets hate uncertainty! And this process has injected a ton of uncertainty. How do you know where to put your dollars if you’re not confident of the impact tariffs may have on your investment? It’s exceedingly difficult!

And so, the market declined last week as we got closer to the “deadline”, concerned about what might be coming. And it will undoubtedly be volatile this week as we learn more about what is heading our way.

But investors need to take a moment and reset their expectations. This week is not the end of discussion. It will likely not be the market’s “Liberation Day”. There will be more jockeying and more negotiating in the weeks and months to come. So far, our economy has weathered the (limited) new tariffs. But the markets – the most obvious daily price mechanism for our economy – will likely be a rollercoaster as we get more information. That’s why we remain broadly defensive in portfolios. Hopefully, the fear and greed cycle will give us more opportunities to pounce.

Sincerely,