The Weekly Insight Podcast – Can’t Hide From Earnings Season

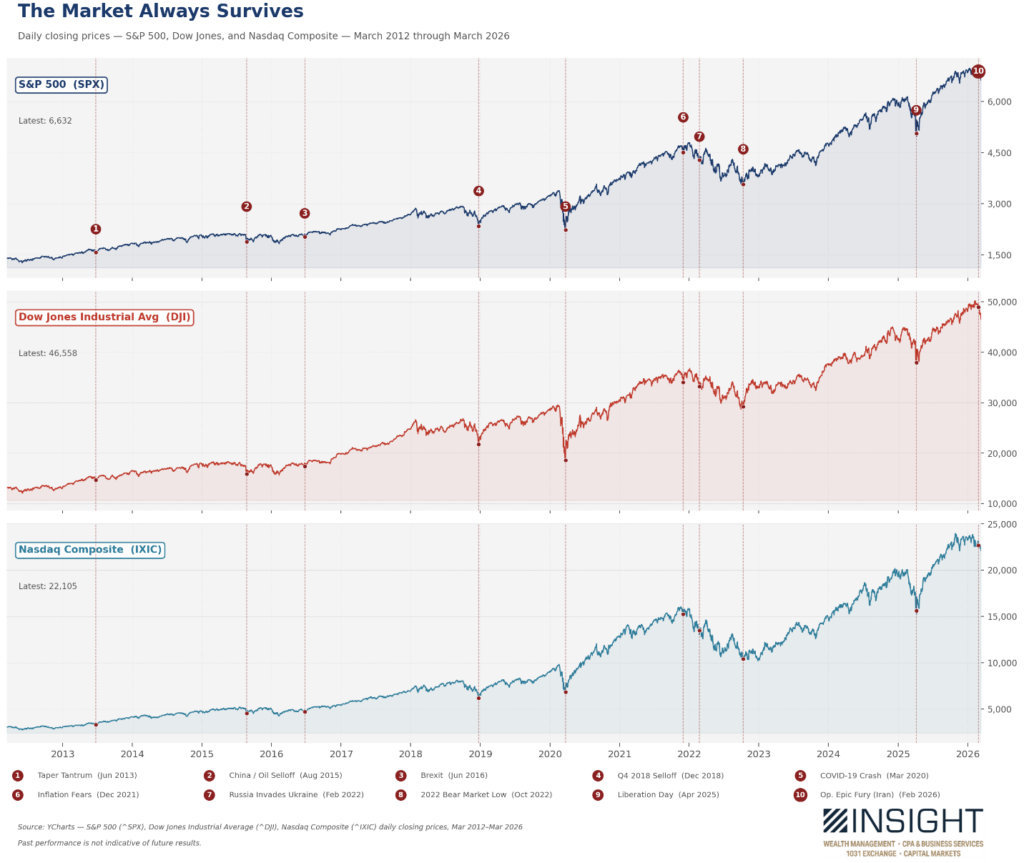

As we sat down to draft this update over the weekend, we were reminded that the Insight Companies just celebrated their 14th anniversary yesterday. And one week from today will be the sixth anniversary of the COVID pandemic stock market lows. Think of all we’ve been through during those periods. Wars, pandemics, volatile elections, inflation, the quickest interest rate hikes in history. Throw in a river turned to blood and a locust infestation (we did have “murder hornets”!) and the last decade starts to look a bit like the book of Exodus.

Before we address the latest plague, we want to remind you of an ESPECIALLY important point: while these events can be scary in the moment, being patient and not letting fear drive your decisions has never been a bad idea. It’s with that mindset that we need to be managing the current set of concerns we have for the market. It’s worked out pretty well for the last 14 years. And it will this time as well.

Past performance is not indicative of future results.

Heightened Expectations for 2026

As we stormed into 2026, no one had a sustained war in Iran as their base case for the geopolitical environment. Even more importantly, market analysts were not weighing any significant risk of the Strait of Hormuz closing for the first time in the history of modern markets. In that sense, this moment is the definition of a “Black Swan.”

Instead, as we entered the year, analysts were incredibly optimistic about the state of the U.S. economy and the outlook for equities. Yes, there were concerns weighing on investors’ minds: a stalling labor market, a weakening dollar, tariffs, etc. But none of them was serious enough to offset the strength in profitability.

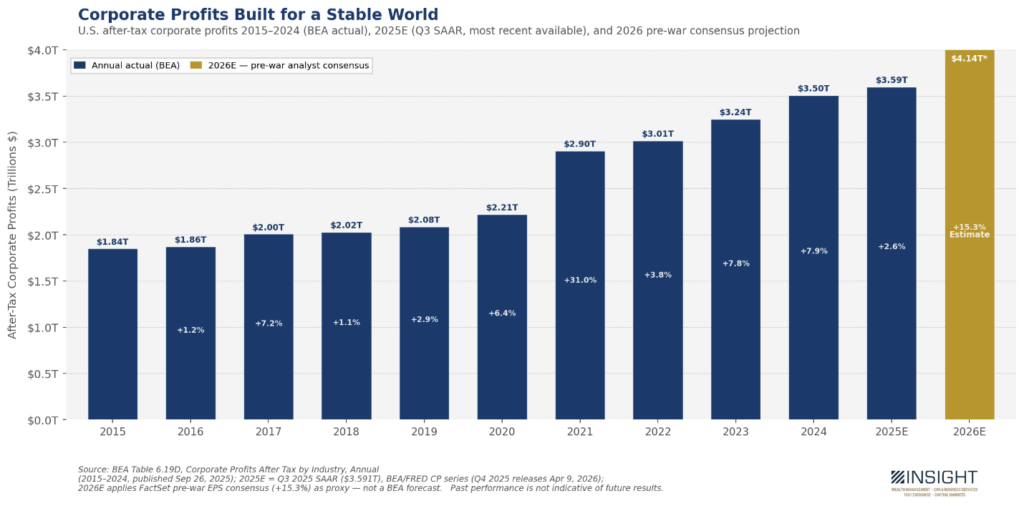

Corporate profits tell an amazing story. Despite all we’ve been through in the last decade, they have steadily marched forward. This is a function of technology, managing economic risk, etc. But it’s notable that we have seen consistent growth for years.

We saw one big spike in 2021 that was due to the massive infusion of cash the government provided during COVID. But even after that – and with the massive increases of labor and input costs caused by post-COVID inflation and 2025’s tariff war – profits have marched forward.

And the estimates for 2026 were that this march would not just continue but accelerate. FactSet is estimating 15.3% growth in profits. Barring 2021, that would be the biggest jump in a decade.

Past performance is not indicative of future results.

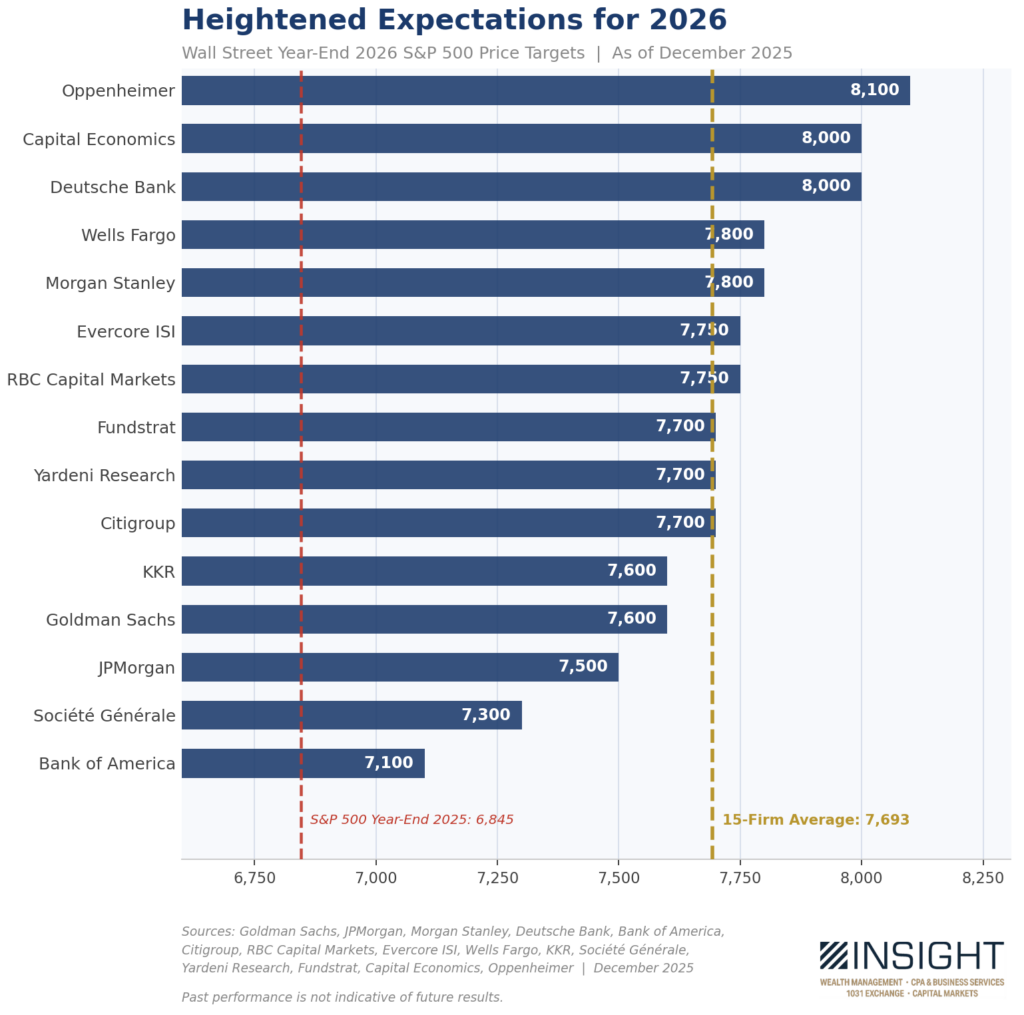

You can understand why analysts were so positive heading into 2026. You’ll remember from our memo in December (Can 2026 Continue the Trend?) that the leading firms on Wall Street were incredibly optimistic about the year. The average expected market outcome was nearly 12.4% for the S&P in 2026.

Past performance is not indicative of future results.

Earnings Season Is Coming

Up to this moment – not much has changed. Yes, the war has increased volatility in the market. Fear has increased – the VIX is up 36.9% since the start of the war and has been as high as 48.5% higher.

Markets though? An incredibly muted response. The worst of the worst – the Dow – is down just 4.9%. The S&P is down just 3.6%. The Nasdaq just 2.5%.

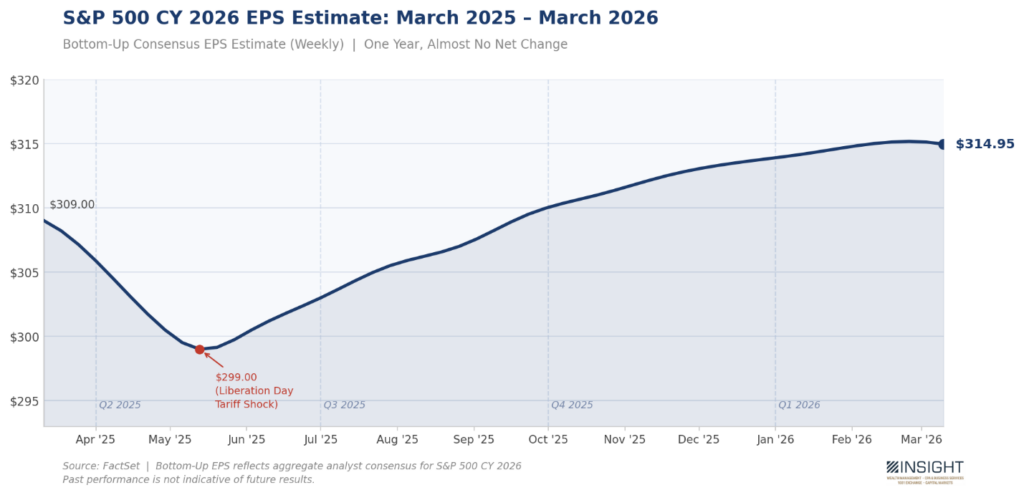

The why – so far – is simple. Estimates for earnings this year have not changed since the start of the war. Everyone is counting on a solid year of earnings. So why would you bail on equities?

Past performance is not indicative of future results.

Think about that for a moment. 20% of the world’s oil supply is…gone. It’s return is not imminent. Petrochemicals touch nearly every product we use.

The phone or computer you’re reading this on? It has petrochemicals in it. It travelled to the store you bought it from using oil. And the electricity you power it with was likely produced burning natural gas. Look around you. Look at the clothes you’re wearing. Look at the food you’re eating. Oil is in some way involved.

And still, earnings expectations have not moved an inch. The market is betting this will all end soon and the world will go back to how it was. We hope so too. But at this point, hope is all we have. The facts don’t care about our hope.

And the facts will start coming in droves in just three weeks. That’s when we’ll begin to fully understand the impact of rising oil prices. Why three weeks? That’s when earnings season begins.

When oil prices rise $30 per barrel (as they have through 3/15/26), the impact is broad. U.S. airlines – all of whom used $88/barrel as their base case for 2026 – must adjust. That’s a big deal considering jet fuel is 25% of their overhead. Earnings will be impacted.

The trucking and freight industry has seen diesel prices rise 36% in the last month. They have started bumping their fuel surcharges – but those typically lag the price at the pump. Earnings will be impacted.

Consumer discretionary & retail companies will feel this as well. Estimates show every $10 increase in the price of oil reduces U.S. consumer spending by 0.2 – 0.3%. At $30 so far, that means a 0.6% – 0.9% drop in consumer spending in just a few weeks. Earnings will be impacted.

We could go sector by sector, but the math is clear: the estimates analysts have been refusing to change do not include an event that bumped up oil prices, creating a drag on the economy and an increase in inflation. The inputs have changed – but estimates haven’t. Yet. In just a few weeks, CFOs are going to start to put real numbers to the impact.

The Good News: This Isn’t 1973 (Yet)

You’ll note we tend to view this event as more impactful than the broader market does. We walked through that reasoning in depth last week (The Old Playbook Doesn’t Apply Anymore). But that also doesn’t mean the world is ending.

The best corollary we can find for this moment is the 1973 Arab Oil Embargo. The impacts of 1973 were significant. It was the event that defined a decade of stagflation. It gave us gas lines, 11% inflation, and interest rates that eventually hit 20%.

It was caused by the removal of 7% of the world’s oil supply from the market. This one – in its scale – is bigger. Roughly 20% of the world’s oil supply is cut off from market.

But scale isn’t everything. Our price move in oil today is 50%.Crude oil prices jumped from $3/barrel to $12/barrel from October 1973 – January 1974. That’s a 400% increase. 50% isn’t fun – but it’s much better statistically. And a swift resolution to this crisis should mute the pain. That’s the bet the market is making right now.

Because of 1973, stagflation is a word you’ve likely been hearing about in this moment. It is defined by a shrinking economy (recession) and rising inflation. There is little mechanism to handle it.

The normal response to a recession is to cut interest rates to incentivize growth. But cutting rates in an inflationary environment is a no-no. It just accelerates inflation. To kill inflation, you need to raise rates (we all remember that!). But if you do that when the economy is in recession…you just deepen the pain.

That is the Fed’s impossible position. We’ll hear a lot more about it this week as they have their next FOMC meeting.

In the meantime, we haven’t seen a 400% increase in the price of oil. So, we shouldn’t panic about a lost decade like we had in the 1970s. Six years ago, we handled a 34% crash in equities in 19 days. The S&P is off just 3.6%.

But if this drags out – and actual data begins to show the pain of the moment – the market is going to have a choice. Hold onto the estimates of old – that included low inflation, an expanding economy, and stable oil prices? Or begin to price in the actual impact of a historically important moment for world oil supply? That choice will define the next quarter in markets.

Sincerely,