The Weekly Insight Podcast – Age-Old Investment Advice

There have been countless books written, articles posted, and speeches made in the last one hundred years about the “rules” investors should live by. Whether it is Vanguard’s John Bogle reminding us that “Time is your friend” or Warren Buffett’s “Be fearful when others are greedy…,” there are some really good nuggets out there. (There are some pretty awful suggestions as well!)

The last few weeks have offered us some excellent reminders of our core philosophies at Insight. Let’s look at a few of them in the context of some great investment advice from the investment advice Hall of Fame.

“Markets can remain irrational longer than you can remain solvent.”

John Maynard Keynes

Let’s preface this with some important context: we do not believe this market is on the precipice of some sort of collapse. We do not think the market is repeating the tech bubble of the late 1990s.

But, as we have discussed before, the market is substantially overweight to just a very few, remarkably similar names. And the concentration is getting more extreme by the day.

Past performance is not indicative of future results.

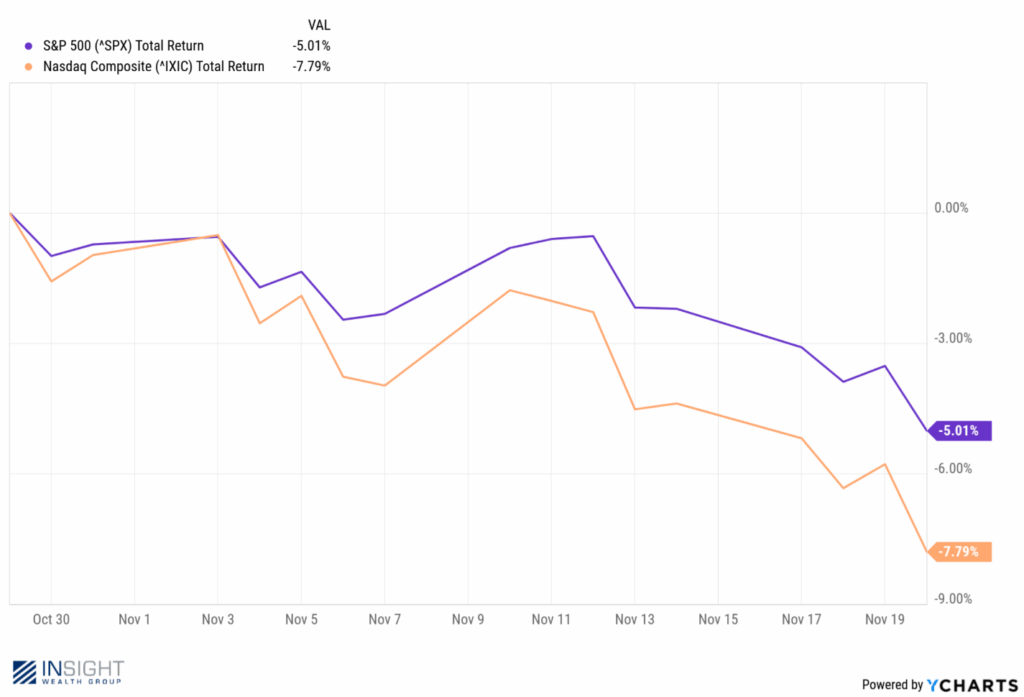

As we have discussed in recent memos, that concentration has started to lead to some concerns among market participants. Specifically, about the cost of buildout for the newly required AI infrastructure and how that expenditure would benefit investors. And it was realized – to a degree – in late October when Meta announced a much larger (and debt financed) spend in 2026. Their stock was punished – to the tune of 12% in a day – which correlated with the drawdown we saw in equities over the coming weeks.

Past performance is not indicative of future results.

You will note in the chart above, however, that markets briefly turned around on Thursday morning. There was one simple catalyst: NVIDA’s earnings.

The NVDIA report had the market on edge at the beginning of the week. Why? Simple: a bad report from NVIDIA would have blown a hole in the AI narrative. A good report – theoretically – should do the opposite. The report was good – they significantly exceeded earnings expectations – but the benefits were short lived.

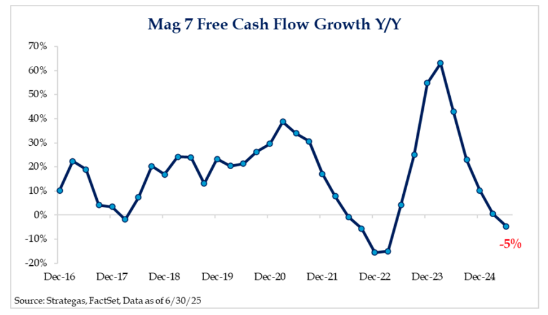

Except for Google – which benefited from the rollout of the latest version of Gemini and Berkshire Hathaway announcing a sizable position in the company – the rest of the Magnificent Seven had a negative week. Some badly.

There are reasons to be concerned. For one, free cashflow for the Mag 7 is declining after massive growth. The reason is the AI spend. But it indicates that the growth cannot go on unabated forever (at least without significant indebtedness).

Past performance is not indicative of future results.

And the market is starting to come to the realization that the future of each of these companies is wildly interrelated. Just look at the graphic below.

Past performance is not indicative of future results.

Start in the right-hand corner of that graphic and focus on the arrows emanating from OpenAI. As the developer of ChatGPT, they are a rapidly growing company. Revenues in 2025 are expected to be between $15 and $20 billion – far exceeding previous estimates.

But note their relationship with Oracle (who also had a bad week last week – down 10.84%). Oracle invested in OpenAI’s “Project Stargate” and OpenAI committed to buying $300 billion in computing power from Oracle. If that was OpenAI’s only expense (it’s not!) – that is a commitment for 15 years’ worth of the current revenue the company generates. Quite the commitment.

Then follow the arrows. Oracle then committed $300 – $500 billion to NVDIA for new chips. And NVDIA turned around and committed $100 billion to OpenAI.

Just imagine for a second that OpenAI flounders. And their ability to spend $300 billion at Oracle evaporates. What happens down the chain from that problem? There is an interconnectedness here that is concerning. And we must manage for it in portfolios.

But the problem – as markets have shown us for a long time – is they are willing to remain irrational for a long, long time. Yes, people are starting to talk about these concerns. But massive blowout quarters like the one NVDIA just had will offset those issues until they stop being theoretical and start being real world. When it happens, the world will be shocked. You shouldn’t be!

“Be fearful when others are greedy and greedy when others are fearful.”

Warren Buffett

Long-time readers have heard us cite this quote since the dawn of this memo. We repeat it because it might be the most important piece of investment advice ever dished out. Why? Because it gets to the psychological barriers that exist for investors. It is those barriers we have been at war against at Insight since our founding.

In some ways, it is at war with the Keynes quote. Keynes is saying, essentially, “you can bet against the market – and be RIGHT – but you still may lose because you don’t have the resources to be right long enough.”

Buffett is saying that, whenever the market feels overly enthused or overly despondent, it is best to bet against that trend. But, with Keynes in mind, you had better have the confidence and wherewithal to wait it out.

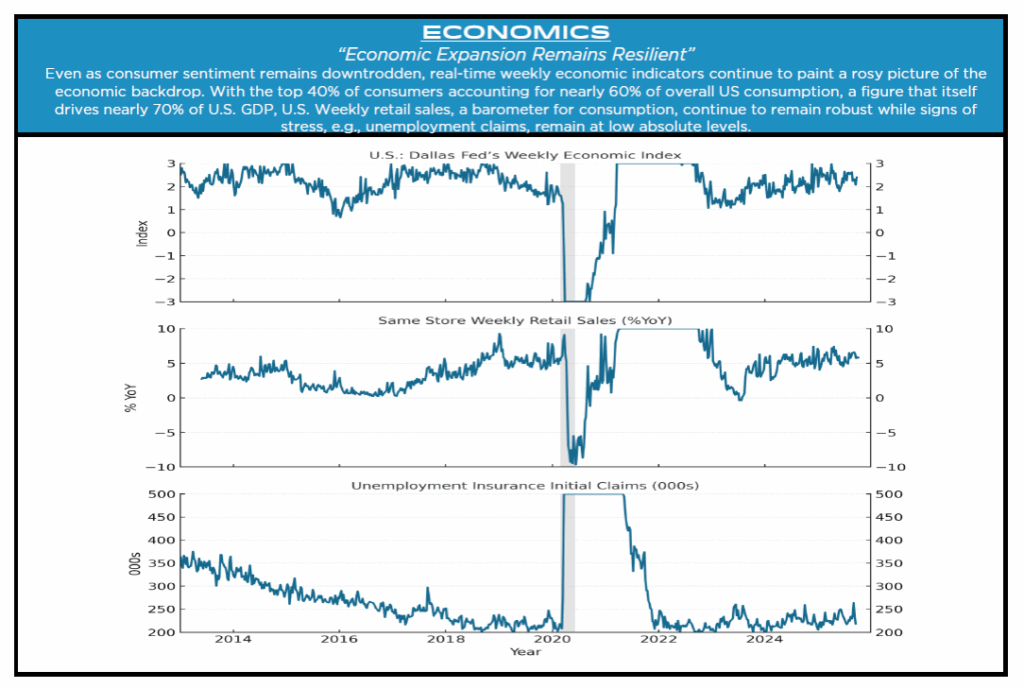

That brings us to the overall pessimism investors seem to have about the broader economy. It showed up in the consumer confidence numbers we talked about last week (second worst ever) and it shows up in discussions with investors who feel like they are just waiting for the other shoe to drop.

There are many reasons for this. The media pushes the narrative. The political environment encourages the pessimism. But are we really about to hurtle off an economic cliff?

Simply put: no. We could show you dozens of charts to back this up (just ask us the next time we talk – we cannot resist our charts!). But this graphic passed along to us last week hits it best. And it comes directly from the Dallas and Atlanta Federal Reserve. The U.S. economy is doing just fine.

Past performance is not indicative of future results.

How Do We Reconcile the Competing Narratives?

That is the most important question. Let’s break it down:

Problem #1: Tech stocks have weaknesses that put their current valuations at risk. But the irrationality of the market may mask that for weeks, months, or even years.

Solution: We cannot avoid 42% of the U.S. stock market! But we can participate while limiting exposure. We do not want 42% of your portfolio tied to the risk that OpenAI (or some other example) cannot live up to its expectations.

Problem #2: Even with the concerns around tech, the U.S. economy remains healthy – but public perception of it is not. How do we manage for that in portfolios?

Solution: While remaining exposed to public markets – look for assets that will be resistant to short-term market volatility. And have plenty of dry powder in portfolios ready to pounce if a short-term corrective action happens. That is exactly what we are doing.

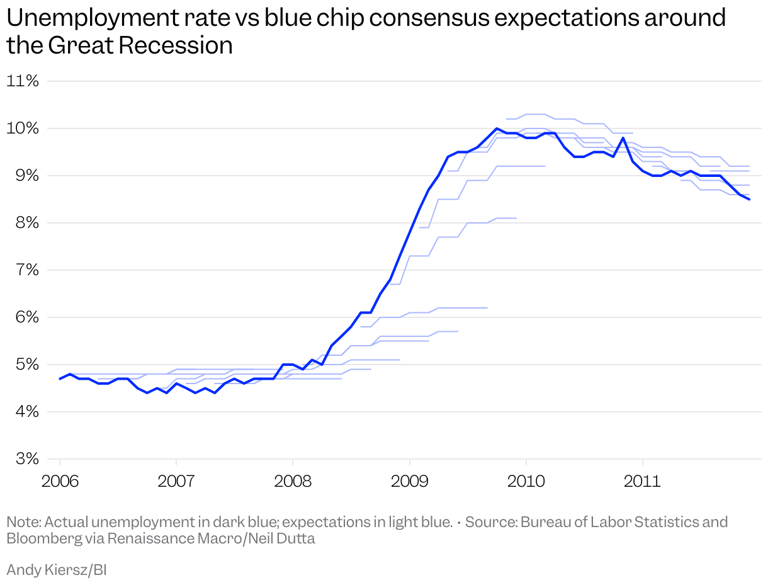

We remain unconvinced the “world is ending.” Then again, we must be intellectually honest enough to understand we do not know everything. It’s why we always remember charts like the one below. Back in 2008 the “experts were wildly wrong about what would happen in the labor market.

Past performance is not indicative of future results.

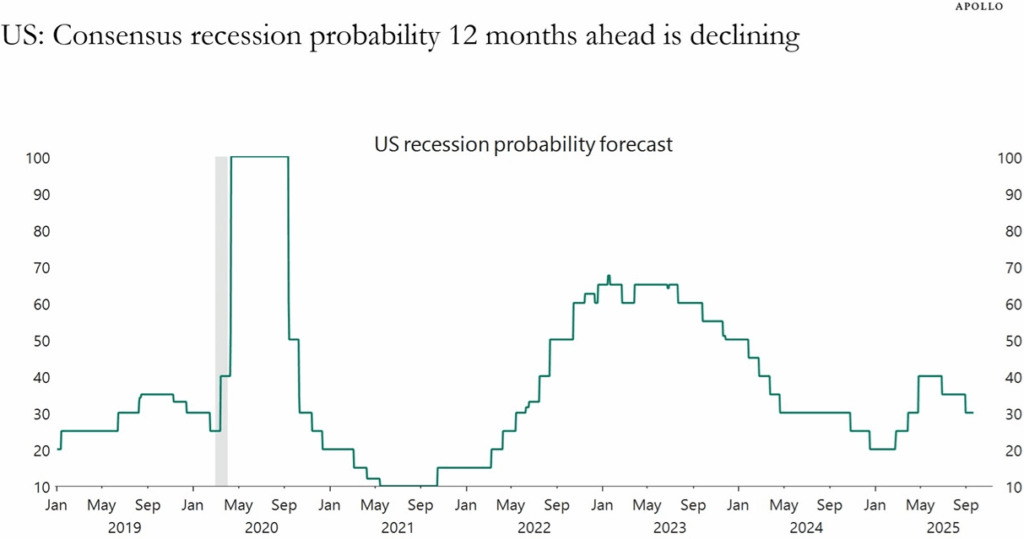

And for the last several years, those same experts have been wildly wrong about predicting the next recession.

Source: ApolloAcademy.com

Past performance is not indicative of future results.

And so – even in exceptionally good years like this – we must balance the irrational optimism at the top of the market with the irrational pessimism on our economic condition. It may not be the sexiest story to tell in memos like these. But it matters more where it counts: your portfolio statement.

Sincerely,