Another week, another COVID-19 memo! As if you haven’t already heard enough about this crazy disease, right?

Last week was a good week in the markets overall (see below), but we know as you do, that this has been a historically bad month for portfolios. There has been no place to hide. There are no asset classes that have been sheltered from the fear and irrational pricing that has permeated the markets. But we also know from our years of experience, that now is exactly the time when we must force fear out of our thinking and focus on the facts on the ground.

Our Investment Committee has been meeting daily to first triage any problems that exist in portfolios, but more importantly to position you – and all our clients – to take advantage of the inevitable recovery. It will take patience to work through this process, but we will be with you every step of the way.

We hope these memos are providing some bit of additional perspective – especially on how we’re managing your money. This week we’re going to try to keep it a little bit shorter as we focus on a few very important areas: the impact of the federal stimulus bill (the CARES Act), what you should be aware of personally from the bill, and our plans for your portfolios over the coming weeks.

The Impact of Federal Stimulus

We hope your opinion of Insight over the years is a firm that doesn’t do much hyperbole – and instead focuses on what we can know with certainty and how best to deal with those facts to your benefit. The last month, however, is a time when the facts are wilder than any hyperbole, we could have imagined just a few short weeks ago.

As the virus has grown rapidly both in the U.S. and around the world, governments have responded. We can all debate when this is over whether the response was measured and appropriate. That won’t be known until this is all behind us. What we can’t debate, however, is that the Federal Reserve as well as federal, state and local governments have unleashed both barrels to prevent the economy from crashing.

This week the biggest guns yet were rolled out. The Federal Reserve announced new emergency measures on Monday with the goal of supporting the economy and ensuring that households and businesses can have access to credit. It has been aggressively adding to its balance sheet. In just the last two weeks, it has purchased $942 billion in treasuries and mortgage backed securities.

In typical Fed fashion, any announcement they make seems to result in a down day at the market. Monday was no different. But on Tuesday, the stock market started to see the fiscal stimulus from Congress begin to take shape and reacted in a strongly positive way. The S&P 500 was up nearly 18% from Monday’s close to Thursday’s close – all in anticipation of a final bill passing both houses of Congress and going to the President.

As everyone knows by now, the bill Congress passed, and the President signed – the CARES Act – pushes over $2 trillion back into the hands of taxpayers and business owners in an attempt to minimize the impact the virus has had on the economy. But more importantly – if you combine the monetary stimulus from the Fed with this bill – we have seen over $6 trillion committed to prop up the economy.

While the numbers seem huge, it is important to put them in perspective. We have seen wildly fluctuating predictions for what the impact of COVID-19 will be on the economy. Most economists have been predicting negative GDP growth of somewhere between -5% to -15% for the 2nd quarter. The most dire prediction we’ve seen so far is -24% by Goldman Sachs.

Let’s assume the worst-case scenario of -24% GDP growth in Q2. If that were to happen, it would cost the economy roughly $1.2 trillion. That’s a big number, no doubt. But in their scenario they are expecting a surge in Q3 and Q4 of 12% and 10% respectively, resulting in negative GDP for the year of 3.8% meaning we’d have a total drag on the economy of less than $200 billion – a hole which is being filled with $6 trillion in cash and lending. This is a very serious stimulus program.

The problem is no one knows how accurate the GDP numbers will be. We mentioned the unemployment numbers coming out this week in our last memo and noted that the worst-case scenario was 2.5 million in new unemployment claims. The number came in at 3.3 million. No one has models that are designed for this type of scenario and – until the virus is under control – we won’t truly know how badly the economy was damaged.

What Now for Portfolios?

In our memo last week, we discussed our main inflection points for portfolios and noted:

“In our opinion, there are two key points at which we can begin to understand what the bottom of this market looks like: the release (and market reaction to) the fiscal stimulus plan from Washington; and the moment we get to “net negative new infections” from COVID-19 domestically.”

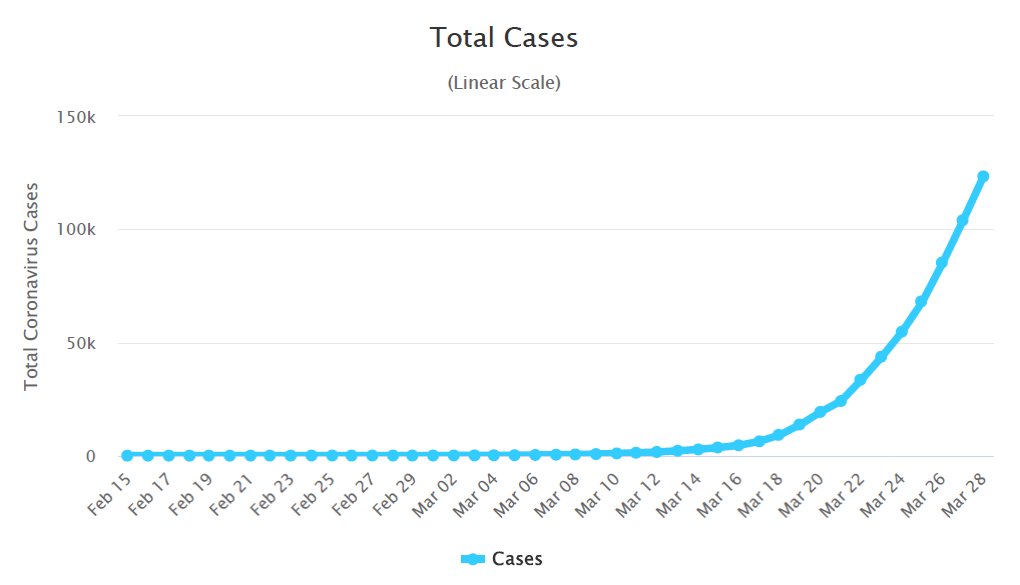

We’ve now hit the first of those signals with the passage of the bill on Friday. As noted above, the bill and the Federal Reserve’s actions put a backstop on the economy for the time being, essentially putting a limit on what the worst-case economic scenario could be. But the real headline risk still exists: how bad will this virus get. The U.S. famously moved into “1st Place” (doesn’t seem like such a great win…) for total number of COVID-19 cases around the world amid a week that saw cases spike all over the world. From March 21st – March 28th we grew the number of total cases nearly 5x domestically – from 23,720 to 118,126.

Probably more importantly, the number of new cases identified every day has also been climbing unabated from 4,825 on March 21st to 19,452 on March 28th. It is certain that the advent of new and better testing has impacted this to some degree, but the simple answer is we haven’t beaten this yet.

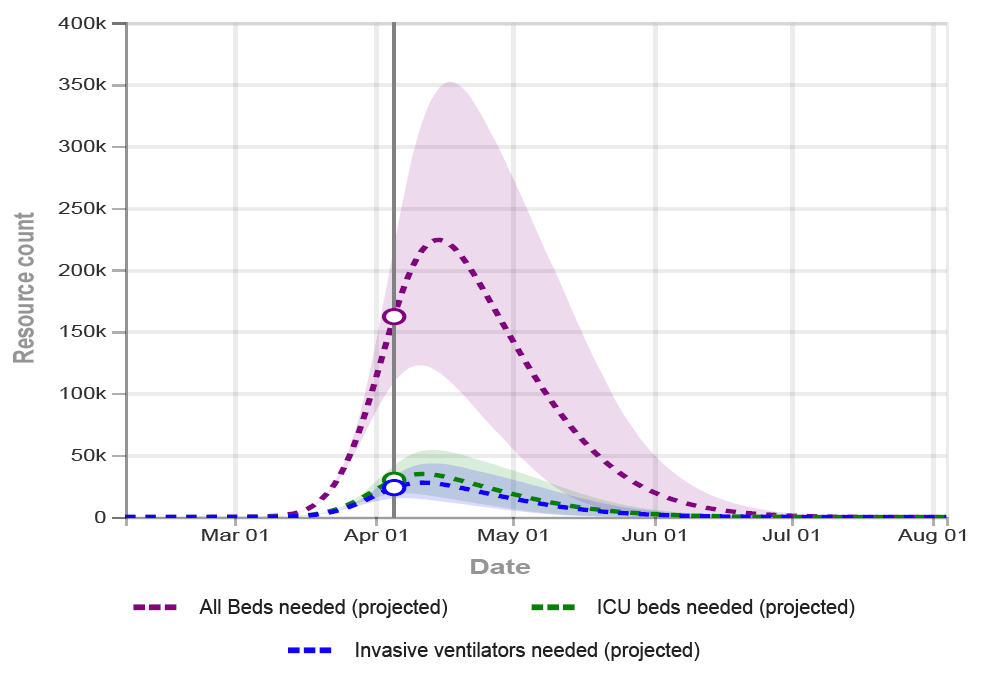

The latest projections from the Institute for Health Metrics and Evaluation (the same data the famous Dr. Fauci has been referencing), are currently showing a peak of hospital resources needed (i.e. new admissions, ICU beds, ventilators) in the United States at roughly April 15th, two weeks from now. While it isn’t a perfect corollary to “net negative new cases”, that data point would seem to be a strong guide.

The IHME data is particularly interesting when you look at it from a state-by-state basis. We would encourage you to take a look via this link: https://covid19.healthdata.org/projections. You will note that in some areas, like Iowa, resources will not be badly strained. For us, they anticipate needing 434 beds and 65 ICU beds at the peak of infection. We have access to 4,297 beds and 246 ICU beds, so it should not be an issue. In New York, it is a much different story as they anticipate needing 58,564 more beds and 10,352 ICU beds than they have available.

While there have been some – the President most prominently – aiming for a quick end to our current social distancing regime, we believe we have to assume a somewhat more extended version – at least on a regional basis – until these numbers can be brought into check. This was confirmed yesterday when the White House pushed back their timeline for social distancing from April 15th to April 30th. Even if the cases peak, we can’t assume it’s “all over” as there is a risk of a second wave.

As such, while the stimulus efforts in Washington give some optimism to our outlook, the headline risk of the virus and current market conditions still require a cautious approach. We have been having daily Investment Committee meetings to identify opportunities within the portfolio. There will come a point – we believe soon – where we will look to reposition our portfolios to their targets allowing us to take advantage of dislocations in the equity markets.

That said, bid/ask spreads in fixed income are still too wide to justify moving away from those positions today. As monetary and fiscal stimulus begin to work their way into the market, those spreads should narrow – meaning the fixed income recovery will lead the equity recovery. We anticipate that will be long before the headline risk of the virus has evaporated and will still allow for substantial upside to portfolios. Simply put – at this point it makes sense to put cash to work but doesn’t make sense to sell any fixed income assets to buy equity assets.

We will continue to monitor this situation daily and reserve the right to move quickly when the irrational pricing of fixed income begins to close. In the meantime, if you have any questions related to your individual allocation, please don’t hesitate to let us know.

What Does the CARES Act Mean for You?

We’ve been working with consultants, lawyers and bankers all week trying to get a full understanding of the CARES Act passed by Congress Friday. In any bill as extensive as this, more details will roll out in the coming days. And – more importantly – the Treasury Department has 10 days to define the rules around the bill. We anticipate them moving quickly to get money in peoples’ hands, but to say we know exactly how that is going to work at this point would be untrue.

But anytime something as substantial as this comes out, we feel it important to outline for you the ways you can take advantage of the opportunities presented both as an individual and – for many of you – as a business owner. We’ve attempted to hit the highlights below. More information will certainly follow as we learn more. And it should be noted, there are many yet unknown tax consequences from some of these rules. This is not meant to provide tax advice and we would highly recommend you talk with your tax preparer before undertaking any of the items noted below.

1. Cash Payments to Individuals: The big headline from the bill was the cash payments that will be going out to individuals. Not everyone is going to receive a check. There is an income limitation on the payments and payments will begin to phase out when an individual exceeds $75,000 of AGI or a household exceeds $150,000 AGI. Those figures will be based on your 2018 tax return filings. If you fall below those thresholds, adults will receive $1,200 each and children will receive $500. This is a one-time cash payment and will likely be considered taxable income on your 2020 tax filing.

2. Unemployment Benefits: The bill makes broad changes to unemployment assistance including adding a federal benefit and broadening who is eligible. While states will still pay unemployment for people who qualify, the Federal government is now going to add $600/week for four months to whatever the state pays. Today, the nationwide average for unemployment is $340/week meaning people will receive four months of benefits averaging $940/week or the equivalent of a nearly $49,000 per year annual salary.

Additionally, the bill allows people who have not previously been eligible for unemployment (i.e. contractors who receive a 1099) to have access to unemployment benefits.

3. Payroll Protection Plan: For small business owners, this is probably the biggest benefit in the bill and one that should be researched thoroughly. We will send more when the final rules are available.

The way we understand this program today, it will provide a forgivable loan equivalent to 2.5 months of payroll, rent or mortgage payments, and utilities for any small business. This loan would be completely forgiven if, on December 31, 2020, you had the same number or more employees than you had prior to the COVID-19 outbreak. If you have had layoffs during that time, you would only be responsible for paying back a percentage of the loan. For example, if you had 10 employees before the outbreak and laid off 2, 80% of your loan would be forgiven.

To put this in perspective, imagine you own a small business with 20 employees who average $50,000/year in salary. Your monthly payroll would be roughly $83,000. Assuming a monthly rent payment of $5,000, you would receive a payment of $220,000 which could be completely forgivable. We highly recommend all business owners taking a close look at this program when the application process becomes available.

4. Changes to Retirement Accounts: Congress instituted a broad number of short-term changes for retirement accounts (i.e. IRAs, 401(k)s, etc. They include:

a. Required Minimum Distributions for calendar year 2020 are waived and you can keep the funds inside your IRA, 401k, etc.

b. Hardship distributions for COVID-19 are allowable without the 10% early withdrawal penalty for up to $100,000 for any individual diagnosed with COVID-19, whose spouse or dependent is diagnosed or who experiences adverse financial consequences from being quarantined, furloughed, laid off, etc.

c. 401(k) Plan loan limits are doubled to the lesser of $100,000 or 100% of their plan balance.

d. 401(k) plans that do not allow loans or hardship withdrawals in their plan document can do so immediately as long as the plan is amended in the next plan year

5. Small Business Loans: Iowa is one of the few states already identified as a “disaster area” and eligible for SBA disaster loans. We anticipate this will be expanded to all states in the coming days and weeks. The SBA disaster loan program allows for up to $2,000,000 in loans that bear an interest rate of 3.75% over a 30-year term. There is some question as to the eligibility for this program in conjunction with the Payroll Protection Plan. Many bankers are recommending looking at the Payroll Protection Plan first and then at disaster loans. Please note we received a notice from the SBA this morning that loans are not yet available and they will “notify lenders as soon as program details become available”.

6. While not technically part of the legislation, it is an important thing to note: The Treasury Department has delayed the tax filing deadline for 2019 taxes to July 15th. There is no penalty or interest accumulating during this time.

As always, there is a lot to digest each week as we work our way through this process. We hope you’re hanging in there through this time of “social distancing”. It’s just a weird time! But we would encourage you to stay home, relax and help us all “flatten the curve”. In the meantime, we will continue to be available to you at your convenience.

We are continuing to split our staff between the office and home during this time and are prepared – if Iowa were to go into a “shelter in place” order – to have our entire office work remotely. No matter what happens, you will always be able to trade, access funds, etc. If you need anything, please don’t hesitate to give us a call or drop us an email.

Sincerely,