The Weekly Insight Podcast – Being Right Isn’t Enough

“There is nothing so disastrous as a rational investment policy in an irrational world.”

– John Maynard Keynes

John Maynard Keynes is the godfather of modern economic thought. The COVID bailout? It was his idea, nearly 90 years before it happened. Government intervention in interest rates? That was him, too. One could argue (we would agree!) that governments have perverted his original ideas causing massive deficits. But you can’t argue that he was a brilliant economist who has, quite literally, changed the world with his ideas.

Keynes’ fingerprints were all over world affairs during the first half of the 20th century. But he was also an accomplished investor. After leading the charge against the Versailles framework that eventually led to Germany’s shift towards fascism (he was right!), Keynes the investor lost his fortune in highly leveraged currency positions (which – knowing Keynes – he was probably right about as well).

Keynes felt this viscerally. Thus, the quote which serves as an important reminder to us about how markets – and economies – work. Put simply, the market doesn’t care if you’re right.

We’ve seen it play out repeatedly. The smartest people in the world have the best idea about how to make money – or save it – in a volatile world. They have information and access to assets. And no matter how correct they may be, the results don’t pan out.

Take Long-Term Capital Management (LTCM). LTCM was a hedge fund started in 1994 by John Meriwether, the head of bond trading at Salomon Brothers. Meriwether was a legend. But LTCM didn’t just have one legend. They also employed Myron Scholes and Robert Merton who both won the Nobel Prize in Economics in 1997 while working at LTCM.

LTCM’s strategy was “convergence trading.” They would find pairs of bonds that were similar and mispriced. They would short the expensive one and buy the cheap one. As the price converged, the goal was to make money on both sides of the trade. It was – in theory – low risk and a near mathematical certainty.

Given the “low risk,” LTCM levered it up. For every dollar of actual capital at play, they borrowed $25. By 1998 they had $125 billion in assets deployed.

That was the year Russia defaulted on its debt. Investors panicked. The spread between LTCM’s positions exploded. The market got more irrational.

It got so bad, the Federal Reserve had to orchestrate a bailout of LTCM to avoid a collapse of the entire bond market. They lost 90% of their investors’ capital in four months. And, just a few months later, investors who owned LTCM’s old positions made a fortune. LTCM was right. They just couldn’t wait long enough.

The story has repeated itself time and again. Julian Robertson’s Tiger Fund was screaming loudly about the dot-com bubble. We all know how right he was, but he couldn’t hold out. The fund was forced to close on March 30, 2000. One year later, the NASDAQ was down over 58%. He was right.

Or there was George Soros. He, too, agreed the tech bubble was a farce. By the end of 1998 he had lost $700 million betting against internet firms. But after underperforming while the market ran wild, he capitulated and piled into tech stocks. You can imagine how that ended. He was right. Then the pain of watching the market prove him wrong became too much and he bought at the top. Even the wealthiest capitulate and it’s never a good idea.

And…here we are again.

Very smart people have said for a very long time that the closure of the Strait of Hormuz would be an economic nightmare. Oil prices would shoot up. The market would crater. A recession would begin. It was – in theory – one of the worst man-made events one could consider that would impact the world economy.

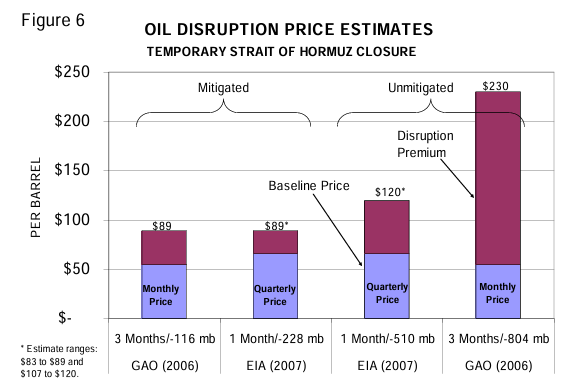

Back in 2007, the Joint Economic Committee of the U.S. House of Representatives released a report from the office of their ranking member, Jim Saxton, a Republican from New Jersey.

In it, they outlined exactly what we and the world have been saying for some time about the Strait. If you’re really interested, you can read it here, but the summary is this: You won’t be able to believe it was written 19 years ago. They’re talking about the exact same things we’ve been talking about today. Shifting supply to the East-West pipeline buys us some time. Releases from the Strategic Petroleum Reserve will be necessary, but declining. The same playbook we’re seeing today.

They even show the impacts on oil prices in a “mitigated” and “unmitigated” situation that look amazingly similar to what we’re seeing with oil prices today.

Source: The Strait of Hormuz and the Threat of an Oil Shock; July 2007; Joint Economic Committee Report, U.S. House of Representatives

Past performance is not indicative of future results.

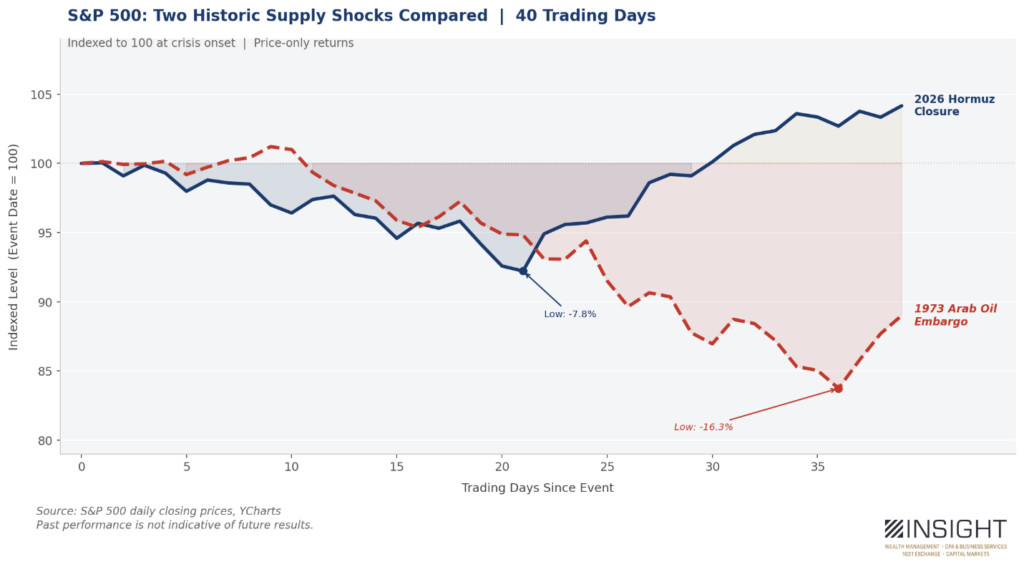

Since this was written, we’ve seen oil scares. But the Strait has remained open, and we haven’t seen a disruption of supply comparable to this moment. And, truly, the only real comparable before or since to what we’re seeing today is the Arab Oil embargo. Not surprisingly, the market reaction at the start was nearly identical to what we saw in 1973.

But the reaction since March 30th has diverged sharply.

Past performance is not indicative of future results.

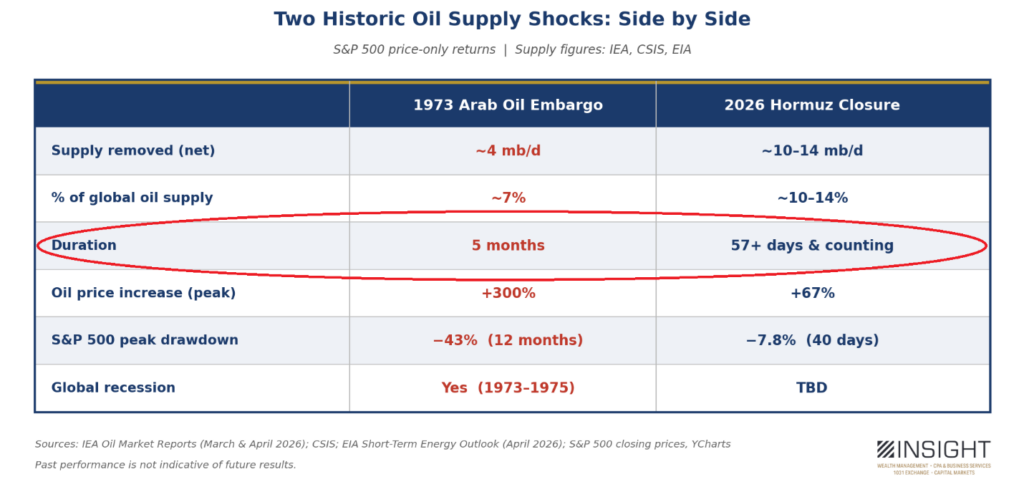

If you take that chart out a full year, the 1973 results get worse and worse. Less than a year later the S&P 500 was down more than 43%. Given the oil embargo had roughly half the impact on global oil supply of the current closure, that should give us pause.

Past performance is not indicative of future results.

The oil embargo removed 7% of supply and the market dropped 43%. The current closure of the Strait has removed 10% – 14% of supply and the market is…up!

The market has clearly made a bet. It’s not the size of the disruption. It’s on the duration. Simply put, they’re convinced this is going away.

So, what are we to do? There are two camps you could be in. In Camp 1, this looks like 1973 and a recession is imminent. In Camp 2, the economy keeps chugging along and a negotiated settlement in Hormuz helps us avoid the worst of the pain.

Neither side is wrong…yet. One will be. And one will be right. But as Keynes, LTCM, Tiger Fund, and George Soros have taught us, being right isn’t a guarantee of success.

Instead, we must balance the risks. You’ll note that every single one of the examples of “being right too early” was an incredibly one-sided trade. They worked or they didn’t. You made a lot of money, or you lost it all.

But that’s not necessary. Our overweight energy position – if the Hormuz closure drags on – will balance the risks to the downside of a recession as will our exposure to treasuries, short-term high-quality bonds, and cash. Our growth and international exposure will provide upside if a resolution emerges and flows through the Strait resume.

It all comes back to thinking you’re smarter than the market. You may be. We may be. But it really doesn’t matter when our old friends, fear and greed, kick into gear. And so, we protect where we can. We take our shots where we can. Because being right isn’t enough. You also must understand the motivations of the market and exactly how it can prove you wrong.

Sincerely,