The Weekly Insight Podcast – The Market Moved On. The Strait Didn’t.

Three weeks of rallies. One weekend of attacks on shipping. And we’re back to the same discussion.

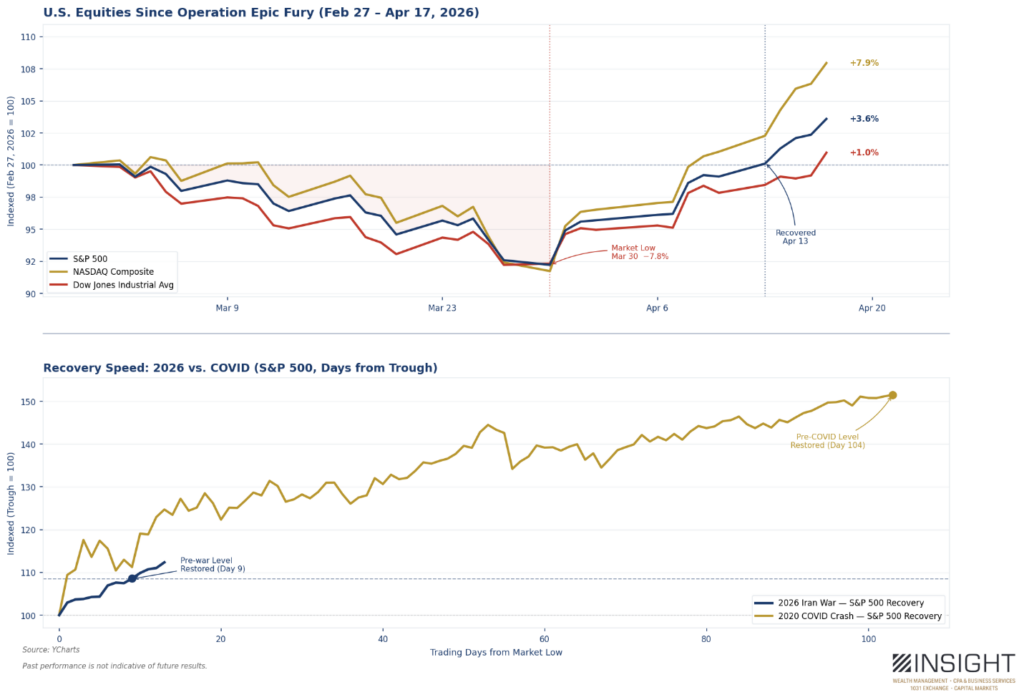

Markets have gone for quite a run. It took just nine days to erase the deficit created by the closing of the Strait of Hormuz. In the last two weeks, a ceasefire with Iran was agreed upon. Equities rallied. Oil prices collapsed. The market was moving on.

Past performance is not indicative of future results.

The COVID recovery noted above was – at the time – one of the quickest bounce backs we had experienced. Yet it still took twelve times longer than what just happened around this war. The reversal was swift and convincing.

But then this weekend happened. And the narrative shifted – yet again – on what the end of this conflict looks like.

Ceasefire No More?

April 22nd – this Wednesday – is the technical end of the ceasefire. If no deal is reached by then, the parties are no longer obligated by the terms.

It seemed that didn’t matter. While there will certainly be some he-said/she-said on this matter, the timeline over the weekend looks like this:

Friday, April 17: Iran declares the Strait of Hormuz “open for commercial traffic”. Markets soar (S&P up 1.4%) and oil plunges 10% with Brent crude hitting five-week lows at $90.38.

Saturday, April 18: Iran reverses the reopening, imposing what it called “strict management and control” over the Strait. It opens fire on vessels attempting to pass and blames it on the U.S. refusing to lift its blockade of Iranian ports. Two Indian- flagged ships were targeted and forced to turn back, including the VLCC Sanmar which had received Iranian approval to pass before being struck with rockets.

Sunday, April 19: Further escalation. President Trump announces that the U.S. fired upon and seized the Iranian-flagged cargo ship Touska after the crew refused to stop. He also threatened, again, to “knock out every single Power Plant, and every single Bridge, in Iran” if they don’t agree to a deal.

And so, the ceasefire is effectively dead. At least for now. Oil was already up more than $7 on Sunday afternoon. Equities will likely be down Monday morning.

U.S. and Iranian delegations are heading back to Pakistan to continue talks. This weekend’s fireworks are posturing as both parties position to get what they want out of these negotiations. But Wednesday will be yet another important deadline the market will have at top of mind.

Does Any of It Matter?

That’s the big question we must ask ourselves as this standoff continues. None of us are invited into the negotiations, so it’s hard to predict exactly what results will look like or when they will happen.

But the market has already made its determination.

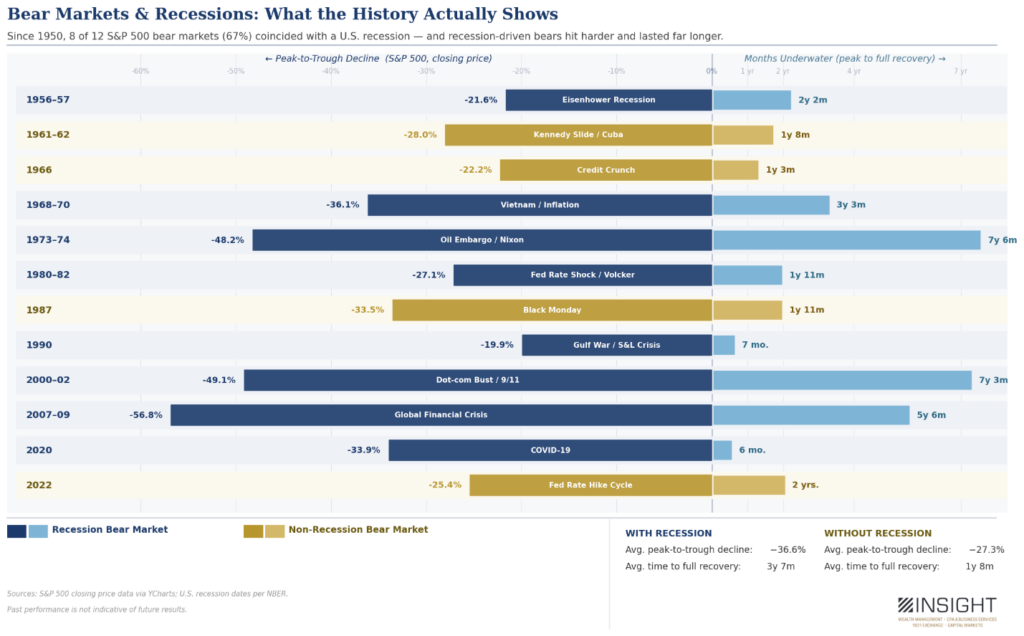

We talk all the time in these pages about how the biggest of the “big things” is being able to understand the likelihood and onset of a recession. Why? They greatly impact market performance.

Sometimes bear markets have occurred without a recession. Those have been event-driven moments: sharp, painful, and quickly over. The Cuban Missile Crisis, Black Monday, etc., etc.

But the length and breadth of a recession-driven bear market is substantially worse. And it’s not even close. Recessionary bears fall more than 9% further and last nearly two years longer.

Past performance is not indicative of future results.

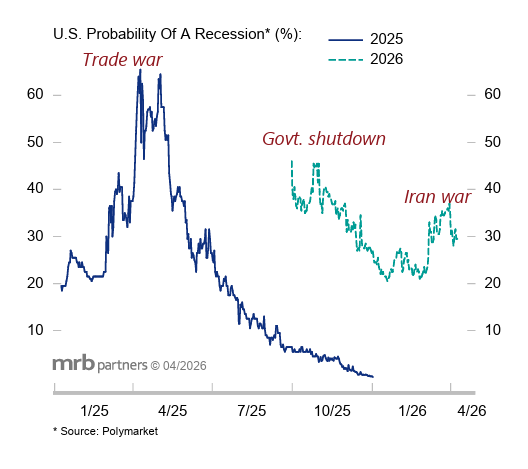

Recessions matter to portfolio returns – likely more than anything else. And for years, analysts warned that a sustained Hormuz closure would trigger a recession. That’s a bad combination of data sets.

It turns out, the market doesn’t buy it. The chart below makes the case. The odds of a recession were significantly higher during the trade issues last year and the most recent government shutdown than they ever got during the Iran conflict.

Past performance is not indicative of future results.

What the market is saying – by both its incredibly quick recovery and its low odds of a recession – is essentially “This, too, shall pass.”

Signals Are Still…Mixed

The good news is the impact these market returns are having on portfolios. Our defensive positioning worked quite well and the uplift from the markets is just adding to the results.

But while the fear in the market a month ago was never a reason to panic, the run for the last few weeks is not an excuse to set aside all defensive positioning. Why? The market is pricing the physical opening of the Strait, but not the potential long-term impacts.

First, as noted above, the core problem is still not behind us. The Strait of Hormuz – and it’s 20% of world oil and LNG supply – is still closed. Completely. Until it is fully and transparently reopened, the risk remains.

Second, no one is yet having a real discussion about just how long it will take to normalize flows through the Strait once it is reopened. The market is treating this problem as “The Strait is Open = Problem is Solved.” It’s not that simple.

Yes, some oil will flow immediately. But we’re really looking at a multi-step process:

Days to Weeks: Recent estimates show that around half of the shut-in upstream production could restart within days of the Strait being truly opened.

Months: There are multiple significant oil and gas infrastructure pieces that have been damaged during this conflict. Bahrain’s Bapco facility with 400,000 barrels per day (bpd) is closed. Kuwait’s Mina Al-Ahmadi has been hit by multiple strikes. The UAE’s Ruwais refinery – one of the world’s largest – was hit by multiple drone-linked fires.

According to Wood Mackenzie senior analyst Priti Mehta, for these facilities, the “restart process will require longer duration to stabilize.” The same goes for shut-in oil fields. Those supply channels could take months to restart.

Years: This is the biggest one the market isn’t talking about: the Ras Laffan LNG trains in Qatar. Seventeen percent of Qatar’s total export capacity was destroyed by Iranian strikes and will require repairs lasting as long as five years.

Even with these extended timelines, Wood Mackenzie predicts a quick turnaround if things go back to normal. Their current projection shows oil averaging $89 in Q2, $75 in Q3 and stabilizing back to $65 for full year 2027.

In the meantime, we still don’t know the full extent of the damage to the economy. Recent economic signals have looked better than some may expect. The March jobs report reversed February’s negative trend and exceeded expectations. Same store sales continue to grow as does consumer spending. Record breaking tax refunds are hitting this month.

The impact of these higher oil prices has yet to be felt. But the March CPI report was instructive. Core CPI remains low, rising to just 2.6% year-over-year. But all-items CPI, which includes energy, spiked 0.9% in the month of March and sat at 3.3% year-over-year. When you account for that, real wages (month-over-month) in the U.S. fell for the first time since our last battle with inflation in 2022.

The question we all need answered is simple: is the Wood Mackenzie data correct? Will oil prices be fully recovered a year from now? If so, the upside is real. Wages will recover nicely and so too will equities. If not, our big recession question may become a real concern.

Past performance is not indicative of future results.

The market has already done the easy part — it priced in the best-case scenario. Everything from here is execution risk. Does the ceasefire hold? Does the LNG infrastructure come back faster than expected? Do oil prices fall to Wood Mackenzie’s $65 target by next year? If the answers are yes, markets are fine. If the answer is no, this rally could reverse as quickly as it recovered.

We don’t know the answers. Neither does the market. What we do know is that asymmetry like this — where the upside is already in the price and the downside is not — is exactly when disciplined positioning earns its keep. We’re keeping ours.

Sincerely,