The Weekly Insight Podcast – We’ve Been Here Before

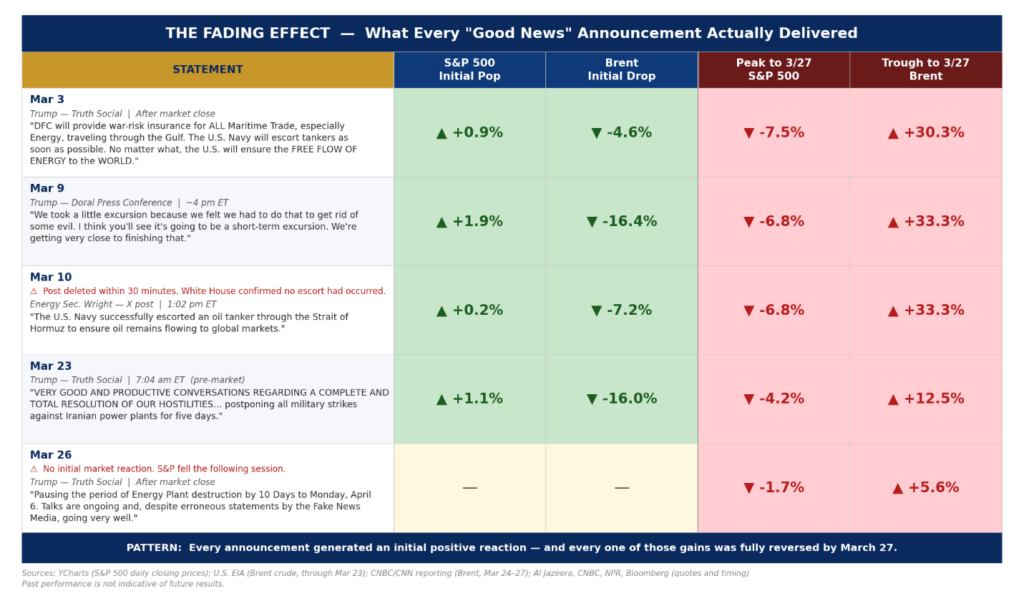

The pattern is clear. The market digests information about the war in Iran, its impact on oil supply, and the state of the global economy, and begins to fall. The White House then releases some sort of statement or plan to buoy market opinion and a brief rally begins. That rally is quickly overwhelmed by facts on the ground and the decline continues.

As we pointed out last week: no one knows what’s really going on. The only people that do are the ones sitting in the White House, the Pentagon, and scattered throughout Iran. Are the current negotiations serious? Are they close to an outcome that both sides will accept?

How long will the rhetoric be able to offset the facts on the ground? Friday answered that question. The market’s tolerance for White House optimism is fading.

Past performance is not indicative of future results.

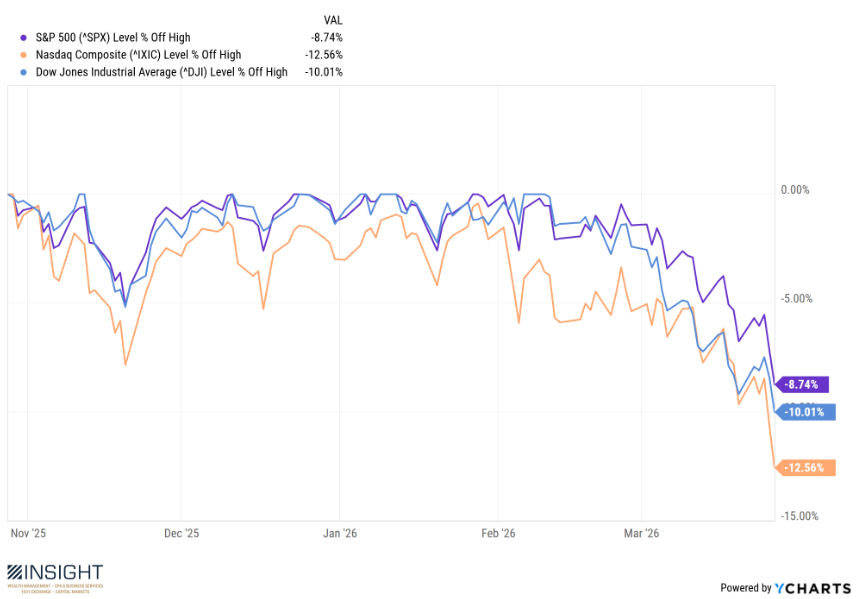

And that led to the scary headlines over the weekend. Markets – specifically the Dow and the NASDAQ – have entered “correction territory.” As the definition goes, they’re down more than 10% from their highs. The NASDAQ – which set its high back on October 28th – is down 12.56%. The Dow is down 10.01%. And the S&P – while not in correction territory – is down 8.74% from its high.

Past performance is not indicative of future results.

Almost six years ago to the week, we were dealing with similar issues. During COVID, the markets bottomed on March 23, 2020. It was a nasty fall, with the S&P dropping 34% in just over a month.

It was a proving ground. Was the world as we knew it ending? Would markets ever recover? Would our loved ones survive? Bluntly, it was the scariest market moment in the history of our firm. And one of the most important moments to understand when we face issues like we’re having with Iran and the oil markets.

Which brings us to our connection between COVID and Iran: MLPZX.

MLPZX is a “master limited partnership fund” that buys interests in MLPs that own U.S. energy infrastructure. Think of things like pipelines, storage systems, drilling rigs, oil and gas processing, etc.

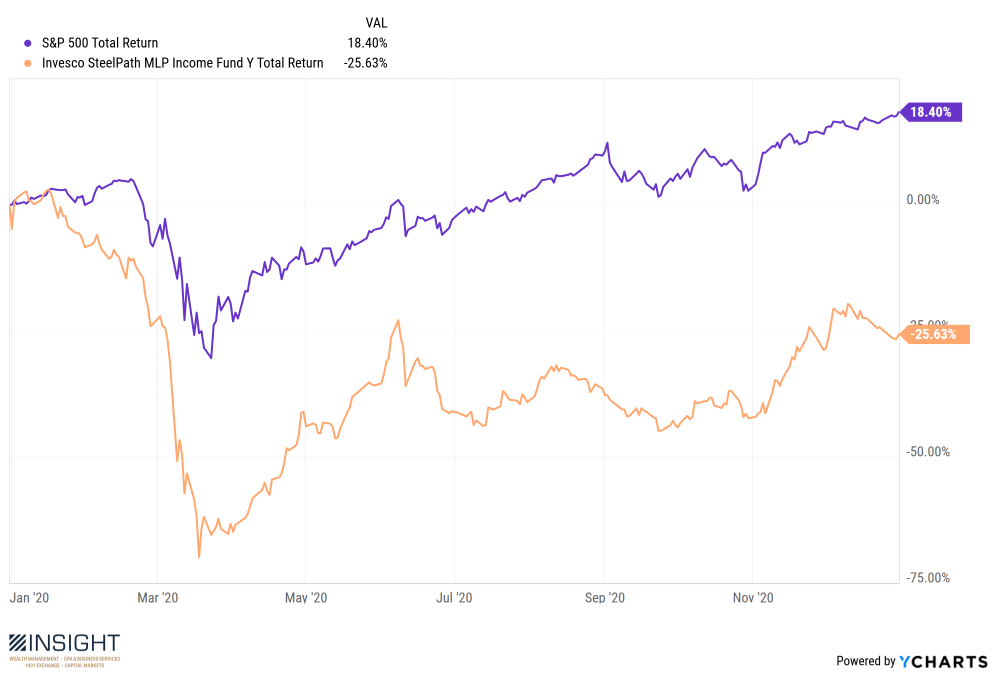

We owned MLPZX at the start of COVID. We didn’t look very smart. When the market was down 34%, it was down more than 70%. By the end of the year, the S&P was up more than 18%. MLPZX was still down nearly 26%.

Past performance is not indicative of future results.

Clients could have been forgiven for wondering what the heck we were thinking when we kept holding onto it. Even more so when we kept buying more shares on the way down.

But it wasn’t some sort of complicated decision.

Yes, oil prices were cratering. In fact – on April 20, 2020, the price of oil turned NEGATIVE. That’s right. If we wanted to sell you a barrel of oil, we had to give you the barrel and $37.63. Quite the deal!

It didn’t take an economics professor to figure out the simple truth: the world was overreacting. Cars would be on the road again. Planes would be full of passengers again. Semis would be hauling goods again. And they would all need energy. The other option – that the economy never recovered – meant the end of civilization as we knew it. If that happened, we were quite sure no one was going to care about a bad bet on MLPZX.

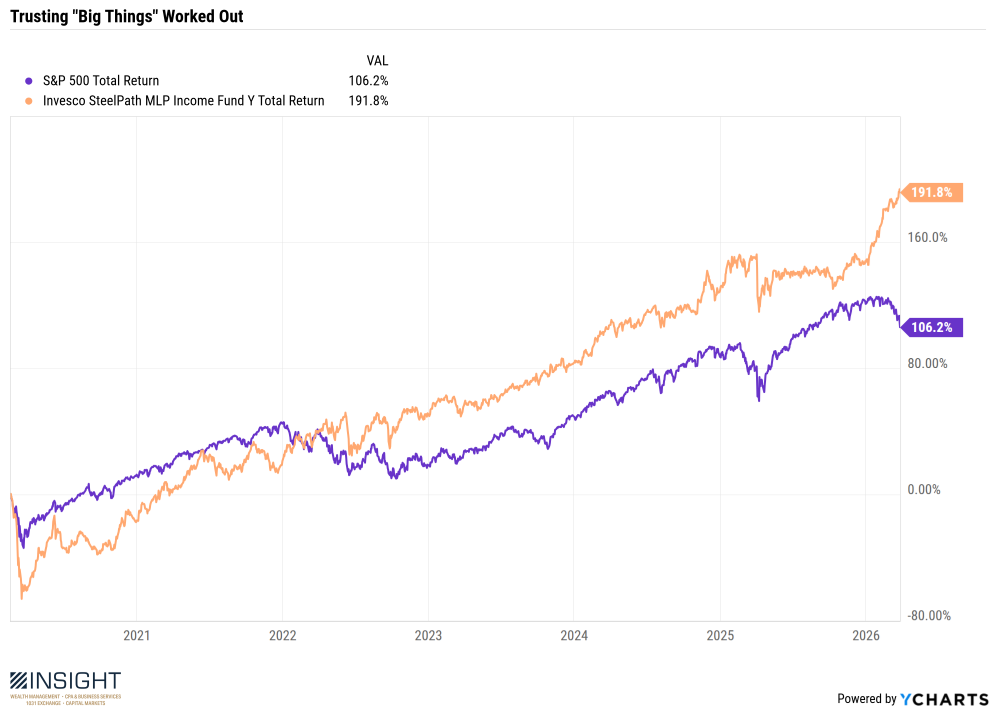

And so, we bought. And bought some more. And held. Our clients – YOU – were patient. It paid off. The chart below shows MLPZX from before the COVID troubles started (peak of the market on 2/19/2020) through last Friday. The result? It has outperformed the S&P 500 (total return – including dividends) by more than 85%.

Past performance is not indicative of future results.

Those are the “Big Things” we talk about so often. It’s not rocket science. Making a bet that the world isn’t going to end – where the risk if we’re wrong is beyond anyone’s control – is not that hard. But doing it when everyone on TV is telling us to panic? It still shouldn’t be hard – but it is.

That’s the “Fear & Greed” thing we’ve talked about so many times in these pages. It’s the behavioral science piece of investing that trips up so many investors. Betting against your instincts – on the upside and the down – is HARD. It’s not natural. Your brain doesn’t like it.

But we must do it. And one of the things that makes it so much easier is the group of investors we get to do it with. Because, on March 23, 2020, when the market was tanking and MLPZX made us look like fools, you weren’t panicking. We made almost zero sells that spring. You held strong.

It’s time to hold strong again. Interestingly, we think the incentive structure – on both sides – is positioned to move the U.S./Israel and Iran to the negotiating table. The White House has an economy and elections to worry about, and Iran has the future of their regime on the table. A negotiated settlement would help solve both problems.

But if they don’t? We still have plenty of opportunities ahead of us.

MLPZX? We still hold it. A lot of it! In our Conservative Growth model alone, it is an 11.5% weight in the model. And it’s performing remarkably well during this moment. It, along with a significant amount of other energy positions are our hedge against this moment. All told, nearly 8% of all holdings we have are in energy.

The defense MLPZX provides in this moment is great – but we will need some offense as well. That’s why our third largest holding is currently FBND – the Fidelity Total Bond Fund. It’s not exciting. It owns a lot of intermediate term dollar denominated debt. Nearly half of that is U.S. Treasuries. Is it going to make us a killing? No.

That’s not offense. Not yet. But if the bottom falls out of this market, it is going to be an asset we can sell to get more aggressive for the future. Much like we did in 2020.

Is a recession coming? Will this Iranian conflict cause the bottom to fall out of the market? It’s possible. But if that happens, we’re ready. We just have to remember that fear and greed can be particularly good tools – but only when they’re used in opposition to our instincts.

Sincerely,