The Weekly Insight Podcast – Nobody Knows, But Somebody Blinked

On March 9th, we wrote in our second memo on the Iran conflict that the market was leaning heavily into a “buy the dip” strategy for this current oil scare. As Goldman Sachs put it at the time:

“Investors should see any correction in equities as a buying opportunity, rather than signaling the start of a bear market…underlying economic resilience and robust earnings growth mean the depth and extent of a pullback will be limited.”

Source: Rose Henderson, www.bloomberg.com

It was a strategy grounded in history – both long-term and short-term. The long-term historical story was simple: oil scares were largely just that. They never developed into real supply disruptions. The short-term had proven equally steeped in experience: President Trump wouldn’t let this significantly harm the economy or the market. His maneuvering around tariffs is a recent example.

And the oil markets justified that optimism. When we wrote that memo, Brent crude (world oil prices) had risen just 27%. WTI crude (U.S. oil prices) had risen 31%. Bad? Of course. But certainly not catastrophic. And certainly not the jump you’d expect when 20% of the world’s oil and natural gas supply disappeared for an extended period.

Last week, the worm turned a bit. Oil prices continued to rise, equity markets suffered. And the narrative changed. On Wednesday, the Fed held rates steady – cementing concerns that no cuts were coming anytime soon. On Friday, the headlines were about the Russell 2000 and NASDAQ entering correction territory.

And the tone from the “experts” was shifting. Here’s what Goldman had to say on Friday:

“The persistence of several prior large supply shocks underscores the risk that oil prices may stay above $100 for longer in risk scenarios with lengthier disruptions and large persistent supply losses.”

Source: John Liu, www.CNN.com

They went on to note that the “stay above $100 math” may last until 2027.

That’s the same firm – just three weeks apart – with a vastly different message. And that’s not a knock on Goldman. Every other big firm has been going through the same change in tone. And Jerome Powell basically said as much on Wednesday when releasing the “Summary of Economic Projections” (SEP):

“If we were ever going to skip an SEP, this would be a good one. Because we just don’t know.”

The most highly respected analysts and economists in the world are telling you the same thing: they don’t know.

To claim we do know would be a recipe for disaster. We don’t. But our “Big Things” theory of the world has proven to be solid footing to stand on. And so, as the market has been trading the rhetoric for the last three weeks, we’ve been a little dumbfounded as the true impact of this supply disruption hasn’t been felt.

Last week, the world started to come to grips with our concerns.

Keep Perspective

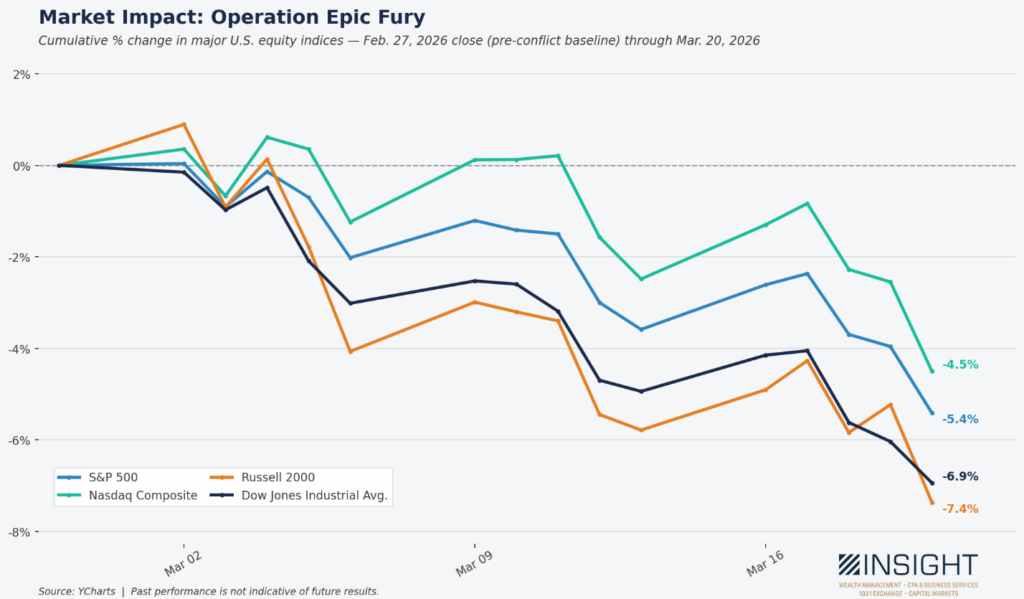

Despite this change in tone, the simple truth is this: markets haven’t been significantly impacted by this conflict. Yes, the Russell 2000 did close in correction territory on Friday. And the Dow and NASDAQ were close (down 9.19% and 9.26% respectively). But that is from their highs – not the start of the conflict.

Those highs were put in at the end of January – not the beginning of this conflict. It wasn’t oil prices that started this move lower. It was actually much more about AI and the weakening dollar at the time (see our memo from February 6th: The Great Rebalancing).

Past performance is not indicative of future results.

Since the conflict began, the returns have been negative but not in any significant way. The S&P is down 5.4% since the bombs started falling. We went back and looked – there have been 113 corrections of 5.4% or more in the S&P since 1950. That’s 1.5 times per year. These results are essentially a historical rounding error.

But – with the new change in tone from Wall Street – it’s now time to start asking the other question: where is the optimism today? What signs might be out there that indicate this process is nearer its end than its beginning? What signals should we be watching to know when to buy?

Mutually Assured Destruction

An interesting moment happened last week that drove oil prices significantly higher: On March 18th, Israel attacked the South Pars natural gas fields in Iran. This was a significant escalation.

South Pars is part of a very large gas field that stretches from Iran to Qatar. Qatar calls it North Dome. On the Iranian side, it provides 70% of Iran’s domestic gas consumption. It fuels power plants, heating systems, and petrochemical complexes. It is not a fuel depot; it is Iran’s economic lifeline.

Iran responded immediately and hit Qatar’s Ras Laffan facility. And the rhetoric from the Iranian side skyrocketed. Their Foreign Minister warned Iran would show “ZERO restraint” if their infrastructure were struck again.

And then the U.S. and Israel backed down. Trump noted the U.S. wasn’t aware it was happening. Netanyahu claimed full responsibility and said Israel acted alone (despite other Israeli officials confirming it was coordinated with the U.S.). Both said they would comply with not attacking infrastructure again.

This is the old Cold War idea of Mutually Assured Destruction (MAD) – only instead of nuclear weapons, we’re talking about energy infrastructure. If that dynamic can also grow to include transit in the Strait, the economic cost of this endeavor shrinks dramatically. As Marko Papic from BCA Research noted this week, “As long as there is a fine MAD balance regarding energy transit and production, the actual kinetic conflict in the region is irrelevant.”

The MAD balance – as it was during the Cold War – will be determined by the pain each adversary is willing to weather. And their ability to inflict pain on the other. As the battle rages, more information is showing us this won’t last forever.

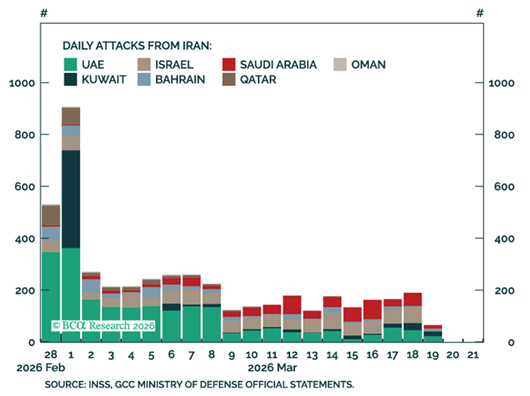

Iranian Capability Declining

Wartime rhetoric is full of propaganda. And – in today’s environment – full of AI faked videos that purport to show destruction where there is none. But one thing we can be certain of? The degradation of the Iranian military – and their ability to cause damage throughout the Middle East is declining. One only needs to see the data to understand it.

Past performance is not indicative of future results.

Notably, the 18th was the day of the South Pars attack. Iran’s response was to launch more attacks than they had since March 8th. But on the 19th? Their attacks fell to the lowest number since the start of the war. Their offensive capability is dwindling.

Trump’s Political and Economic Constraints

As the market data above showed, the economic impact of the conflict has yet to really hit home. Yes, oil prices are up. But the market is holding in there. Job losses aren’t accelerating. We haven’t seen a real spike in inflation yet.

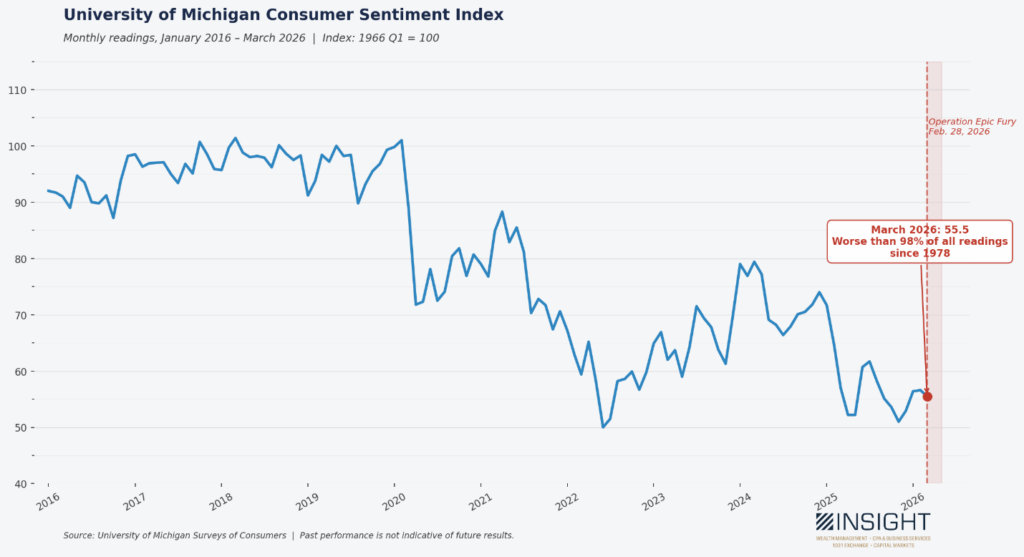

What we have seen, however, is public opinion shifting. Consumer Sentiment – from the University of Michigan – tumbled this month after the start of the war. A number that was as high as 70+ at the start of Trump’s current term – and was starting to climb out of the basement early this year – is back down to 55.5. That number is worse than 98% of all recorded results of this survey since 1978.

Past performance is not indicative of future results.

This is important because economic sentiment has in the past been an excellent predictor of election results. Anytime we’ve seen sentiment below 80 at a midterm election, the President’s party has lost – on average – 33 seats in the House. In an environment where the GOP controls the House 218 – 214 (with three vacancies), it can only lose two seats and maintain control.

Ending this war quickly – especially given the potential political impact – will clearly be a priority to the Trump Administration.

Off Ramps Presenting Themselves

Amidst all the rhetoric, several off-ramps are forming. The South Pars strike is an excellent example. What could have led to more escalation instead resulted in a reasonable decision by all parties to tone down the targeting.

Other optimistic moments have been happening in the last week. Iran floated a plan to reopen the Strait earlier this week that would include a fee for passage of $2,000,000. That seems…hefty. But when you consider the cargo, it isn’t. Depending on the size of the ship, that is an extra $2 – $3 per barrel.

It’s already started, but just barely. Iran confirmed Sunday they had already collected transit fees, calling it a “new concept of sovereignty” over the Strait. At least one Pakistani tanker transited Sunday along with two Indian ships and one Turkish ship. It’s not much – but oil is moving.

President Trump offered his own offramp on Friday. He stated the following on Truth Social:

“We are getting very close to meeting our objectives as we consider winding down our great Military efforts in the Middle East with respect to the Terrorist Regime of Iran…The Hormuz Strait will have to be guarded and policed, as necessary, by other nations who use it – The United States does not!”

Close to winding down is the beginning of an offramp if we’ve ever seen one. And the President makes a compelling point: the Strait of Hormuz is vitally important for the world (mostly China and India) – but we don’t really need it. Protecting the flow of oil through the Strait is an artifact from a much different time. Today, America produces more oil than it needs.

And now – despite initial pushback – twenty-two nations have signed an agreement pledging to help keep the Strait open for shipping. Why? As Trump noted, even if we started it, it’s much more their problem than it is ours.

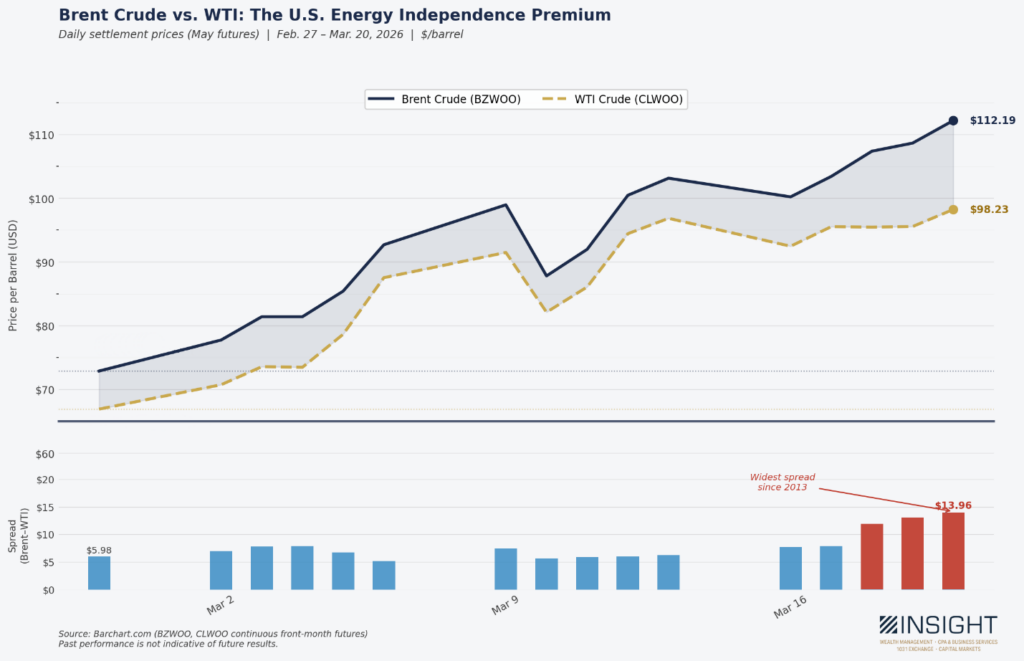

That’s why – especially in the last week – we’ve seen a significant expansion between the price of Brent crude (the world’s price) and the price of WTI crude (our local price). The spread reached nearly $14 on Friday. That’s the highest it’s been since 2013.

Past performance is not indicative of future results.

Not Quite Yet

24 hours is a long time on the world stage. Which is why it shouldn’t be a big shock that just a day after posting about “winding down” and letting the rest of the world worry about the Strait, President Trump posted this to Truth Social:

“If Iran doesn’t FULLY OPEN, WITHOUT THREAT, the Strait of Hormuz, within 48 HOURS from this exact point in time, the United States of America will hit and obliterate their various POWER PLANTS, STARTING WITH THE BIGGEST ONE FIRST!”

That was posted at 7:44PM EDT on Saturday. Meaning the deadline expires Monday at 7:44PM EDT. The market will be hyper focused on this Monday.

It’s not quite the offramp that Friday’s message was. But interestingly enough – if the deadline passes without significant escalation – it may end up proving Trump’s Friday missive. It may be the biggest off-ramp yet.

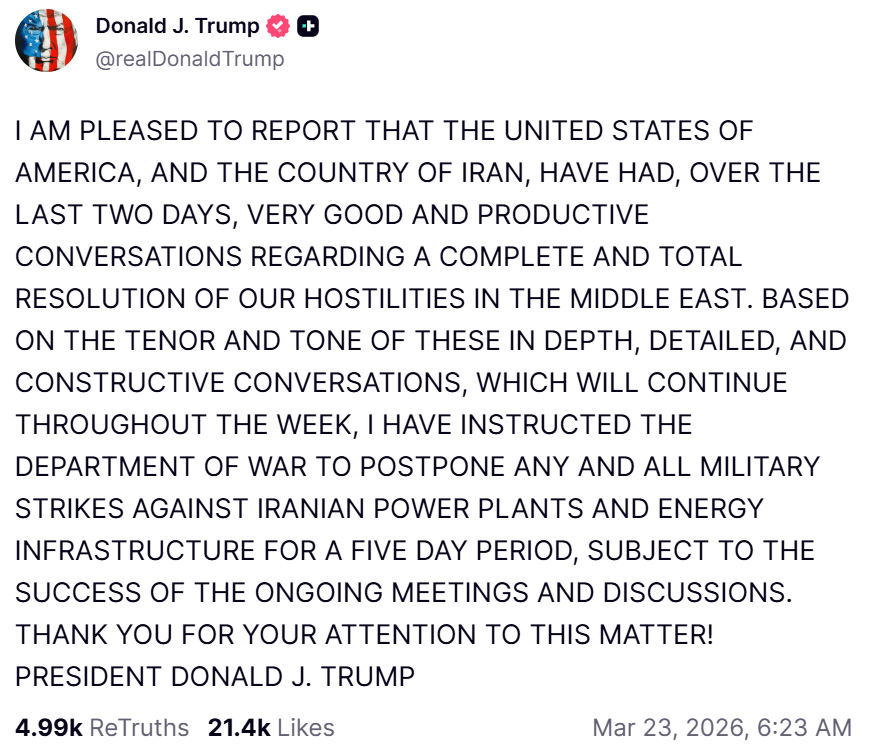

EDITOR’S NOTE: Somebody blinked! Trump posted the below message on Truth Social early this morning.

Iran denied the negotiations but simultaneously declared victory on state TV. Both sides are managing their domestic audiences – but the market read right through it. At the open, equities are up and oil is down sharply. As noted above when this was written, this may prove to be the offramp the market was looking for.

What We’re Watching

Powell said it Wednesday: We don’t know. The analysts have been saying it all along as they’ve moved their goal posts since the beginning of this conflict. Frankly, even the leaders of Iran, Israel, and the United States are saying it in their own way. How this ends – how quickly and how painfully – is very much up in the air.

The pain for markets hasn’t been nearly as much as we worried it could be. That’s good news. If that pain does end up coming, we’re still well allocated for the moment. That hasn’t changed.

But when this is done, the market will shift very quickly. Which is why we’re looking at a number of signals to help us understand what the end looks like. They include:

1. Capitulation on Saturday’s Threats: Iran responded to Trump’s Saturday evening “Truth” by saying they would “permanently close the Strait” if he attacked their power plants. Will either of them blink? If not – and Trump moves forward with the attacks – it would signal an escalation of the conflict.

NOTE: This is now confirmed. The market’s reaction speaks for itself.

2. Tacit Approval of $2 million Transit Fee: Iran has started this process. If it continues without U.S. intervention, it could significantly free up oil transit. It may be a quiet way to slow the conflict.

3. WTI/Brent Spreads Narrow: If prices start to drop AND the spread between Brent and WTI begins to narrow, that is a sign physical supply is returning to the market. That’s your best leading indicator.

4. Coalition Ships Begin to Move: It’s one thing to promise ships to open the Strait. It’s another to put your sailors in the midst of a hot war. If the coalition begins to move and work to guarantee safe passage, it’s a sign of cooling in the battle.

Much like everyone else – we don’t know what will happen in the coming weeks and months. But we do have a good idea of what moves the needle and how we need to react. How this plays out today – and through this week – will help us understand if this is a multi-month process or something which will begin to wind down more quickly.

Sincerely,